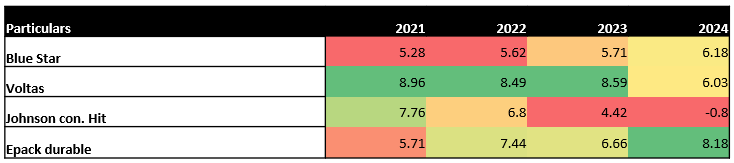

Operating profit margin (%)

• Between 2021 and 2024, Blue Star maintained steady yet gradual growth in its operating profit margin. In contrast, Voltas, which had the highest margin in 2021, saw a consistent decline, reaching 6.03% in 2024.

• Epack Durables emerged as the leader with the highest operating profit margin among peers in 2024, while Blue Star secured the second position. This highlights Blue Star’s improving margin performance relative to its peers, driven by a 21.4% increase in revenue and a 3.5% rise in net profits.

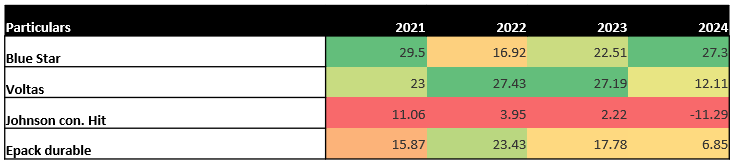

ROIC(%)

• In 2024, Blue Star recorded the highest ROIC among its peers, maintaining steady and consistent ROIC performance in previous years with minimal fluctuations. This reflects the company’s ability to effectively generate returns from its invested capital. Additionally, the ₹1,000 crore raised through QIP in FY24 could further enhance ROIC if the deployed capital are utilized efficiently in value-accretive activities. {3}

• In contrast, Johnson Controls reported a negative ROIC of -11.29% in 2024, marking the lowest performance across all years among its peers. Epack Durables also experienced a sharp decline in ROIC from 2021 to 2024, highlighting challenges in sustaining returns on invested capital.

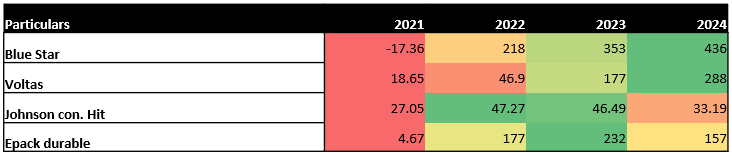

Net Capex(cr.)

• Blue Star’s capex experienced a remarkable increase, jumping from -₹17.36 crore in 2021 to ₹436 crore in 2024. This reflects the company’s aggressive investment strategy, focusing on expansion and the development of innovative products aimed at decarbonization and energy efficiency for OEMs in Europe and North America. {3} Additionally, the company plans to expand its product offerings in the Room Air Conditioner and Commercial Refrigeration segments by launching new models.

• While all peers have shown consistent year-on-year growth in capex, Blue Star stands out with the highest capex in 2024. In contrast, Johnson Controls-Hitachi reported the lowest capex in 2024, continuing its year-on-year decline.

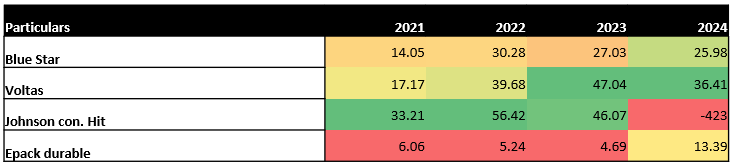

EV/EBITDA

• Blue Star has maintained a stable EV/EBITDA compared to its peers during 2021–2024, indicating that the company is neither undervalued nor overvalued in the market. This stability is attributed to a consistent increase in the company’s revenue, accompanied by a steady rise in its EV/EBITDA.

• On the other hand, Johnson Controls-Hitachi experienced a significant shift, moving from the highest EV/EBITDA in 2021 to a negative EV/EBITDA in 2024. Meanwhile, Voltas currently holds the highest EV/EBITDA, suggesting that it is overvalued relative to its earnings.