ANGELONE’s top peers are ICICI Securities Ltd. (ISEC), Motilal Oswal Financial Services Ltd. (MOTILALOFS) and IIFL Capital Services Ltd. (IIFLCAPS).

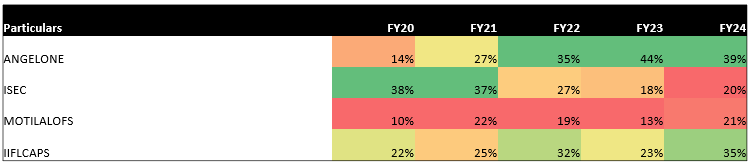

Comparison of company’s key metrics with top peers

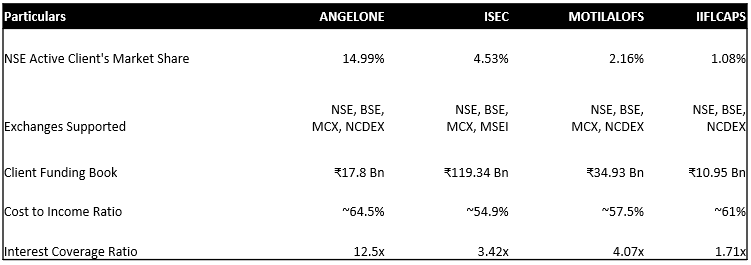

ANGELONE holds a market share of 14.99% in the NSE Active Client base ranking it third highest in the online discount broking segment, significantly outperforming its competitors. While ISEC, MOTILALOFS, and IIFLCAPS had a market share of 4.53%, 2.16%, and 1.08%, ANGELONE had almost 2x of that combined. This shows the company's clear dominance in terms of active NSE clients, which, with ANGELONE’s healthy customer acquisition and retention rate, is set to increase even further due to the increase in retail activity in the capital markets. Moreover, the company provides services across NSE, BSE, MCS, and NCDEX, attracting customers who desire to trade through different exchanges.

The company’s client funding book lagged behind competitors like ISEC and MOTILALOFS, whose books amounted to ₹119.34 billion and ₹34.93 billion. Although ANGELONE’s client funding book was higher than that of IIFLCAPS’s book, which totaled ₹10.95 billion, the company’s performance in this sector was comparatively less than that of its peers. The company’s client funding book amounted to ₹17.8 billion at the end of FY24, growing by only 7.9% YoY.

ANGELONE has the highest cost-to-income ratio, which equals about 64.5%, as compared to its competitors whose cost-to-income ratios range from 54% to 61%. This indicates that the company has some improvements to work in terms of operational efficiency to decrease its cost-to-income ratio and stay aligned with its competitors to remain a leading company in the industry.

Lastly, the company’s interest coverage ratio majorly surpassed its competitors with a number of 12.2x. The company’s peers, ISEC, MOTILALOFS, and IIFLCAPS had ratios of 3.42x, 4.07x, and 1.71x, indicating that ANGELONE has more than enough funds to comfortability take care of its interest expenses and does not have to rely on any contingent plans. However, in some cases, an extremely high-interest coverage ratio might suggest that the company is not efficiently employing debt securities.

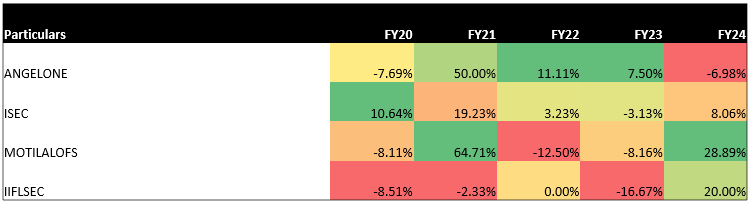

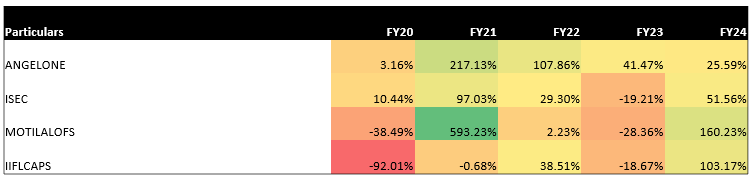

Operating Profit Margin Growth (%)

After decreasing in FY20, ANGELONE’s operating profit margin growth rate increased for three year, but in FY24 the margin growth declined to -6.98% indicating a decrease in operatiooperationalnally efficiency.

In comparison, ISEC showed impressive stability in its operating growth through the years, ending with an increase of 8.06% in FY24, as opposed to IIFLCAPS, whose operating margin saw a majority decline but finally increased by a healthy 20% in FY24.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.