Peer analysis of Federal Bank, IndusInd Bank, and IDFC First Bank, three mid-sized private sector banks with comparative market capitalizations as of FY24.1 9 11

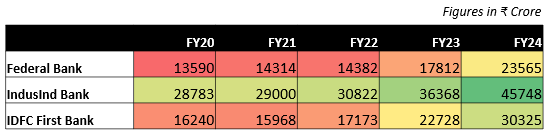

Revenue

• Federal Bank reported consistent growth, with revenue increasing from ₹13,590 crore in FY20 to ₹23,565 crore in FY24, achieving a CAGR of 16.9%. This performance was supported by a focus on high-margin retail products, stable Net Interest Margins, and an expanding credit portfolio driven by digital adoption and physical network growth.

• IndusInd Bank maintained steady growth, with revenue rising from ₹28,783 crore in FY20 to ₹45,748 crore in FY24, reflecting a CAGR of 12.9%. The bank sustained a larger revenue base throughout this period.

• IDFC First Bank reported the highest revenue growth, with a CAGR of 21.7%, as revenue increased from ₹16,240 crore in FY20 to ₹30,325 crore in FY24. This growth was driven by a shift from wholesale and infrastructure financing to a retail-focused model, following its merger with Capital First. Retail assets grew from 37% of total funded assets in FY20 to 63% by FY21. The bank expanded its retail loan portfolio, strengthened its retail deposit base, and used Capital First’s expertise, branch network, and technology to enhance operations and customer outreach.

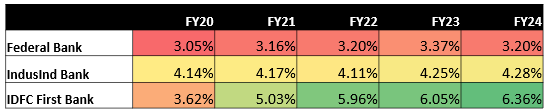

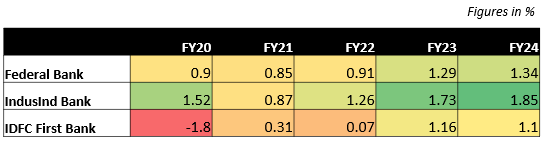

Net Interest margin

• Federal Bank's NIM has remained relatively stable, ranging between 3.05% and 3.37% from FY 20 to 24. Further, NIM is projected to improve to 3.5 to 4% by FY27, driven by the bank’s focus on increasing CASA deposits and high-yielding retail loans.

• IndusInd Bank's NIM has also shown stability, fluctuating between 4.11% and 4.28%. It is further expected to remain stable, benefiting from its established wholesale banking model.

• In contrast, IDFC First Bank has experienced a significant improvement in its NIM, rising from 3.62% in FY20 to 6.36% in FY24. This increase is partly due to a focus on high-margin retail products. Additionally, after merging with Capital First, the bank's Current Account Savings Account (CASA) deposits have grown significantly, now making up nearly 50% of total deposits. Since CASA deposits are a low-cost source of funds, this has helped improve the bank's NIM and profitability.

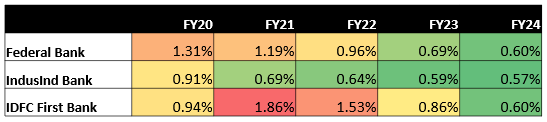

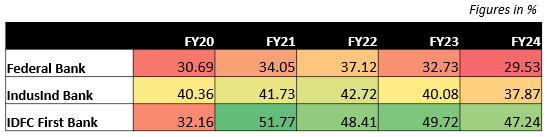

Net NPA

• Federal Bank has consistently reduced its Net NPA ratio, from 1.31% in FY20 to 0.60% in FY24. The bank’s GNPA ratio is expected to remain stable at around 2.1% over the next three years, supported by its proactive credit monitoring systems and focus on retail loans, which are less prone to defaults. Federal Bank’s diversification efforts to reduce concentration in South India will further strengthen its asset quality.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.