Written By: Bhumika Jain

If you’ve ever listened to a company’s conference call, you’ve likely heard management mention “You will see the benefits of operating leverage from next quarter onwards”. But what does it actually mean?

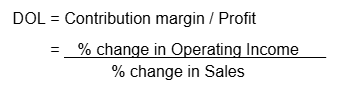

Operating leverage is about how a company’s fixed costs affect its profits without making any changes to the selling price, margin, or the number of units it sells.

Imagine you run a factory that makes shoes.

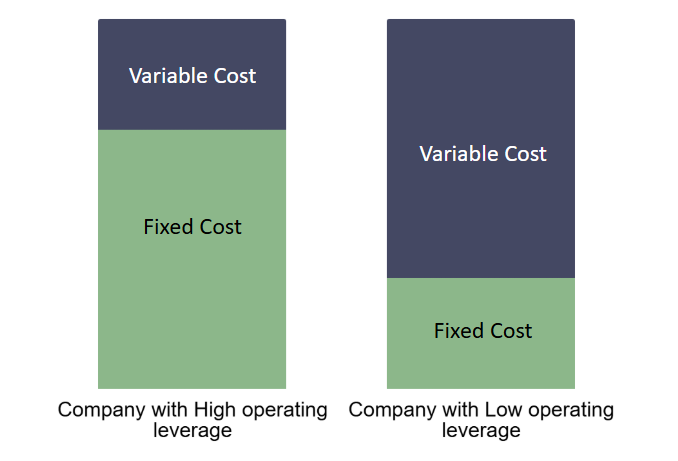

1) Fixed Costs: These are your constant expenses like rent, machinery, and salaries, let's say are ₹1,00,000 every month - you pay them whether you produce 10 shoes or 10,000 shoes.

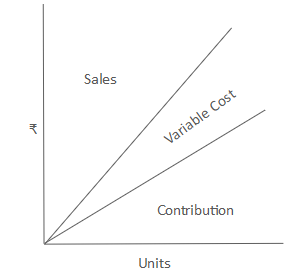

2) Variable Costs: These depend on how much you produce, like raw materials.

Now, if your sales go up, your fixed costs don’t change, so most of that extra revenue turns into profit. This is operating leverage - when higher sales lead to disproportionately higher profits because fixed costs remain constant.

It is important to compare operating leverage between companies in the same industry, as some industries have higher fixed costs than others. The concept of a high or low ratio is then more clearly defined.

If you only sell 10 shoes in a month, the fixed costs still need to be covered. So, each shoe would have to contribute a larger portion of the profit to cover that ₹1,00,000. So, Low operating leverage companies may have high costs that vary directly with their sales but have lower fixed costs to cover each month.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.