Written By: Saizal Agarwal

In the world of finance, managing the balance between short-term liquidity and long-term stability is a delicate art. One key strategy that financial institutions use to achieve this balance is borrowing short-term loans to fund long-term loans. At first glance, this might seem unexpected – why would a bank or lending institution take on short-term debt to finance long-term assets or loan?

The answer lies in the complex dynamics of asset-liability management , a strategy that financial companies use to match their resources with customer needs, helps them manage risks like changing interest rates, liquidity issues, and shifting market conditions. In simple terms, it’s about ensuring that a company has enough short-term funds to support long-term investments.

Now this leads to the question that what exactly is asset-liability management ?

Asset-Liability Mismatch is a term that refers to the misalignment between the assets (loans, investments) and liabilities (deposits, borrowings) in terms of maturity or cash flow timing. This mismatch, commonly seen in financial institutions like banks and NBFCs (Non-Banking Financial Companies), can expose these entities to severe liquidity and interest rate risks, especially during economic downturns.

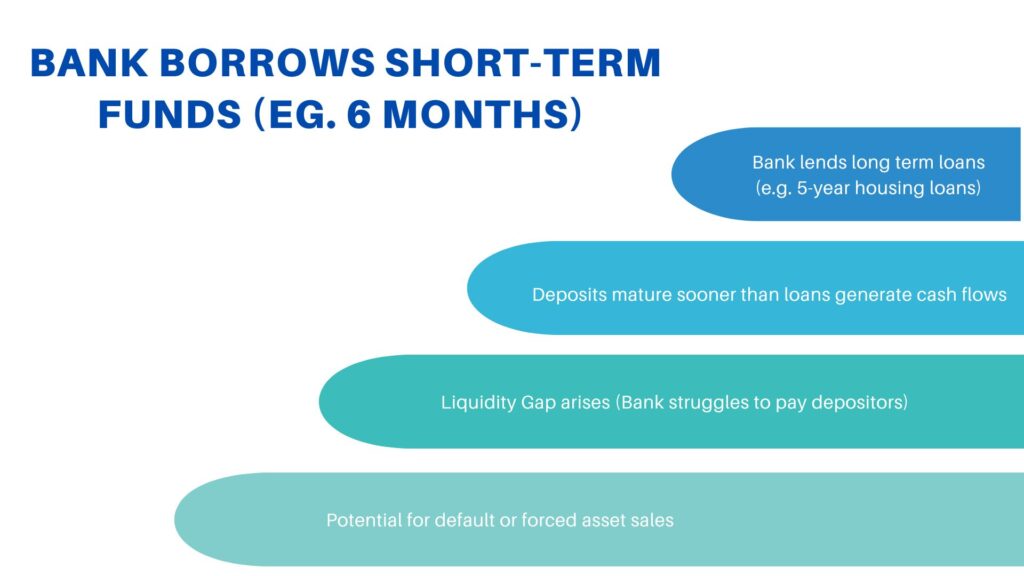

It occurs when the duration, interest rate, or cash flows of assets differ significantly from liabilities. Financial institutions generally borrow funds for the short term (such as customer deposits) but lend for longer periods (such as mortgages or business loans). The returns from these assets often exceed the costs associated with short-term liabilities, creating a profit opportunity. However, if liabilities come due before assets generate cash flow, the institution may face a liquidity shortfall, leading to financial distress. But, despite the risks, banks and NBFCs often engage in to optimize returns or meet specific business objectives.

What are the risks involved in asset-liability mismatches & how can they impact financial institutions?

- Liquidity Risk

It is one of the most immediate and significant concerns in Asset-Liability Management . It refers to the risk that an institution may not have enough liquid assets to meet its short-term obligations when they come due, which can lead to a liquidity crisis.

In the context of financial institutions, liquidity is the ability to quickly convert assets into cash or access funds to meet obligations such as paying off short-term borrowings or other financial commitments.

Financial institutions like banks or NBFCs often deal with mismatches in the timing of cash inflows and outflows. While they may have long-term assets like loans or investments that will generate returns over time, they must still meet short-term liabilities, such as maturing debt, operational expenses, or customer withdrawals. Basically, when there is a mismatch between the maturity of liabilities and the cash flow generated from assets, liquidity risk arises.

- Example: The IL&FS (Infrastructure Leasing & Financial Services) crisis in India, which came to a head in 2018, was a result of liquidity risk stemming from a classic asset-liability mismatch. IL&FS, a large NBFC, borrowed heavily through short-term debt instruments like commercial papers to finance long-term infrastructure projects, such as highways and power plants. While these projects were expected to generate cash flows over time, they faced delays and cost overruns, preventing IL&FS from meeting its short-term debt obligations. When market conditions tightened, and the company struggled to refinance its debt, IL&FS found itself unable to raise the necessary funds to meet maturing liabilities.

As a result, IL&FS defaulted on payments in 2018, triggering a liquidity crisis. The company's defaults led to a widespread loss of confidence in the NBFC sector, causing a ripple effect across financial institutions that had exposure to IL&FS's debt. The crisis ultimately required government intervention to manage the debt restructuring process and stabilize the financial system. This incident highlighted the dangers of relying on short-term financing for long-term investments, exposing the vulnerabilities of financial institutions to liquidity risks.

- Interest Rate Risk

Asset Liability Mismatch exposes institutions to interest rate fluctuations, especially if the cost of borrowing increases faster than the yield on long-term assets. For instance, if a bank funds long-term loans with short-term deposits, a rise in interest rates could increase the cost of deposits, reducing profitability. If not managed well, this could erode the net interest margin and lead to financial strain. - Example: Suppose a bank funds 10-year fixed-rate mortgages using 1-year loan.

- The 10-year fixed-rate mortgage might offer a 7% interest rate to the borrower, which means the bank earns 7% annually for the next 10 years.

- However, the bank uses 1-year loan as its funding source with 5% p.a. interest rate which initially sounds low.

- Now, imagine that interest rates rise due to an increase in inflation or a tightening of monetary policy by the central bank. The cost of the 1-year loan for the bank could increase from 5% to 6% or 7% in the next year. However, the interest rate on the 10-year fixed-rate mortgage remains locked at 7% for the entire loan duration.

- This situation creates a mismatch in the interest rate sensitivity between the bank's liabilities (the 1-year loan) and its assets (the 10-year fixed-rate mortgage).

This results in a squeeze on profitability, as the bank cannot adjust mortgage rates to reflect the higher funding costs, reducing its net interest margin. The mismatch between rising short-term funding costs and stable long-term asset returns increases interest rate risk, putting pressure on the bank’s financial stability and profitability.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.