Negative Alpha: If an investment has a negative alpha, it means the investment has underperformed the market or benchmark. For example, if an alpha of -1.0 means the investment performed 1% worse than the market.

Zero Alpha: If an investment has an alpha of zero, it means the investment performed exactly in line with the market or benchmark.

The concept of alpha came about when weighted index funds were created. These funds try to match the performance of the whole market by giving equal weight to different investment areas.

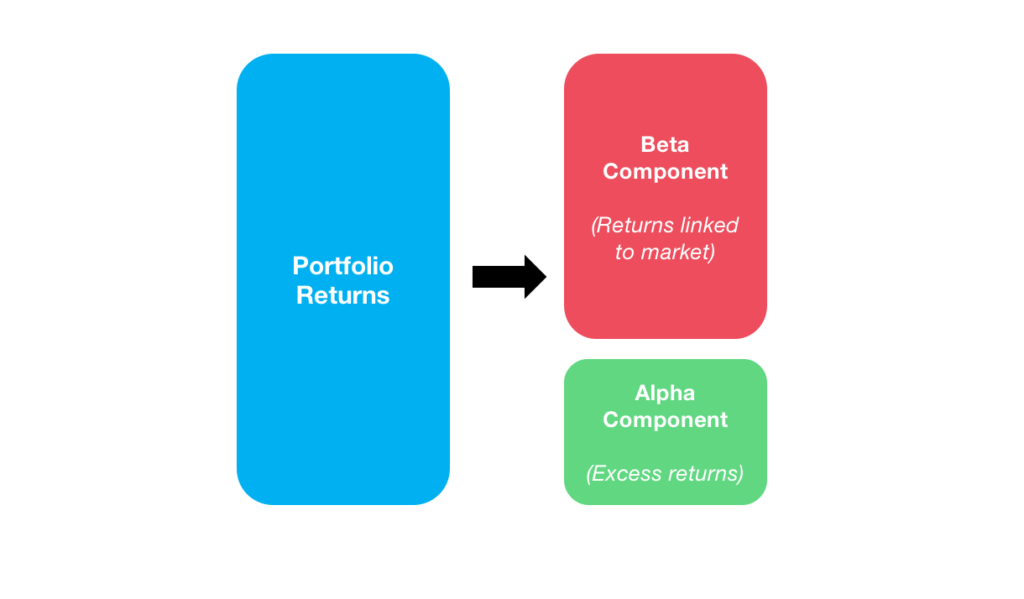

Alpha is one of five popular technical investment risk ratios. The other four are beta, standard deviation, R-squared, and the Sharpe ratio. These are all statistical measurements used in modern portfolio theory (MPT) and are intended to help investors understand the risk and potential return of an investment. Each measure provides insights into different aspects of the investment's performance and risk.

To get a deeper understanding, we can use “Jensen’s Alpha” (in honor of Michael Jensen, an economist who developed a method for calculating alpha as part of his work on the Capital Asset Pricing Model). This method takes into account the Capital Asset Pricing Model (CAPM), which adjusts for risk. CAPM uses beta to estimate what the return of an investment should be based on its risk level and overall market returns. By comparing alpha and beta, investors can better evaluate and compare the performance of their investments.

Calculating Alpha

The formula for Jensen's Alpha is:

α = Ri − [ Rf + βi × ( Rm − Rf ) ]

Where:

Ri = Return of the investment

Rf = Risk-free rate of return

βi = Beta of the investment

Rm = Return of the market or benchmark index

Let's walk through an example using hypothetical data for a company, say Reliance Industries, and the Nifty 50 index.

We assume that Reliance Industries' stock returned 15% over the past year and the Nifty 50 returned 12% over the past year. The yield on 10-year Indian Government Bonds is 7% and the beta for Reliance Industries is assumed to be 1.

By applying the formula: α = Ri − [ Rf + βi × ( Rm − Rf ) ]

α = 15% −

Calculating the Expected Return:

Rm − Rf = 12% − 7% = 5%

βi × ( Rm − Rf ) = 1.1 × 5% = 5.5%

Rf + βi × ( Rm − Rf ) = 7% + 5.5% = 12.5%

Calculating Alpha:

α = 15% − 12.5% = 2.5%

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.