Research By: Yug Goyal

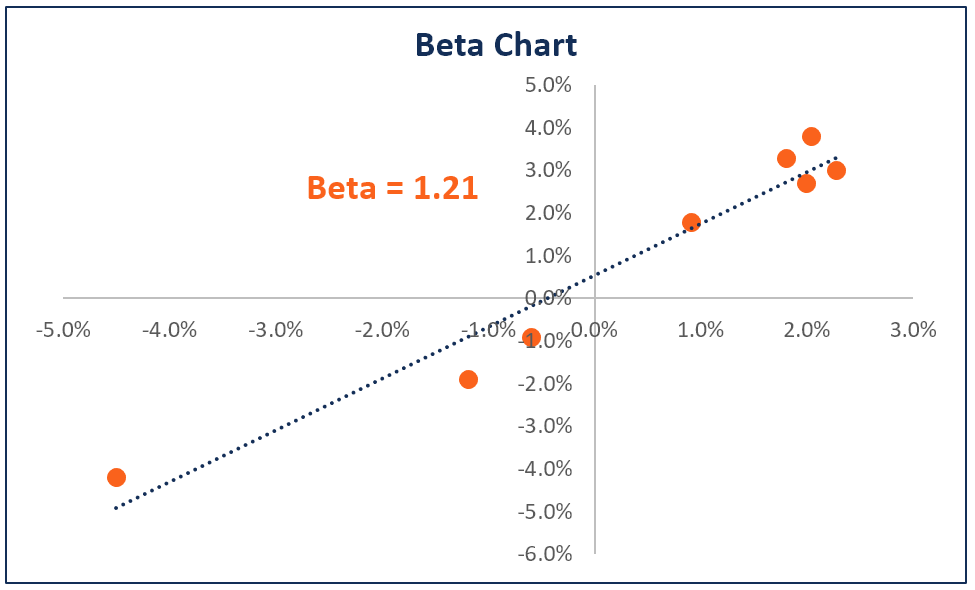

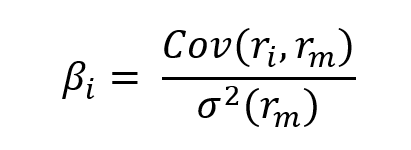

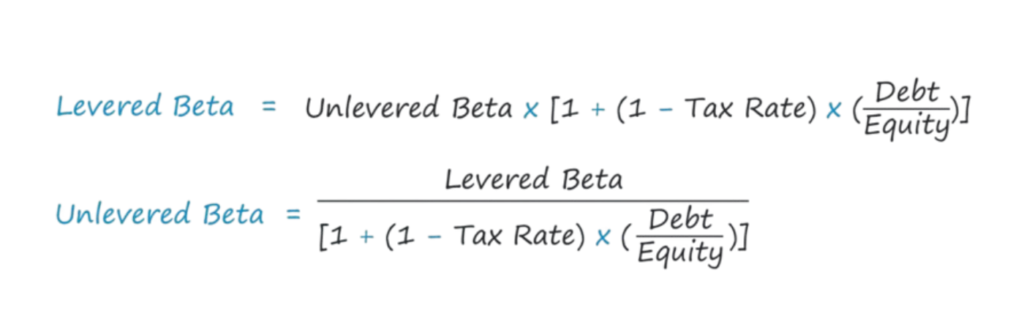

Beta is the measure of systematic risk.

Before moving on to beta, it is important to understand the 2 types of risk- systematic and unsystematic.

- Systematic risk refers to the risk inherent to the entire market or market segment. Systematic risk, also known as undiversifiable risk, volatility risk, or market risk, affects the overall market, not just a particular stock or industry. Systematic risk, also known as market risk, cannot be reduced by diversification within the stock market. Sources of systematic risk include: inflation, interest rates, war, recessions, currency changes, market crashes and downturns plus recessions.

- Unsystematic risk, also known as company-specific risk, represents risks of a specific corporation, such as management, sales, market share, product recalls, labor disputes, and name recognition. This type of risk is peculiar to an asset, a risk that can be eliminated by diversification.

So, beta measures the systematic risk of the company. It measures the volatility of the stock with respect to the market. The market, often represented by a major index like S&P 500 in US or Nifty 50 in India, has a beta of 1.

Some interpretations of beta are –

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.