Research By: Navya Sinha

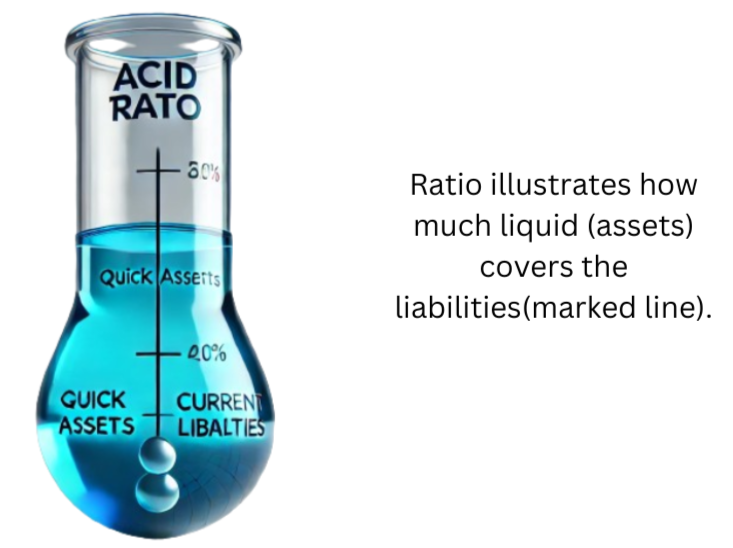

Acid-Test Ratio also known as the quick ratio, is a liquidity ratio that measures how sufficient a company’s short-term assets are to cover its current liabilities. In other words, the acid-test ratio is a measure of how well a company can satisfy its short-term (current) financial obligations.

Understanding The Ratio

Analysts sometimes prefer using the acid-test ratio instead of the current ratio (or working capital ratio) because the acid-test ratio excludes assets like inventory, which are difficult to liquidate quickly. This makes the acid-test ratio a more cautious measure of a company's financial health.

Generally, an acid-test ratio of 1.0 or more indicates a company can pay its short-term obligations. Companies with an acid-test ratio of less than 1.0 do not have enough liquid assets to pay their current liabilities and should be treated cautiously. If the acid-test ratio is much lower than the current ratio, a company's current assets are highly dependent on inventory.

However, this isn't always a negative indicator, as some business models naturally depend on inventory. For instance, companies having retail stores business might have very low acid-test ratios without being at risk. What's considered an acceptable acid-test ratio varies by industry.

For most industries, the acid-test ratio should exceed 1.0. On the other hand, a high ratio is not always good. It could indicate that cash has accumulated and is idle rather than being reinvested, returned to shareholders, or otherwise put to productive use.

The acceptable range for an acid-test ratio depends on the industry and marketplaces the company operates in, so comparisons are most meaningful when evaluating companies within the same industry.

Formula

The following items can all be found on a company’s balance sheet:

- Cash and cash equivalents are the most liquid current assets on a company’s balance sheet, such as savings accounts, a term deposit with a maturity of fewer than 3 months, and T-bills.

- Marketable securities are liquid financial instruments that can be readily converted into cash.

- Accounts receivables are the money owed to the company from providing customers with goods and/or services.

- Current liabilities are debts or obligations due within one year.

The acid-test ratio formula can alternatively be rendered as follows:

where:

Current assets are assets that can be reasonably converted into cash within a year.

Inventories are the value of materials and goods held by a company with the intention of selling them to earn profits.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.