Written By: Soumya Singhal

Companies capitalize rather than expense a purchase when the item provides future economic benefits beyond the current accounting period. Capitalizing spreads the cost over the asset's useful life, aligning expenses with the revenues they help generate, a practice based on the matching principle in accounting.

The difference between capitalization and expense lies in how a company records a cost on its financial statements and how it affects profitability over time. Here’s a breakdown:

| Aspect | Capitalization | Expense |

| Definition | Recording a cost as an asset on the balance sheet to be depreciated or amortized over its useful life. | Recording a cost directly on the income statement reduces profits in the current period. |

| Purpose | Used for expenditures that provide long-term benefits. | Used for expenditures that provide short-term benefits. |

| Accounting Treatment | Added to the balance sheet as an asset and depreciated/amortized over time. | Recorded as an expense on the income statement in the period incurred. |

| Effect on Net Income | Spreads the cost over several periods, minimizing the immediate impact on net income. | Reduces net income in the period it is incurred. |

| Impact on Financial Statements | Increases in assets on the balance sheet and delays impact the income statement. | Reduces net income and retained earnings immediately. |

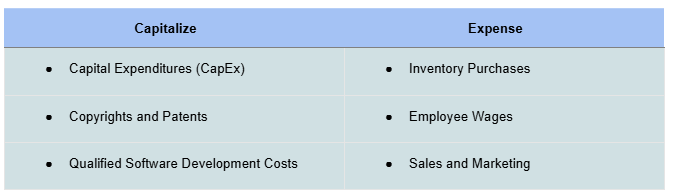

| Examples | - Purchasing machinery, buildings, or software.- Construction of a new factory.- Development of a patent. | - Office supplies.- Salaries and wages.- Utility bills.- Routine maintenance. |

| Impact on Cash Flow | Recorded in the investing activities section of the cash flow statement. | Recorded in the operating activities section of the cash flow statement. |

| Financial Ratios | Improves profitability ratios (e.g., EBITDA, net profit) in the short term. | Immediately reduces profitability ratios. |

| Depreciation/Amortization | Depreciated (for tangible assets) or amortized (for intangible assets) over time. | No depreciation or amortization; fully expensed in the current period. |

Generally, one useful question is, “Will the cost continue to provide benefits for more than a year?”

- Yes?✅ → Capitalize

- No?❌ → Expense

If the anticipated useful life exceeds one year, the item should be capitalized – otherwise, it should be recorded as an expense.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.