Written By: Anika Manav

For investors, analysts, and stakeholders, it is important to understand the reasons for the difference in data regarding debt on a company’s annual and credit rating reports. An annual report focuses on a company in its entirety, incorporating information regarding every aspect of the company. On the other hand, a credit rating report only focuses on areas relating to the debt financing of the company and the possible risks associated with the company and the industry.

Moreover, the purpose of an annual report is to provide readers with the results and highlights of the company during the preceding financial year, whereas, a credit rating report needs to incorporate the historical debt standing of a company and conclude the level of risk associated with its financial instrument.

This difference in intended purpose and main focus might lead the respective publishers to use different accounting standards and rules to report and analyze the data with them.

Let us understand the reasons for this difference in debt reports with the help of an example.

Samman Capital Ltd (SCL), a non-banking financial company (NBFC), announced that it will be taking on the loan book of its wholly-owned subsidiary, Samman Finserve Ltd. (SFL) and then ICRA, a credit rating agency, issued ratings on those debt instruments.

Here are the snapshots of the debt reported in the annual report of the company and then the credit rating report issued by ICRA, respectively.

Source: Sammaan Capital Limited Annual Report – FY24, Page-138

Source: ICRA Report – 26th November, 2024, Page-1

As noted above, the subordinated debt and debt securities reported on the annual report amounted to approximately ₹4,188 Crore and ₹14,488 Crore, while on the credit rating report, the subordinated debt and the total debentures were ₹450 Crore and ₹5,550(2,250+3,300) Crore, respectively.

1. Repayment or Redemption of Debt

The most common reason for the difference in debt reported in an annual report and a credit rating report is the repayment or redemption of debt liabilities during the time between the publishing dates. Where annual reports are published yearly, usually as a regulatory compliance for public companies, credit rating reports are made in relation to reasons such as new issues of financial instruments or updating previous ratings.

In the annual report for SCL, the independent auditor’s report was dated 24th May 2024, and on the other hand, the ICRA report was last updated on 26th November 2024. This almost 6-month difference leads to some of the debt to be repaid.

To understand this difference, let us look at some other amounts reported in the SCL annual report and the ICRA credit rating report.

Source: Sammaan Capital Limited Annual Report – FY24, Page-211

Source: ICRA Report – 26th November, 2024, Page-7

As seen above, only the amounts redeemable after September 2024 have been reported, because securities with a maturity date before that have already been redeemed. This is also the case regarding the repayment of certain loans, leading to them not being considered in the credit rating report.

2. Inclusion of Proposed Debt

The credit rating reports include debt instruments that are proposed by the company, meaning those instruments that are yet to be issued.

Below, is an abstract of a credit rating report by CRISIL Ratings on IIFL Securities Limited, now IIFL Capital Services Limited, and we can see that the agency has incorporated the proposed debt instruments in their rating, but in the annual report there is no mention of them.

Source: CRISIL Ratings Report – 28th March, 2024, Page-1

Source: IIFL Securities Limited Annual Report – FY24, Page-292

This proposed debt was not recorded in the annual report of IIFL, leading to different numbers.

3. Coverage Of Debt

Another factor that might contribute to the difference between the debt reported in annual reports and credit rating reports is that the credit report is not rating the entire debt securities of a company, and thus, does not need to consider the liabilities that it does not deem relevant.

Let us look at the notes to account for the company and the debt instruments listed in the credit rating report.

Source: Sammaan Capital Limited Annual Report – FY24, Page-172

Source: ICRA Report – 26th November, 2024, Page-1

As we can see, the credit rating agency has not mentioned the borrowings other than debt securities in the report as it is not rating those loans, leading to a difference in the figures.

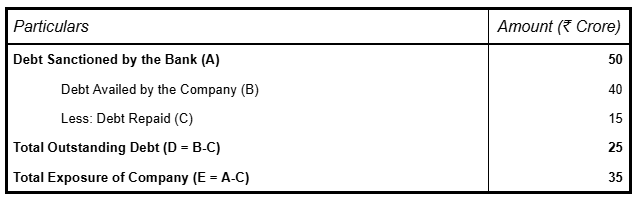

4. Treatment of Unused Debt

The next reason why the debt reported in these two reports will be different is the difference in the treatment of unused debt by the company and the agency. In the company’s annual report, unused debt is not mentioned under the liabilities segment, but on the other hand, a credit rating report does include those debt securities in its calculation of the risks associated with the company or the instruments.

Let’s consider an example where the following details are given regarding the debt of a company.

In this example, the company’s annual report will show the total outstanding debt to be ₹25 Crore in the balance sheet, but on the other hand, the credit rating report will show a total exposure of the company, which is ₹35 Crore.

This is also a big reason for the difference in debt amount reported in the two reports.

5. Change in Market Value

One of the reasons for the difference in the amount of debt on these two reports can be due to the fluctuation in the market value of debt instruments such as debentures.

Let us look as an extract of the bifurcation of redeemable non-convertable debentures in both reports.

Source: Sammaan Capital Limited Annual Report – FY24, Page-202

Source: ICRA Report – 26th November, 2024, Page-8

As we can see, the 9.10% and the 8.75% redeemable non-convertible debentures are reported at the same value, but the 8.84% and the 9.20% debentures have a variation in the recorded value.

This effect is reflected in the difference between the total of these categories in each report.

In short, the primary reasons for the difference in the value of debt is due to redemption or repayment of some instruments, incorporation of proposed debt, the difference in the debt taken into account in relation to the requirements, the treatment of unused debt, and finally, the difference in the market value of the securities at the date of publishing of each report.