Research By: Navya Sinha

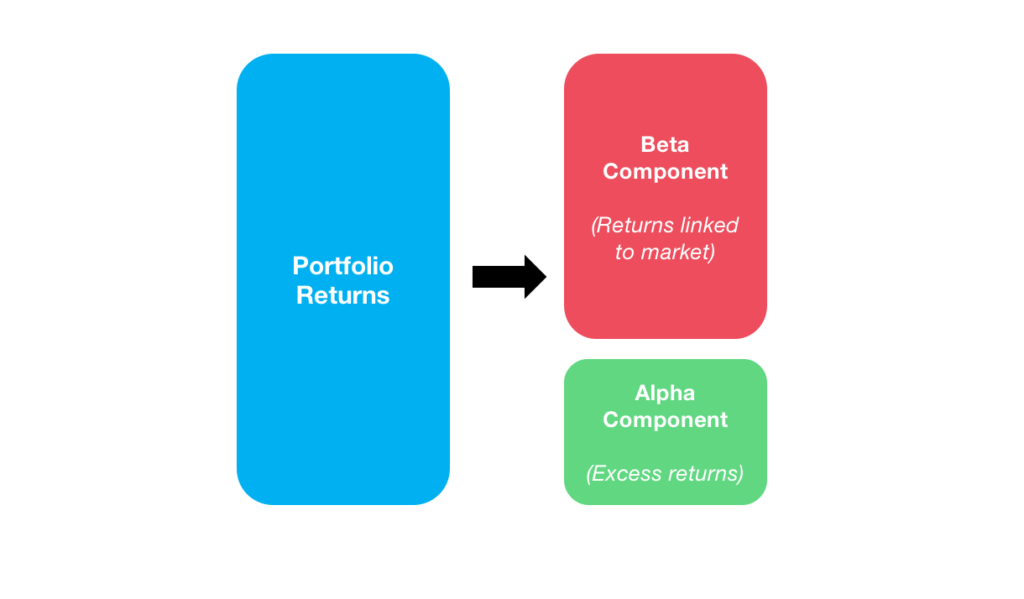

In financial terms, “alpha” refers to a measure of an investment’s performance relative to a benchmark, such as a market index. It indicates how much better or worse the investment did compared to the market as a whole. It represents the value that a portfolio manager adds or subtracts from a fund’s return. Alpha is one of the key performance metrics used in modern portfolio theory and is often used alongside beta, which measures volatility relative to the market. Alpha may be positive or negative and is the result of active investing.

Here’s a more detailed breakdown:

Positive Alpha: If an investment has a positive alpha, it means the investment has outperformed the market or benchmark. For example, if an alpha of +1.0 means the investment performed 1% better than the market.

Negative Alpha: If an investment has a negative alpha, it means the investment has underperformed the market or benchmark. For example, if an alpha of -1.0 means the investment performed 1% worse than the market.

Zero Alpha: If an investment has an alpha of zero, it means the investment performed exactly in line with the market or benchmark.

The concept of alpha came about when weighted index funds were created. These funds try to match the performance of the whole market by giving equal weight to different investment areas.

Alpha is one of five popular technical investment risk ratios. The other four are beta, standard deviation, R-squared, and the Sharpe ratio. These are all statistical measurements used in modern portfolio theory (MPT) and are intended to help investors understand the risk and potential return of an investment. Each measure provides insights into different aspects of the investment’s performance and risk.

To get a deeper understanding, we can use “Jensen’s Alpha” (in honor of Michael Jensen, an economist who developed a method for calculating alpha as part of his work on the Capital Asset Pricing Model). This method takes into account the Capital Asset Pricing Model (CAPM), which adjusts for risk. CAPM uses beta to estimate what the return of an investment should be based on its risk level and overall market returns. By comparing alpha and beta, investors can better evaluate and compare the performance of their investments.

Calculating Alpha

The formula for Jensen’s Alpha is:

α = Ri − [ Rf + βi × ( Rm − Rf ) ]

Where:

Ri = Return of the investment

Rf = Risk-free rate of return

βi = Beta of the investment

Rm = Return of the market or benchmark index

Let’s walk through an example using hypothetical data for a company, say Reliance Industries, and the Nifty 50 index.

We assume that Reliance Industries’ stock returned 15% over the past year and the Nifty 50 returned 12% over the past year. The yield on 10-year Indian Government Bonds is 7% and the beta for Reliance Industries is assumed to be 1.

By applying the formula: α = Ri − [ Rf + βi × ( Rm − Rf ) ]

α = 15% − [ 7% + 1.1 × ( 12% − 7% ) ]

Calculating the Expected Return:

Rm − Rf = 12% − 7% = 5%

βi × ( Rm − Rf ) = 1.1 × 5% = 5.5%

Rf + βi × ( Rm − Rf ) = 7% + 5.5% = 12.5%

Calculating Alpha:

α = 15% − 12.5% = 2.5%

Interpretation: Jensen’s Alpha for Reliance Industries is 2.5%. This means that after adjusting for the risk (beta) and the performance of the market, Reliance Industries outperformed by 2.5%. A positive alpha indicates that the investment performed better than expected based on its risk level, suggesting that the portfolio manager added value.

Significance

Jensen’s Alpha allows investors to determine whether a portfolio manager’s performance is due to skill or simply taking on more risk. A positive Jensen’s Alpha indicates outperformance after adjusting for risk, while a negative Jensen’s Alpha indicates underperformance.

Given the wide variety of investments and how different market conditions can affect returns, it’s important to consider alpha along with other risk-return measures to get a full picture of an investment’s performance.

Other methods to calculate alpha:

- Regression analysis – Alpha can be derived from a regression analysis of the investment returns against the market returns. The regression equation is:

Ri = α + βRm + ϵ

Where:

- α = Intercept of the regression line (representing alpha)

- β = Slope of the regression line (representing beta)

- ϵ = Error term

This method provides a statistical approach to isolating alpha by controlling for market movements and isolating the manager’s contribution.

How do companies use alpha?

- Financial companies, such as asset managers and mutual funds, use alpha to evaluate how well their portfolios or funds are performing relative to a benchmark.

- Financial companies use alpha to assess the effectiveness of different investment strategies.By analyzing the alpha generated by various strategies, companies can determine which strategies are successful and worth continuing or expanding.

- Alpha is used alongside other risk metrics to evaluate and manage the risk-return profile of investments. Understanding alpha helps in balancing the potential for higher returns with the risks involved, aiding in portfolio construction and risk management.

What is a good alpha in finance?

In finance, a “good” alpha typically means that the investment or portfolio has outperformed its benchmark index after adjusting for risk. Here’s what to consider:

Benchmark Comparison: What constitutes a “good” alpha can vary depending on the benchmark and the investment type. For instance, a good alpha for a high-risk, high-reward investment might be different from one for a conservative investment.

Market Conditions: Alpha should be considered in the context of market conditions and the investment’s risk profile. A positive alpha in a challenging market or for a high-risk asset can be especially significant.

Potential drawbacks and limitations to using alpha as a measure of investment performance:

- Alpha is calculated relative to a benchmark index. If the chosen benchmark is not appropriate or representative of the investment’s true risk profile, alpha may provide misleading results.

- Alpha may be more volatile in the short term, making it less reliable for evaluating long-term performance. Short-term alpha swings can be misleading.

Bottom Line

The goal of an investor is to achieve the highest returns possible. Alpha measures how much better an investment performs compared to a benchmark, taking into account the risk involved. Active investors try to earn higher returns than the benchmark and use various strategies to achieve this. Many funds, like hedge funds, focus on generating alpha and often charge high fees for their efforts.