Written By: Nikhil Thapliyal

Consider as an investor, you have a well-diversified investment portfolio having net realized profits exceeding the taxable exemption limit for the financial year, but at the same time some stocks or mutual funds in your portfolio are underperforming. Now, instead of simply accepting the losses, what if you could turn them into a financial advantage? This is where tax loss harvesting comes into play; a strategy used by investors to reduce tax liabilities while at the same time optimizing their portfolios.

Further in this article, we will explore the concept of tax loss harvesting, laws governing it, how it works, its benefits and the potential pitfalls to avoid.

What is Tax Loss Harvesting?

Tax loss harvesting is a strategy that helps investors lower the amount of tax they owe on their profits from investments. It works by selling investments that are currently worth less than what they were bought for, which results in a loss. This loss can then be used to reduce the taxable profits (capital gains) made from other investments.

For example, if an investor makes a profit by selling some stocks but also has other stocks that are losing money, they can sell those loss-making stocks to balance out the profit. This way, they report a smaller total profit to the tax authorities, which reduces the tax they have to pay.

Tax loss harvesting involves three key steps:

– Identifying Loss-Making Investments: Investors review their portfolio and pinpoint securities that are trading below their purchase price.

– Selling These Assets: The loss from the sale of these securities can be used to offset capital gains made during the same financial year.

– Reinvesting in Similar Assets: To maintain portfolio exposure, investors might choose to reinvest in similar but not identical securities, ensuring compliance with tax regulations.

This strategy is commonly used in countries like the United States, where capital gains taxes can be high. In India, investors can also use tax loss harvesting under the country’s tax laws to manage their tax burden effectively. However, they need to be mindful of tax rules, such as set-off and carry-forward provisions, which determine how losses can be adjusted against profits in different financial years.

Understanding India’s Tax Laws on Capital Gains

Before exploring how tax loss harvesting works, it’s imperative to have an understanding of the tax rules that apply to capital gains in India:

– Short-Term Capital Gains (STCG): Profits from selling equity shares or equity-oriented mutual funds held for less than one year are taxed at a flat rate of 20%.

– Long-Term Capital Gains (LTCG): Gains from equity investments held for more than one year are exempt from tax up to ₹1.25 lakh per financial year. Any amount exceeding ₹1.25 lakh is taxed at 12.5% without the benefit of indexation.

– Set-Off Rules: short-term capital losses (STCL) can be set off against both short-term and long-term capital gains, whereas long-term capital losses (LTCL) can only be set off against long-term capital gains

– Carry Forward of Losses: If capital losses cannot be fully utilized in the same year, they can be carried forward for up to eight financial years to offset future capital gains.

These tax provisions allow investors to strategically use tax loss harvesting to reduce their overall tax burden.

How Tax Loss Harvesting Works

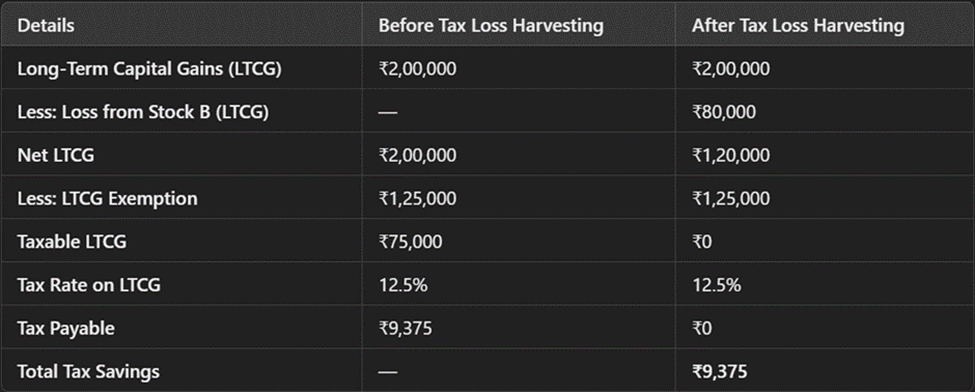

Let’s assume an investor has made a realized profit of ₹2,00,000 from stock sales during the financial year. However, they also have some stocks in their portfolio that are currently at an unrealized loss of ₹ 80,000. To reduce their tax liability, the investor can decide to implement a tax loss harvesting strategy by selling the loss-making stocks before the end of the assessment year.

Given below are the appraisal of the two scenarios regarding this:

Scenario Without Tax Loss Harvesting

– Taxable LTCG: ₹2,00,000 – ₹1,25,000 (exemption) = ₹75,000

– Tax Payable: 12.5% of ₹75,000 = ₹9,375

Even though the investor has an ₹80,000 loss from another stock, if they do not sell it before the financial year ends, they cannot use it to offset their profits. As a result, they end up paying ₹9,375 in tax.

Scenario With Tax Loss Harvesting

Now, if the investor sells the loss-making Stock B before the financial year closes, they can offset this loss against their capital gains:

– Adjusted LTCG: ₹2,00,000 – ₹80,000 = ₹1,20,000

– Taxable LTCG after Exemption: Since ₹1,20,000 is below the ₹1.25 lakh exemption, the taxable LTCG becomes ₹0.

– Tax Payable: ₹0

– Total Tax Savings: ₹9,375

By strategically utilizing unrealized losses, the investor not only brings down taxable capital gains but also saves ₹9,375 in taxes. This example highlights how tax loss harvesting can help investors reduce or even eliminate their tax liability while maximizing tax savings. By strategically selling their loss-making investment, the investor eliminates their tax liability on capital gains, making tax loss harvesting a smart and effective tax-saving strategy.

Benefits of Tax Loss Harvesting

– Lower Tax Liability: Helps investors reduce their tax burden by using capital losses to offset taxable gains, lowering the overall tax payable.

– Portfolio Rebalancing: Provides an opportunity to sell underperforming stocks or funds and reinvest in stronger assets, improving portfolio quality.

– Compounding Advantage: The money saved from lower taxes can be reinvested, allowing it to grow and generate more returns over time.

Wrong Practices to Avoid in Tax Loss Harvesting

– Wash Sale Rule Violation: While repurchasing the same asset isn’t explicitly prohibited in India; frequent trades may attract tax scrutiny. Consider waiting before rebuying or opting for a similar but different asset.

– Excessive Trading for Tax Benefits: Frequent buying and selling to exploit losses can lead to higher transaction costs, reducing the actual tax advantage.

– Ignoring Exit Loads & STT: Selling mutual funds may incur exit loads, and stock sales involve STT, which can impact overall savings.

– Disrupting Investment Goals: Selling solely for tax benefits may harm long-term portfolio strategy. Ensure tax loss harvesting aligns with financial goals.

In conclusion, tax loss harvesting can be a useful strategy for investors looking to optimize their tax liabilities. However, it should be implemented carefully to align with long-term financial goals. Investors must also stay compliant with tax regulations to avoid potential legal issues. By incorporating tax loss harvesting into financial planning, investors can take advantage of market downturns while ensuring compliance with tax regulations. If used wisely, this strategy can serve as a powerful tool for tax-efficient investing.