Written By: Nishant Parsad

When financial markets turn volatile, investors often scramble to protect their money. While many rush to find “safe investments”, the smartest investors know that avoiding bad investments is just as crucial as picking good ones. Imagine you’re walking through a street filled with open manholes. The key to safely getting to the other side isn’t just about choosing the right path – it’s about avoiding the dangerous holes in the ground.

Similarly, in uncertain times, knowing which sectors and companies to avoid can save you from major financial losses. In this article, we’ll break down industries that become particularly risky during economic downturns and highlight safer alternatives.

Banks with High Exposure to Real Estate and Commercial Vehicles

Banks are the backbone of any economy, but some carry far more risk than others – especially those heavily involved in real estate and vehicle loans. When a financial crisis hits, these are often the first loans to turn bad.

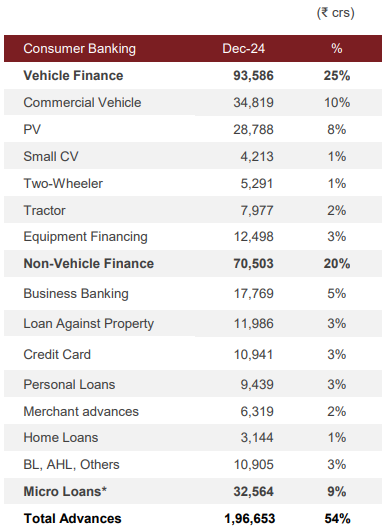

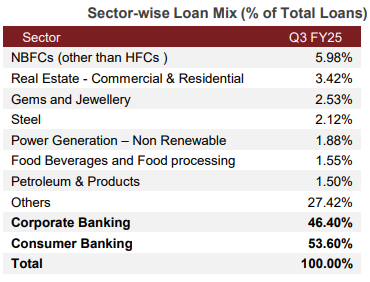

Take IndusInd Bank and RBL Bank as examples. IndusInd Bank has about 3.42% of its loans tied to real estate and 25% of its loan book in vehicle finance (including three-wheelers and commercial trucks) (as of Q3-FY25). Imagine an economic slowdown—builders struggle to sell homes, transport businesses cut costs, and defaults rise.

A lesson from history: During the 2008 global financial crisis, banks heavily exposed to real estate collapsed under bad loans. Even in India, many financial institutions with real estate exposure faced serious liquidity issues. Today’s investors should be wary of banks with large loan books in these vulnerable sectors.

Small Finance Banks and Microfinance Institutions

Small finance banks and microfinance institutions play a crucial role in lending to small businesses and low-income borrowers. However, their greatest strength—the ability to lend without collateral—is also their biggest weakness during downturns.

Consider Bandhan Bank, a major microfinance player in India. During protests in Assam, the bank’s collection efficiency fell from 88% to 78% (in 2021), showcasing how quickly external disruptions can hurt financial stability. When the economy slows, borrowers with unsecured loans—who often rely on daily earnings—fail to repay, creating a chain reaction of defaults.

These institutions may thrive during stable times, but in a financial crisis, they can become some of the riskiest bets for investors.

Public Sector Undertakings (PSUs): Profits vs. Politics

Public Sector Undertakings (PSUs) might seem like safe bets because they have government backing, but that’s exactly where the problem lies. Many PSUs are forced to prioritize social and political goals over profitability, making them vulnerable during financial crises.

Look at companies like Indian Oil, ONGC, Coal India, and NTPC—they often have to sell products at government-regulated prices, even if it leads to losses. Similarly, PSU banks frequently lend to politically influenced projects that may not generate strong returns.

During economic downturns, governments might impose fuel subsidies, price caps, or forced lending to support struggling industries, further eroding profits. Investors looking for stability should approach PSUs with caution during turbulent times.

Highly Leveraged Sectors: The Danger of Debt

Some industries thrive on borrowed money during good times, but when a downturn hits, their high debt levels become a massive burden.

– Airlines: Fixed costs like aircraft leases, fuel, and salaries don’t disappear even when flights are grounded. The COVID-19 pandemic highlighted how airlines can burn through cash rapidly.

– Hotels: With high overhead costs, hotels struggle when occupancy drops. During crises, business and leisure travel take a massive hit, making hospitality a risky sector.

– Hospitals: While essential, hospitals operate on high capital costs. During financial downturns, delays in payments and fewer elective procedures can strain cash flows.

For investors, these businesses might seem attractive due to their size and demand, but during crises, their financial structures make them vulnerable to significant losses.

Auto and Auto Ancillary Companies: First to Feel the Pain

Buying a car isn’t a necessity—it’s a luxury for most consumers. When the economy slows, people postpone big purchases, making the automobile sector one of the first to suffer.

Companies like Tata Motors and Motherson Sumi are heavily dependent on consumer demand and global supply chains. Any disruption—whether from market slowdowns, chip shortages, or inflation—can send auto stocks plummeting.

Investors should be wary of automobile companies during downturns, as their sales cycles closely follow economic trends.

Real Estate and Property Businesses: High Risk, Low Reward

During financial downturns, real estate becomes one of the riskiest sectors. People delay buying homes, companies put off office expansions, and property developers get stuck with unsold inventory.

The 2008 housing crisis in the US is a classic example of how overleveraged real estate markets can collapse. In India, high-debt real estate companies often struggle when market demand falls, making them a risky choice for investors during economic slowdowns.

Unsecured Lending Companies: A Recipe for Defaults

Unsecured lending—loans without collateral—can be incredibly profitable in good times but disastrous in a crisis. When borrowers start defaulting, these companies have no assets to recover their money.

Many microfinance institutions fall into this category. Since they serve economically weaker sections, their loan books are highly sensitive to income shocks. Investors should approach these businesses with caution, especially during periods of financial instability.

Defensive Sectors to Consider During Financial Crises

Not all industries crumble during a crisis. Some sectors remain stable because people continue using their products and services no matter how bad the economy gets.

– Consumer Staples: Companies like Nestlé, Hindustan Unilever, and Procter & Gamble provide essential goods—food, hygiene products, and cleaning supplies. These products are non-negotiable, making these companies stable investments.

– Healthcare and Pharmaceuticals: Companies like Johnson & Johnson, Sun Pharma, and Dr. Reddy’s offer medicines and medical services, which are always in demand. The healthcare sector provides strong protection during downturns.

– Utilities: Firms like NTPC and Tata Power provide electricity and water—essential services that people continue using regardless of economic conditions.

– Gold and Precious Metals: Gold has long been considered a safe-haven asset during financial turmoil. Companies in the gold mining and precious metals space, like Newmont Corporation and Hindustan Zinc, tend to perform well when other industries decline.

Tools and Resources for Tracking Sector Performance

Successful investors rely on trusted data sources to track market movements and sector performance. Here are the best resources for getting accurate and timely information:

📌 Government Reports: The Reserve Bank of India (RBI) and Ministry of Finance publish sector-specific financial stability reports. These documents provide real insights into industry health and risks.

📌 Stock Exchange & SEBI Disclosures: The NSE, BSE, and SEBI release regular updates on sectoral performance and regulatory changes that affect businesses.

📌 CMIE Industry Reports: The Centre for Monitoring Indian Economy (CMIE) offers detailed sector-wise data, from industrial output to profitability metrics.

📌 Sector-Specific Government Portals: Resources like IBEF, Invest India, and NABARD provide sectoral growth projections, investment opportunities, and credit reports on industries like agriculture, MSMEs, and infrastructure.

📌 International Reports: Organizations like the World Bank and IMF offer global macroeconomic insights, helping investors gauge broader market risks.

By using these resources, investors can base their decisions on solid, data-backed insights rather than speculation.

Investment Philosophy: Learn to Avoid, Not Just Find Legendary investor

Charlie Munger often said, “Invert, always invert,” meaning that instead of just looking for what to invest in, also think about what to avoid. During financial crises, this advice becomes even more valuable. Avoiding high-risk sectors can often save you more money than chasing risky high returns. By staying away from highly leveraged companies, PSUs with government interference, microfinance institutions with unsecured loans, and industries that depend heavily on economic stability, investors can keep their portfolios safe during market downturns.

Conclusion

Financial crises and market volatility are part of investing, but big losses don’t have to be. By avoiding sectors like highly leveraged businesses, PSUs influenced by politics, microfinance institutions, and industries with high fixed costs, you can build a portfolio that survives and even thrives during tough times. In investing, sometimes the best strategy is to avoid the wrong moves. Knowing which sectors to steer clear of during financial crises is just as important as knowing where to invest. Stay smart, stay safe, and let your portfolio weather any storm!