NSE: ANGELONE

Income Statement

Balance Sheet

Cash Flow Statement

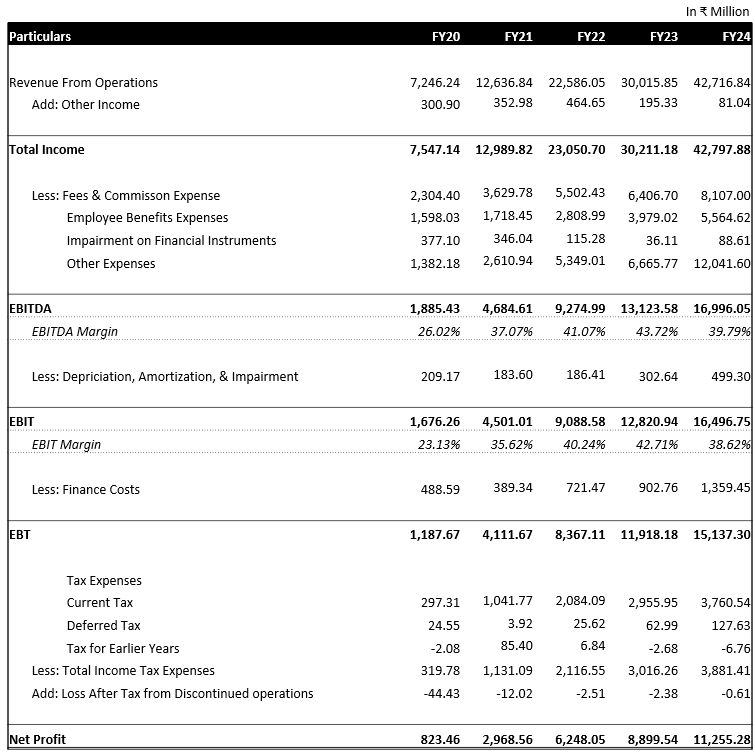

Commentary on Statement of Profit & Loss:

I. Revenue from Operations

Interest Income

• ANGELONE’s interest income grew by 51.38% YoY in FY24, as opposed to 56.09% in FY23 and 88.1% in FY22. The interest income in FY24 comprised interest on Fixed Deposits with the bank interest from client funding and delayed payments.

• ₹5 billion of the total interest income was from interest on Fixed Deposits with banks, 77% of which was attributed to client funds. This income increased from ₹2.6 billion in FY23, showing a 95.09% increase in FY24, as the company has been gradually increasing its funds deposited with banks. This indicates that the company has a stable stream of passive income.

• The rest of approximately ₹2.8 billion was interest from margin funding and delayed payments which grew by 9.92% in FY24 as opposed to 1.48% in FY23. The same income saw a spike in growth rate in F22 when it grew by 111.47% because the company’s average client funding books grew by 108.3% YoY.

• During November of 2024, the company reduced its margin interest charge from 18% to 14.99%, in order to increase its client funding books and match their competitors. ANGELONE believes this change will help in expanding its market share in the MTF segment.

Fee & Commission Income

• The fee and commission income grew by 40.52% in FY24 from ₹24.8 billion in FY23 to ₹34.8 billion. The largest contributor to this, the brokerage income, which accounted for 68.3% of the total revenue, grew by 40.2% on YoY basis in FY24 after 32.21% in FY23. This rate saw a sharp decline after experiencing growth of 79.9% and 73.59% in FY21 and FY22, respectively, even though the income was increasing. This income is expected to keep on increasing in the long-run, due to the large number of new people, who have entered and will enter the capital markets that prefer online discount brokers.

• Moreover, both income from depository operations and distribution operations saw a decrease of -20.78% and -3.29% respectively on a YoY basis in FY23, but in FY24 they both increased by 56.43% and 32.16%. Both these incomes have remained stable through the years, relying consistency of these operations.

• The company’s other operating income grew by 37.92% YoY in FY24 to ₹3.6 billion, in which ₹3.5 billion was contributed by ancillary transaction income.

Future Outlook:

• The company’s revenue from operations has been growing with a CAGR of 55.82% for the last 4 years, and in relation to future growth, the company is expected to increase its revenue at roughly 30% – 40% CAGR.

• Due to the increased margin requirements for customers in the F&O segment, the company’s funds with the banks might increase, leading to an increase in the interest income. On the other hand, the income from lending activities might see a slight decline due to these same restrictions. To offset this effect on the revenue, the company has introduced interest on disproportionate non-cash collateral offered as margin exceeding ₹50,000.

• The fee and commission income, mainly the brokerage income will see an even further uptick for the company, as the number of demat accounts in India almost quadrupled from 4 crore in FY20 to about 15 crore in FY24. 5 With the company’s strong acquisition and retention rate, ANGELONE will surely expand its customer base further and increase its market share in the coming years.

• The ancillary transaction income will be the most negatively impacted due the introduction of the true-to-label transaction costs by SEBI. The company has introduced brokerage on cash delivery segments in order to minimize this impact.

• Additionally, in the light of these new SEBI regulations, the company expects a short-term slow down in trading volumes and continues to monitor client behavior but believes that these regulations will strengthen the market in the long-term. The management conveyed that the company expects a short-term impact of 13%-14% to be felt on the total income from clients. The management has also said it will focus on diversifying its revenue streams and acquiring more market share in order to minimize any decline in profitability due to the SEBI regulations and the overall cyclical nature of the broking industry.

• In short, the broking revenue are expected to continue to rise at a good pace, as ANGELONE has implemented a couple of new policies to offset the effect of the new SEBI regulation that might affect revenue.

II. Expenses

Fee and Commission Expenses

• ANGELONE saw an increase in the fees and commission expense in the FY24, where it rose from ₹6.4 billion in FY23 to ₹8.1 billion, representing a 26.54% increase.

• This change was heavily influenced by the increase in pay-out for the company’s network of Authorized Personnel and Digital Referral Associates (DRAs), who are owed a part of the revenue earned from clients acquired through them. The growth in the company’s client base facilitated a huge rise in its ADTO which increased by 143.5% to ₹33.2 trillion which finally led to the increase in the fee paid to these Authorized Personnel and DRAs.

Employee Benefit Expenses

• The employee benefit expenses saw an increase of 39.85% YoY in FY24 and this growth rate has been gradually decreasing after spiking in FY22 at 63.46%.

• These expenses saw a rise due to the increase in staff as well as salaries and new hires regarding expansion into the asset management and wealth management segments, coupled with stock option grants at a higher cost.

Other Expenses

• The company noted an increase in other expenses, which rose from ₹6.7 billion in FY23 to ₹12 billion in the FY24, representing an 80.65% YoY increase.

• The biggest part of these other expenses, which account for about 61.67% of it was the spends on advertisement and publicity which amounted to ₹7.4 due to the increase in gross client acquisition and the number of orders. These expenses also included the costs of about ₹0.23 Billion relating to the Indian Premier League sponsorship.

• Next, 18.34% of these expenses were gone towards software connectivity license and maintenance.

• Exchange and statutory charges grew from approximately ₹267 million in FY23 to about ₹669 million in FY24, indicating an increase of 150.82%.

• The rest of the expenses were accounted for though increased demat charges to depository due to higher client activity in the cash delivery segment, legal and professional charges and increase in CSR spends.

Future Outlook:

• Taking into account these changes, the expenses for the company have a change of growing at a rate of 15% – 20% CAGR.

• As an after effect of the increasing client base, the fee and commission expenses will increase as more clients get acquired through referral, hence, increasing the fee paid to Authorized Personnel and DRAs.

• Moreover, with the ongoing expansion of the company into asset management and wealth management, more professionals who hold expertise in these fields will be onboarded, resulting in an increase in employee benefit expenses in the near future.

• The advertisement and publicity expenses, under the other expenses head, are expected to increase as the company plans on expanding into asset management and wealth management, which will require ANGELONE to increase its spending on advertising and publicity.

• Overall, ANGELONE’s expenses will see an increase due to onboarding of new client and the expansion of the company into new business segments.

III. EBITDA

• The EBITDA of the company grew from around ₹13 billion in FY23 to about ₹17 billion in FY24. The company’s EBITDA growth rate has been gradually decreasing as in FY21 it grew at a rate of 148.46% but in FY23 and FY24, it grew by just 41.49% YoY and 29.51% YoY, respectively.

• The EBITDA margin reduced from 43.72% in FY23 to 39.79% in FY24. This reduction in margin is partially related to the increase in the impairment on financial instruments expenses, which were decreasing from FY20, but increased by 145.39% YoY to approximately ₹89 million and the increase in other expenses.

• Future Outlook: The EBITDA is expected to experience growth of approximately 20%-25% CAGR for a short period, then, as the new business segments start to generate revenue, it is expected to rise higher, leading to an increase in the EBITDA margin, as the company has to incur expenses to set up their potential revenue drivers before they start to generate revenue.

IV. EBIT

• The EBIT of the company, which grew from ₹12.8 billion in FY23 to ₹16.5 billion in FY24 represented a growth rate of 28.67% YoY.

• The company’s EBIT margin reduced from 42.71% in FY23 to 38.62% in FY24, as an effect of the decrease in the EBITDA margin.

• Future Outlook: Same as the case for EBITDA, the EBIT is also expected to be have a growth of approximately 20%-25% CAGR in the short run and then rise higher as an after effect of the EBITDA. The EBIT margin is expected to increase gradually as well.

V. EBT

• The company’s EBT increased to approximately ₹15 billion in FY24 from about ₹12 billion in FY23. This number has also seen a decrease in growth rate over the past five years. This EBT increased by 42.44% YoY in FY23 but in FY24, it grew by just 27.01%.

• Future Outlook: Taking into account the YoY growth rate of the company, in addition to the increase in finance costs due to possible additional debt financing, the EBT of the company is also expected to grow at a CAGR of 20%-25% in the future.

VI. Tax Expenses

• The total income tax expenses grew by 28.68% to ₹3.9 billion, mostly constituting of current tax expenses of about ₹3.8 billion. This growth rate has also been decreasing over the years. Moreover, this expanse has been gradually increasing, mirroring the income of the company.

VII. Net Profit

• Finally, the Net Profit for the company grew to ₹11.3 billion in FY24, indicating a growth rate of 26.47%, from ₹8.9 billion in FY23. This growth rate, same as the growth rate for EBITDA and EBIT, has been decreasing over the years.

• The net profit is increasing in line with the income of the company through the years and has been showing a consistent growth in net profit margin though FY21 to FY23, only decreasing slightly by -11.13%, resulting in a margin of 26.35%.

• Future Outlook: Overall, the company’s net profit has been growing at a CAGR of 92%, and with the changes the company has implemented to curb the effect of the new SEBI regulations coupled with their plans to expand their business segments and goals to increase market share, the Net Profit is sure to see good growth in the coming years.

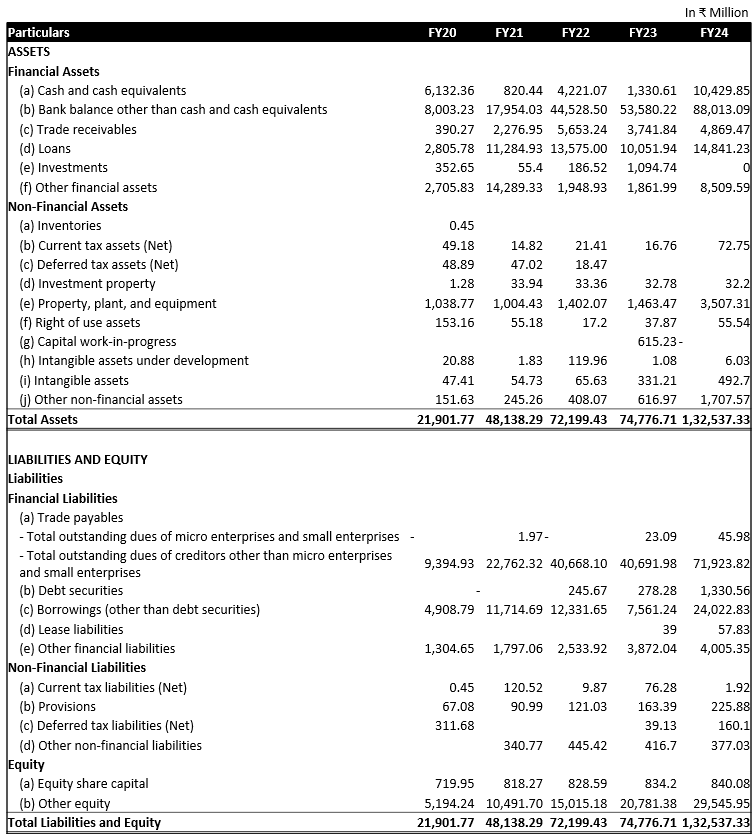

Commentary on Statement of Balance Sheet:

I. Assets

Financial Assets

• Cash and Cash equivalents constituted 7.87% of the total asset and grew from about ₹1.3 billion to approximately ₹10.4 billion in FY24, increasing almost 8x. This increase was led by an increase in client’s margin, along with cash generated from business operations. During the year, the company’s client funding book increased by 54.1% to almost ₹18 billion, which in turn increased the company’s balances with the banks. Taking into account the new regulations by SEBI, which increased the value of margin requirements, this balance will possibly multiply further. Moreover, this hefty rise has improved the liquidity position of the company.

• Next, 66.41% of the total assets was bank balance other than cash and cash equivalents. These balances amounted to about ₹88 billion, increasing by 64.26% YoY. This increase was led by short-term fixed deposits with banks and has been relatively stable for the past three years. These deposits also add to the company’s position to meet short term demands for cash.

• During the year, the company decided to liquidate its investments, decreasing the amount of about ₹1.1 billion in FY23 to nil in FY24.

• Loans given amounted to about ₹14.8 billion on the company’s balance sheet, increasing by 47.65%. This was mainly led by the growth in the client funding segment of the company’s business. As mentioned, ANGELONE’s margin trading books increased by 54.1%, but due to the higher margin requirements, this number might see a small dip for a short period of time.

• The company’s other financial assets grew almost 4.6x to about ₹8.5 billion. During the year, the security deposits kept with stock exchanges increased to ₹8.1 billion, leading to this sudden increase.

Non-Financial Assets

• The non-financial assets of the company have seen steady growth in the last three years, amounting to a total of approximately ₹5.9 billion, representing an 88.55% YoY increase.

• This increase was led by the rise in plant, property and equipment, which grew by almost 2.4x reaching ₹3.5 billion. The reason for this was the addition of new computer equipment to grow the company’s investment in its technological infrastructure. This is a smart move by ANGELONE, as due to the extremely competitive nature of the online discount broking industry, there is a need for the company to continuously bring innovative technological advancements.

• The other non-financial assets of the company grew to be about ₹1.7 billion at the year end, increasing by almost 2.8x. The increase in prepaid expanses and advances to venders by the company, coupled with the balances with government authorities facilitated this increase.

Future Outlook: The company’s total assets have been growing at a CAGR of 56.84% for the last 4 years and in the future, this growth is expected to continue as the growth in ANGELONE’s MTF book will increase the bank balances of the company, along with cash and cash equivalent and trade receivables. Moreover, the company might have to invested in more plant, property and equipment due the plans for expansion into asset management and wealth management.

II. Liabilities & Equity

Financial Liabilities

• The company’s trade payables accounted for almost 70.5% of the total liabilities, amounting to approximately ₹72 million. This represented the balances of client’s funds with clearing corporations as margins. Moreover, the majority of these trade payables were aged less than one year.

• The total borrowings of the company including debt securities increased by about 3.2x, coming to a total of approximately ₹25 billion. The company issued commercial paper during the year making its year end balance increase from ₹278.28 million in FY23 to about ₹1.3 billion in FY24. Additionally, the overdraft balance of the company with banks amounted to almost ₹4.8 billion and working capital demand loans from banks and NBFCs equaled to approximately ₹19.2 billion. This need for increase in borrowing for the company rose due to the increase in client funding book, couple with the margin obligation with clearing corporations. In the future, as ANGELONE is planning on expanding into new business segments and also keep up the robust growth in its client funding facilities, these borrowing might see an increase due to rise in need for capital investments and working capital demand.

Non-Financial Liabilities

• The total non-financial liabilities have been steadily increasing though the years, amounting to about ₹765 million in FY24. This number was made up of majorly other non-financial liabilities and provisions. The other non-financial liabilities were mostly relating to statutory dues payable.

Equity

• The total equity of the company amounted to ₹30.4 billion at the year end form ₹26.6 billion in FY23, representing a 40.57% YoY increase. This increase was facilitated by a 42.18% YoY increase in other equity of the company, which amounted to about ₹29.6 billion.

• This was due to the rise in retained earing of the company, which increased from about ₹15.7 billion in FY23 to ₹23.7 billion in FY24, reflecting the company’s plan for expanding into the asset management and wealth management services. Additionally, this conservative dividend policy implies ANGELONE’s confidence in increasing the overall value for its Shareholders.

Future Outlook: Mirroring the total assets, the company’s liabilities and equity is also expected to increase due to the rise in components such as, borrowings and trade payables in relation to the expansion of business segments and the impressive growth in the MTF book, leading to increased working capital requirements for the company.

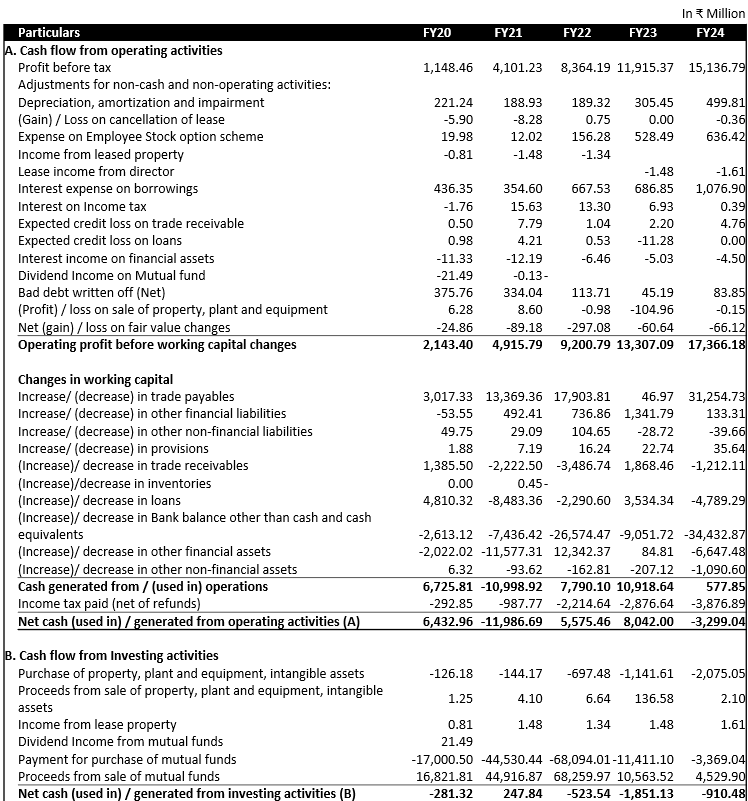

Commentary on Statement of Cash Flow Statement:

I. Cash Flow from Operating Activities

• The net income used in operating activities amounted to about ₹3.3 billion at the year end as compared to a positive cash generated in FY23 of ₹8 billion.

• Furthermore, the operating profit before working capital changes amounted to a positive of approximately ₹17.4 billion, heavily influenced by the interest expense on borrowings, because the borrowings of the company, as mentioned in the commentary on balance sheet, increased by about 3.2x to ₹25 billion.

• Next, the expense on employee stock option plan also increased by 63.63% on an YoY basis because, as mentioned in the commentary for profit and loss, the company’s employee benefit expenses grew by 39.85% during the year.

• The total changes in working capital came to be about a negative ₹16.8 billion, majorly influenced by the increase in trade payables and bank balances other than cash and cash equivalent.

• Again, as mentioned earlier, the trade payables for the company grew by about 76.76% YoY, increasing by about ₹31.3 billion. Moreover, the bank balances other than cash and cash equivalent increased by ₹34.4 billion or by 64.26% YoY.

• Finally, the income tax paid, net of refunds came to be about ₹3.6 billion, as also mentioned in the commentary for profit and loss.

• Future Outlook: As an after-effect on all the items of the profit and loss statement and the balance sheet, the cash used in operating expenses will see a probable increase due to the expansion plans.

II. Cash Flow from Investing Activities

• The net cash used in investing activities totaled to be about ₹910.5 million in the FY24.

• This amount was influenced by the payment for purchase and proceeds from sale of mutual funds, which were approximately ₹3.4 billion and ₹4.5 billion. The net of these two activities came to be about roughly ₹1.2 billion at the year end.

• Next, the purchase of property, plant and equipment along with purchase of intangible assets came to be about a negative of about ₹2 billion. This number was due to the reason discussed earlier for the company to increase its investments in technological infrastructure and commissioning of data center and disaster recovery sites.

• Future Outlook: Same as cash used in operating activities, the cash used in investing activities is also likely to increase due to investments in plant, property and equipment for the earlier mentioned reasons.

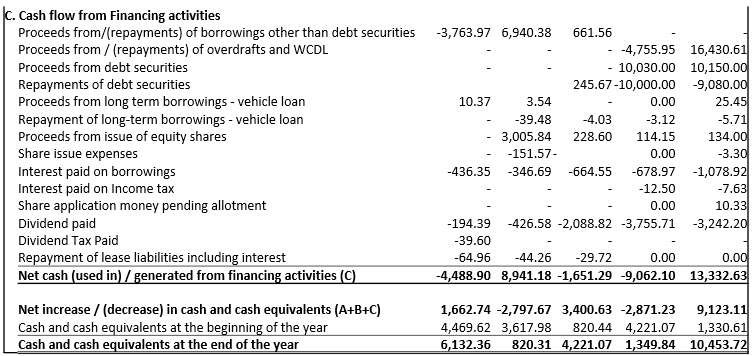

III. Cash Flow from Financing Activities

• The cash generated from financing activities equaled to a positive of about ₹13.3 billion at the year end.

• This was majorly influenced by the proceeds from borrowings other than debt, coupled with overdrafts and working capital demand loan (WCDL) which totaled to about ₹26.6 billion. This increased in borrowings, again, is related to the increase in working capital requirements and need for funds due to expansion of the client funding business and the company’s plan to diversify into new business segments. Moreover, the interest paid on borrowings cost the company about ₹1.1 billion.

• The company paid a dividend of about ₹3.3 billion and raised ₹134 million through the issue of equity shares.

• Future Outlook: The company’s cash generated from financing activities is expected to increase, mainly influenced by the possible increase in proceeds from debt securities.

IV. Cash and Cash Equivalent

• In total, the cash and cash equivalents for the company grow almost 8x, from ₹1.3 billion at the end of FY23 to ₹10.4 billion at the end of FY24.

• Future Outlook: Overall, after taking into account all the changes, the cash and cash equivalent of the company is expected to experience a net increase.