Capital Market

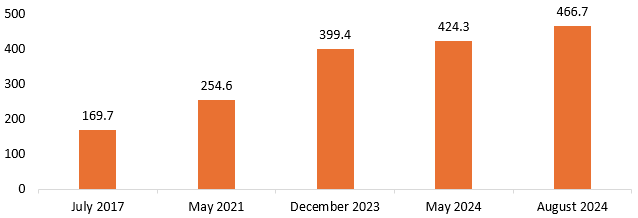

Equity Market 5: As of 30th August, India’s Market Capitalization stood at an incredible ₹466.7 trillion, ranking it the fourth-largest country globally. This astonishing growth was seen through December 2023, when the number was at ₹399.4 trillion to May 2024, when it increased by another trillion to ₹424.3 trillion and finally increased in just three months by half a trillion dollars. India’s market capitalization is said to likely increase to ₹848.6 trillion by 2030.

Both benchmark indices, Nifty and Sensex achieved high milestones in the FY24 of 22,526 and 74,245, while for the current fiscal year, both indices have touched all-time peak of 25,000 and 82,000 mark, respectively.

Regardless of these impressive numbers, the Indian market is said to be overvalued due to overly bullish retail investors. The Buffett Index for the Indian Market, which is nothing but the value of all listed companies in ratio to the country’s GDP, rose from its historical average of 0.83 to about 1.4. The revenue for the broking industry is immensely related to the conditions of the overall Indian market.

Exhibit 1: The massive increase in the Market Capitalization of India from about ₹170 trillion in July 2017 to ₹467 trillion in August 2024 provides impressive future growth prospects (In ₹ Trillion)

Source: The India Express

Derivative Market 6

The Indian derivative market has experienced immense growth, where more than 36.8 billion equity index options were recorded to have been traded at the NSE and BSE in Q2 of FY24. The monthly notional value of derivatives traded was almost ₹11 trillion in August, having the highest number globally. 8 The share of retail investors in India’s overall derivative trading volumes grew from about 2% in FY18 to about 41% in FY2, while the number of trading accounts rose by 4x from 36 million in April 2019 to 154 million in April 2024. 9

The rise of discount brokers and online trading facilities has led to a huge increase in the number of active derivatives traders in India, rising by about 8x from under 0.5 million in 2019 to over 4 million in October 2024. 10

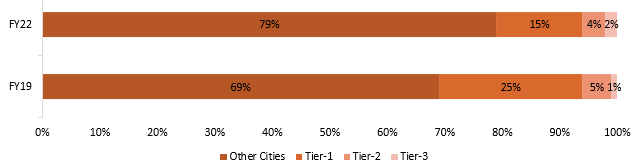

Exhibit 2: Derivative Trades diversified over Cities regarding All Individual Trader activity in FY22 shows a combined contribution of 94% from tier-3 and other cities, showing their dominance

Source: SEBI Report

A SEBI report showed that 99.8% of the total traders in the equity F&O segment were individual or retail traders. 11 SEBI also recorded an increase in participation from Tier-3 cities increased by 1% and the cities beyond Tier-3 had a rise in participation from 69% in FY19 to 79% in FY22.

Despite these massive numbers, SEBI’s study showed that 93% of individual traders in the equity F&O segment had losses averaging ₹2 lakh during FY22-FY24. 12

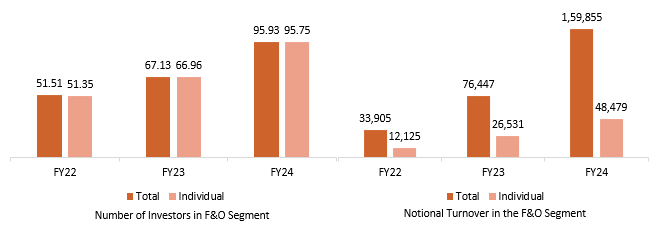

Exhibit 3: The share of Individual or Retail Investors in the Equity Futures & Options in FY23 was approximately 30% showing an immense rise in Individual participation (In ₹ Lakh Crore)

Source: SEBI Report

This has led to SEBI issuing restrictions to increase the minimum contract size, increasing the lot size, introducing extreme loss margin, limiting weekly expiring contracts to 1 per exchange, and revising the exchange transaction charges and STT to curb the retail trading activity in the index derivative market. These restrictions might lead to a decrease in the number of clients for brokers, which in turn will affect the broking revenue earned from these derivative trades. Furthermore, due to an increase in contract and lot size, broking houses might increase their margin requirements for clients. 7 13

On the other hand, the restrictions introduced by SEBI in order to curb the losses for retail investors might help their financial health in the long run, increasing the vitality of the market.

Retail Equity 14 15 16 17: The number of registered investor base at NSE rose by almost 3x from FY20 to 9.2 crore in FY24. The number of Demat accounts in India has also increased drastically from 4 crore in FY20 to 15 crore in FY24, representing an almost a 4x growth with 3.2 crore opening in just FY24 with the number of active clients also increasing by 4.18 crore.

This rise in number has been associated with the rise of discount brokers and the technological advancement in this field. The Economic Survey 2023-24 stated that the share of retail investor in the equity cash segment turnover was at 35.9% in the FY24.

The share of domestic institutional investors (DII) combined with retail investors increased from 58.7% in March 2019 to 62.9% in March 2024. 18 This increase signifies growth in the risk appetite of the domestic population and the rise in financial literacy among the people. Moreover, the growth in technology, AI-ML sectors, along with an increase in the geographical reach and ease in the use of digital platforms also plays a significant role in this growth.

Although this growth is extremely impressive, the Economic Survey 2023-24 of India has also cautioned that the significant rise of retail participation in the stock market with the expectations of higher returns without the real market conditions to back is up is concerning.

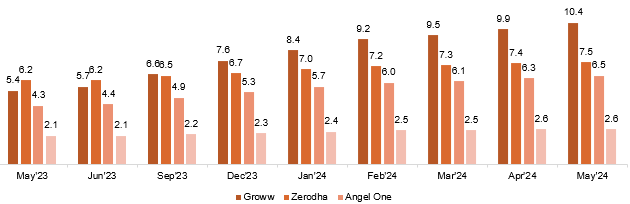

Exhibit 4: The number of NSE Active Clients for the Top 4 brokers in India from May 2023 to May 2024 shows an increase from 18 million to 27 million in the number of clients (In Million)

Source: MOFSL

Broking Industry

Discount Brokers: The market share of the top 5 discount brokers increased from 58.1% in July 2022 to 64.6% in July 2024. 19 As access to technology is continuously increasing in India, the client base is actively shifting towards discount broking houses which provide a simplified pricing structure and are lower in cost. 20 Discount brokers are also increasingly expanding into Margin Trading and Cross-selling segments in order to diversify and increase their revenue streams. These discount-broking houses which offer a diverse portfolio of services online through a digital platform are especially attractive to young, tech-savvy investors. Moreover, these online discount brokers are more available and accessible to retail and individual investors, as opposed to traditional, full-service, or institutional brokers.

With the rising number of Demat accounts and the increase in active investor base in India, the demand for discount broking is set to increase as a younger client base coming from tier-3 and beyond cities joins the market.

According to Crisil, discount brokers might be negatively impacted by the introduction of the new F&O regulations by SEBI much more than full-service brokers as derivative trades account for approximately 95% of total trading volumes for them and it is also the biggest contributor to their revenue mix, accounting for about 60% to 80% of the broker’s total revenue. 21