Consumer Durable Sector

Consumer durables are products that are used for domestic use and have an extended lifespan. Goods and appliances such as Televisions, Washing machines, Air conditioners, Kitchen appliances, and Cell phones fall into this category. The consumer durable business in India’s projected growth of CAGR 4.7%by 2027 reaching US$ 77million. {6}

The Consumer durables industry in India is segmented as;

• Brown Goods – Consumer electronics (TV, DVD players, stereos)

• White Goods – Consumer household appliances( refrigerators, washing machine, dishwasher , dryers, etc.) {6}

The white goods market is estimated to cross $21 Bn in 2025 expanding at a CAGR of 11%. Domestic manufacturing contributes nearly $4.6 Bn on average to this industry.{7}

Market size

• Indian appliance and consumer electronics Industry market size is approximately Rs. 1.48 lakh crore (US$ 17.93 billion) by 2025. By 2025, India’s consumer electronics and appliances industry is predicted to be the 5th largest in the world.

• India’s consumer electronics and home appliances market is set to grow by US$ 2.3 billion between 2022 and 2027, registering a CAGR of 1.31%. {6}

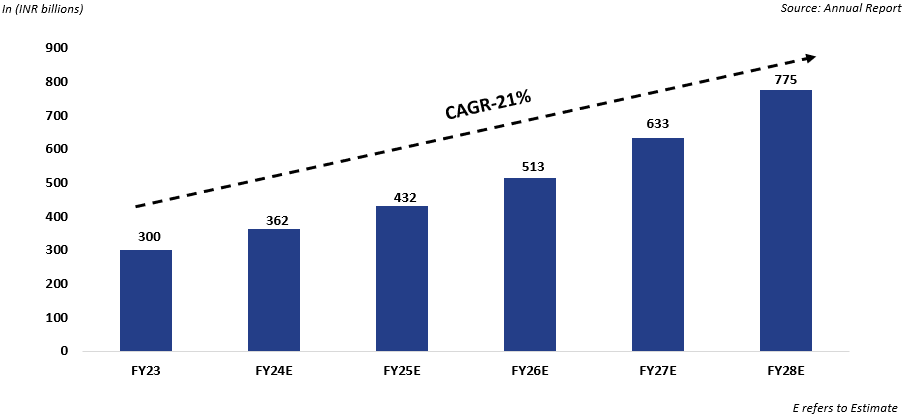

Exhibit 1: The Indian consumer durables ODM market in FY23-FY28E growing with a CAGR of 21%.

Contribution of the Consumer Durable Sector in the Indian GDP:

• India’s consumer durables sector, currently contributing 0.6% to the nation’s GDP, which is projected to grow at a compound annual growth rate (CAGR) of 11%, reaching US$ 35.73 billion (Rs. 3 lakh crore) by 2029.

• The sector’s GDP contribution is expected to increase by 1.5 times, aiming to become the fourth-largest market for consumer durables by 2027 and the global leader in this industry by 2030 while also creating 500,000 new jobs.{8}

Indian Air Conditioner Market: {9}

• The global air conditioner market size & share was valued at USD 143.86 billion in 2023 and is expected to grow at a CAGR of 6.10% during the forecast period.

• The market’s anticipated growth can be credited to robust expansion in the residential sector with home sales reaching Rs. 3.47 lakh crore ($42 billion), a 48% year-on-year increase and a 36% volume increase. {10} Which represents the primary end-user of air conditioners. Improved standards of living among Indian consumers have significantly increased the demand for air conditioners in residential settings. Additionally, the commercial sector, another key end-user, has experienced substantial growth over the past decade.

• Over the last five decades, India has experienced more than 700 heatwaves, with experts suggesting that this summer’s extreme and persistent heat ranks among the most severe. According to the Council on Energy Environment and Water (CEEW), 97% of Indian households have electricity, and 93% rely on fans for comfort. However, the year 2024 has seen an unprecedented surge in India’s air conditioning market. Sales of air conditioners are expected to increase by 60% from March to July, compared to the typical 25- 30% growth in previous years.

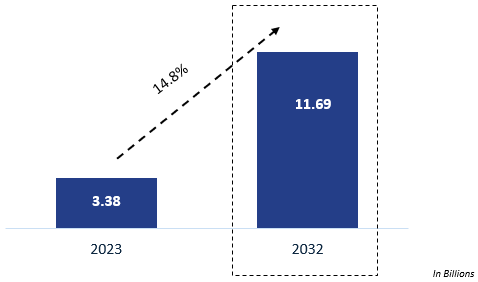

Exhibit 2: Capitalizing on 14.8% CAGR growth in the Indian air conditioner market.[11}

Growth Prospects in the Global Commercial Refrigeration Market {12}

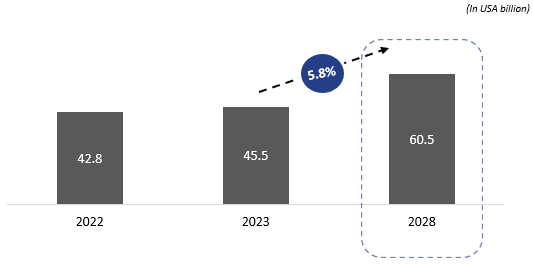

• The global commercial refrigeration market, valued at USD 45.5 billion in 2023, is expected to grow at a CAGR of 5.8%, reaching USD 60.5 billion by 2028.

• This steady growth is driven by rapid urbanization with its current size of 4.4 billion inhabitants to double by 2050, at which point nearly 7 of 10 people will live in cities. {12} Evolving consumer preferences for convenience foods, fresh produce, and ready-to-eat meals. These trends are increasing the demand for efficient refrigeration solutions to store and transport perishable products, ensuring sustained market expansion in the coming years.

Exhibit 3: Seizing Opportunities in the global commercial refrigeration market, projected to grow at 5.8% CAGR by 2028. {12}

Commercial Refrigeration Market Dynamics {12}

• Driver: High demand for frozen & processed food worldwide:

Frozen food products are increasingly becoming an integral part of daily diets worldwide. Rapid urbanization in developing countries and rising living standards fuel the demand for processed and packaged food, leading to higher commercial refrigeration system sales.

• Restraint: Stringent regulations against use of fluorocarbon refrigerants:

Global regulations targeting fluorocarbon refrigerants, such as HCFCs and HFCs, aim to mitigate their environmental impact, including ozone depletion and climate change. These restrictions on production, usage, and emissions are expected to pose challenges to the growth of the commercial refrigeration market.

• Opportunity: Potential demand for carbon dioxide/ ammonia cascade refrigeration systems

H3/CO2 cascade refrigeration systems offer lower operating and capital costs, reduced energy consumption, compliance benefits, improved food quality, and enhanced throughput for food and beverage processing. These benefits are expected to drive opportunities in the commercial refrigeration market during the forecast period.

• Challenge: Limited purification companies

The commercial refrigeration market faces a challenge due to the limited number of companies producing refrigerant-grade ammonia and CO2. These purification companies play a critical role in ensuring high-quality refrigerants that meet industry standards. Their scarcity impacts the availability and growth potential of refrigeration systems reliant on these refrigerants.

MEP (Mechanical, Electrical, Plumbing and Fire-fighting) Contracting {13}

• The mechanical, electrical, and plumbing (MEP) services market in India is expected to grow by USD 5.27 billion at a CAGR of 25.79% from 2023 to 2028.

• These include HVAC systems for temperature control, lighting systems for illumination, gas pipelines for energy distribution, plumbing systems for water supply and drainage, and more.

• MEP services are integral to construction activities, with applications in commercial complexes, residential complexes, transportation hubs, healthcare facilities, educational institutions

• Key factors driving this growth include the 15.9% increasing use of renewable energy in buildings {14} , which requires specialized MEP services for sustainable energy systems, and the adoption of Building Information Modeling (BIM) for more efficient design and construction. However, the market also faces challenges, such as limited service differentiation, leading to high competition and pricing pressures.

• The future of MEP services will be shaped by key trends including the integration of smart building technologies, enhancing energy efficiency, and prioritizing occupant health and wellness. Sustainability will drive innovations in HVAC, lighting, and water systems, while modular construction and prefabrication will improve timelines and quality. {15}

• The shift towards electrification will require expertise in EV charging and electric heating. MEP services will also focus on resilience, disaster preparedness, and meeting evolving regulatory requirements. As urbanization grows, especially in emerging markets, MEP firms will find expansion opportunities. Staying updated with changing regulations will be crucial for staying competitive.