NSE: BANKBARODA

BoB operates a diversified business model, combining retail and corporate banking with treasury, international banking, and digital services, aimed at delivering comprehensive financial solutions across domestic and global markets.

1. Retail Banking

Retail Banking segment at BoB focuses on providing a wide range of financial products to individual customers, including personal loans, home loans, auto loans, education loans, savings and deposit accounts, and credit cards. The segment aims to increase customer outreach through digital channels and a vast branch network, catering to both urban and rural customers across India.

As of FY24, the retail advances portfolio accounted for about 23% of the bank’s total domestic advances, with retail loans totaling around ₹2.3 lakh crore. The segment achieved growth in home loans and personal loans, contributing significantly to the bank’s overall revenue, with retail interest income amounting to over ₹25,000 crore.

BoB has a large retail customer base of over 150 million, attributed by digital presence and product offerings on platforms like the BoB World app. Digital transactions through BoB World grew by around 60% year-over-year, reflecting the bank’s push towards digital banking and customer engagement.

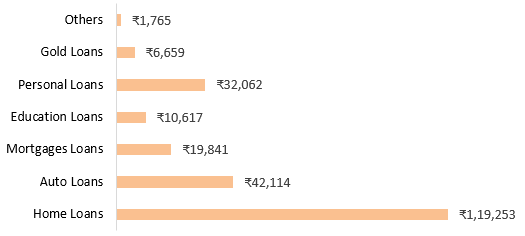

Exhibit 1: Home Loans composed more than 50% of retail advances for 2 years(₹ Cr.)

2. Corporate/Wholesale Banking

Corporate Banking segment of BoB provides financial solutions to large and mid-sized corporate clients, including lending, trade finance, cash management, and structured finance services. This segment focuses on key industries such as infrastructure, energy, real estate, and manufacturing, offering products like working capital loans, term loans, project financing, and treasury solutions tailored to corporate needs.

In FY24, the corporate advances segment constituted approximately 42% of BoB’s total loan portfolio, with corporate advances totaling around ₹3.4 lakh crore. The segment has maintained a steady growth rate, contributing over ₹25,500 crore in income.

BoB’s corporate banking segment has been actively managing asset quality, achieving a gross non-performing asset (NPA) ratio for corporate loans around 3.5%, showing improvement over previous years. The bank employs stringent credit appraisal, monitoring systems, and sector-specific risk assessments to maintain portfolio health and mitigate risks in its corporate lending activities.

Recently Bank has entered into an MOU with IREDA for collaboration (BoB Earth) in areas of Co-Lending for Renewable Energy Projects as well as Loan Syndication and Underwriting. Bank has an outstanding of ₹ 15,268 crore for financing renewable energy projects under Corporate Credit segment.

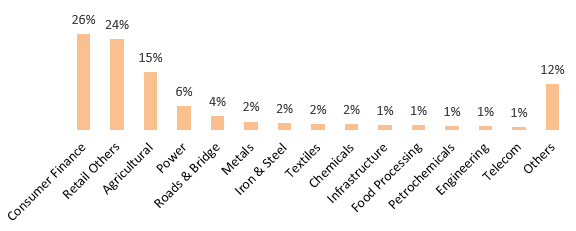

Exhibit 2: Power with maximum allocation of corporate advances: 6.27% share

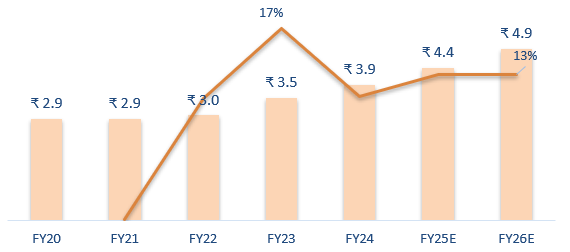

Exhibit 3: Corporate advances expected to reach ₹4.9 lakh crore by FY26, with 13% YoY growth

3. Treasury Banking

Treasury Banking segment at BoB manages the bank’s liquidity, investment portfolios, and trading activities across domestic and international markets. The core functions include investments in government and corporate securities, foreign exchange trading, derivatives, and money market operations. The bank’s treasury department also handles asset-liability management (ALM), ensuring risk mitigation through effective hedging and regulatory compliance.

In FY24, BoB treasury operations contributed significantly to its income, accounting for around 22% of the bank’s total revenue. The segment achieved a net trading income of approximately ₹1,500 crore ($180 million), driven largely by favorable bond yield movements and effective forex transactions.

As of the latest fiscal year, BoB’s investment portfolio stood at over ₹3 lakh crore (₹3 trillion or approximately $36 billion), with a majority allocated to government securities, followed by corporate bonds and other investments. The treasury segment actively manages interest rate, currency, and liquidity risks to enhance profitability while adhering to the bank’s conservative risk framework.

4. Agriculture Banking

The Agriculture Banking segment of BoB is dedicated to providing financial services to farmers, agri-businesses, and rural communities. Core offerings include crop loans, equipment financing, dairy loans, horticulture loans, and financing for allied agricultural activities. The bank also participates in government programs like the Pradhan Mantri Kisan Credit Card (KCC) scheme and aims to support rural economic growth by enhancing credit access for agricultural needs.

As of FY24, the agriculture banking portfolio represented around 15% of BoB’s total advances, with agricultural loans totaling approximately ₹1.38 lakh crore. The segment’s interest income from agriculture advances exceeded ₹2,000 crore, sshowing consistent growth driven by increased lending to small and marginal farmers. As of the latest fiscal year, the bank supported over 2 million Kisan Credit Card holders, with continued investments in digital solutions to streamline credit applications and improve access to finance for rural customers.

5. MSME

The bank aims to empower MSMEs by offering financing solutions across sectors, promoting entrepreneurship, and participating in government schemes like the Emergency Credit Line Guarantee Scheme (ECLGS) and Pradhan Mantri Mudra Yojana.

As of FY24, MSME advances constituted around 20% of BoB’s total loan portfolio, with lending to MSMEs reaching approximately ₹2 lakh crore. The segment has shown strong growth, with MSME interest income contributing over ₹3,500 crore annually, driven by targeted outreach programs and a streamlined loan application process.

BoB has leveraged digital platforms, such as the Baroda Digital Loan for MSME program, to enable quicker loan approvals and disbursements, significantly improving accessibility for MSME clients. In FY23, digital loan processing for MSMEs grew by over 40%.

6. International Banking Segment

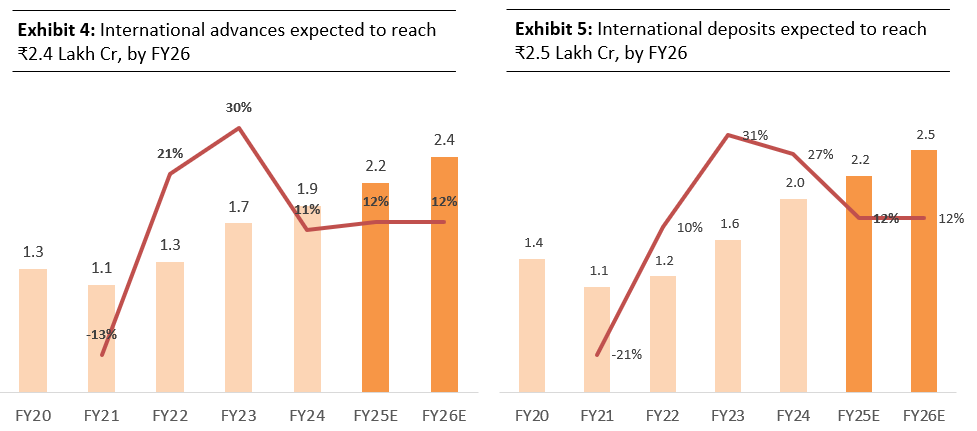

BoB operates across 17 countries with a network of international branches and subsidiaries, allowing it to serve Indian expatriates, support cross-border trade, and tap into global banking markets. Bank’s international banking segment specializes in Non-Resident Indian (NRI) services, remittances, and trade finance, providing a competitive edge in meeting the financial needs of the Indian diaspora and businesses involved in international trade.

BoB international banking segment is exhibiting promising signs of growth and improved performance. International deposits have shown a year-on-year growth of 27%, increasing from ₹ 1,56,313 crore in 2023 to ₹ 1,98,444 crore as of 31st March 2024. While the growth in international advances was more moderate at 10.6%, reaching ₹ 1,92,390 crore as of 31st March 2024. The yield on international investments has seen a significant uptick. This yield has climbed from close to 3.5% in March 2023 to 4.1% in March 2024, indicating improved profitability in the bank’s international investment portfolio.

Certain key ratios pertaining to International segment,

| Particulars ( in % ) | Q4FY24 | FY23 | FY24 |

| Cost of Deposits | 1.95% | 1.94% | 1.97% |

| Yield on Advances | 5.84% | 6.50% | 6.34% |

| Net interest Margins | 3.27% | 3.31% | 3.18% |

Source: Investor Presentation Q2FY25

Subsidiaries and JVs Performance

1. BOBCARD Limited

It has shown impressive growth across key metrics. The company’s card base expanded significantly, with the number of cards in circulation increasing by 29.68% year-on-year to reach 28.09 lakhs as of September 30, 2024. This growth in cardholders translated to a 39.85% surge in spending, which rose from ₹ 12,256 crore in H1 FY24 to ₹ 17,141 crore in H1 FY25. Furthermore, both Average Net Revenue (ANR) and Effective Net Revenue (ENR) witnessed substantial increases of 40.04% and 34.08% respectively, indicating revenue generation and overall strong financial performance for BOBCARD.

2. BOB Capital Markets Limited

It has delivered a strong performance in the first half of FY25, driven by significant growth across various business segments. Gross revenue surged by 49% year-on-year, reaching ₹ 26.29 crore.

The Investment Banking Equity division played a key role in this success, achieving a 553% revenue growth, fueled by successful completion of IPOs for

● P N Gadgil Jewellers Ltd.

● Ola Electric Mobility Ltd.,

● Bharti Hexacom Ltd. (Deal Value of ₹ 1,100Cr., 6,145Cr., 4,273 Cr. respectively)

Retail broking revenue also saw a healthy 62% increase, accompanied by a significant expansion of the retail client base.

3. Baroda Global Shared Services Limited

It experienced a slight dip in performance during the first half of FY25. Total income decreased marginally by 0.51% year-on-year, reaching ₹ 165.11 crore, with a similar decline of 0.77% in revenue from operations. Profit after tax also fell by 23.93% to ₹ 7.66 crore. Despite these declines, the company successfully completed the ISO 27001:2013 Certification surveillance audit.

4. Baroda BNP Paribas Asset Management India Pvt. Ltd.

It has delivered strong results in the first half of FY25. The company achieved a remarkable 44% year-on-year growth in Average Assets Under Management (AAUM), reaching ₹ 45,165 crore as of September 30, 2024. This growth is mirrored by a 44% increase in gross revenue, which reached ₹ 84.27 crore. Notably, the company transitioned from a net loss of ₹ 4.12 crore in H1 FY24 to a net profit of ₹ 16.73 crore in H1 FY25. Furthermore, Baroda BNP Paribas successfully launched three New Fund Offers (NFOs) in H1 FY25, mobilizing ₹ 2,639.27 crore, significantly exceeding the ₹ 1,457.63 crore mobilized through a single NFO in H1 FY24.

Baroda BNP Paribas Mutual Fund offers a diverse range of funds with varying historical performance. Here’s a glimpse into some of their key offerings:

Strong Performers:

● Baroda BNP Paribas Multi Cap Fund: This fund has demonstrated impressive returns, with annualized returns of approximately 17.7% over the past 3 years and 23.66% over the past 5 years.

● Baroda BNP Paribas Large & Mid Cap Fund: This fund has delivered strong returns, with 43.75% in the last year, 18.46% in the last 3 years, and 28.86% since its inception.

Moderate Performers:

● Baroda BNP Paribas Balanced Advantage Fund: This hybrid fund has provided more moderate returns, with annualized returns of approximately 13.48% over the past 3 years and 17.26% over the past 5 years.

● Baroda BNP Paribas Large Cap Fund: This fund has yielded relatively moderate returns, with 16.58% in the last year.

5. IndiaFirst Life Insurance:

IndiaFirst Life Insurance Co. Ltd. has recorded a 21.3% year-on-year increase in Assets Under Management (AUM), reaching ₹ 29,962 crore as of September 30, 2024. However, the company experienced a decline in both New Business Gross Written Premium (GWP) and overall GWP in the first half of FY25 compared to the same period in FY24. New Business GWP stood at ₹ 1,366 crore, and overall GWP was ₹ 3,162 crore. Despite these challenges, IndiaFirst Life maintained its position as the 12th-ranked insurer in India for both New Business GWP and individual new business Annualised Premium Equivalent (APE) in H1 FY25, indicating a continued presence in the market.

6. India Infradebt:

Focuses on lending to infrastructure and renewable energy projects. India Infradebt Limited has demonstrated strong financial performance in the first half of FY25. Total income grew by 12.39% year-on-year, reaching ₹ 363.67 crore, while operating profit increased by 12.22% to ₹ 334.24 crore. The company’s net profit surged by 28.04%, reaching ₹ 327.88 crore. Management guidance stated that subsidiary is in talk with launching IPO in FY26.

Exhibit 6: Wholly owned Subsidiary Portfolio