NSE: BANKBARODA

The Collapse of Silicon Valley Bank

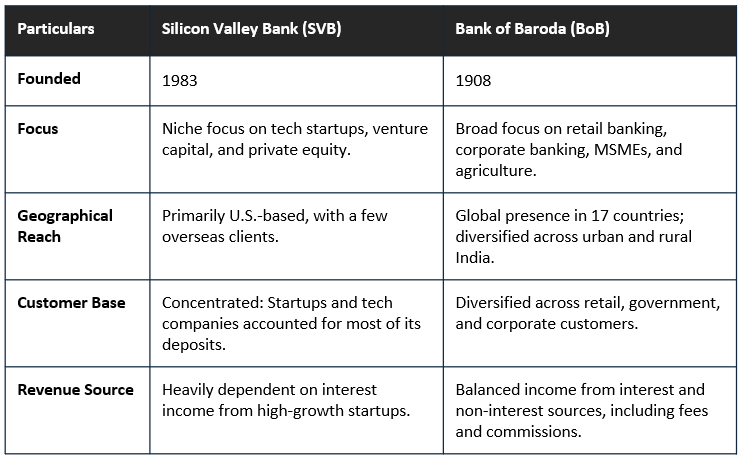

● Brief overview of Silicon Valley Bank (SVB): Established in 1983, SVB primarily catered to startups, venture capital firms, and tech companies. At its peak, SVB had over $200 billion in assets, ranking as the 16th largest bank in the U.S.

● Significance of the collapse: On March 10, 2023, SVB became the second-largest bank failure in U.S. history after Washington Mutual (2008). Triggered widespread concerns about banking stability, particularly for institutions exposed to interest rate risks.

Causes of the SVB Collapse

1. Excessive Investment in Long-Duration Assets

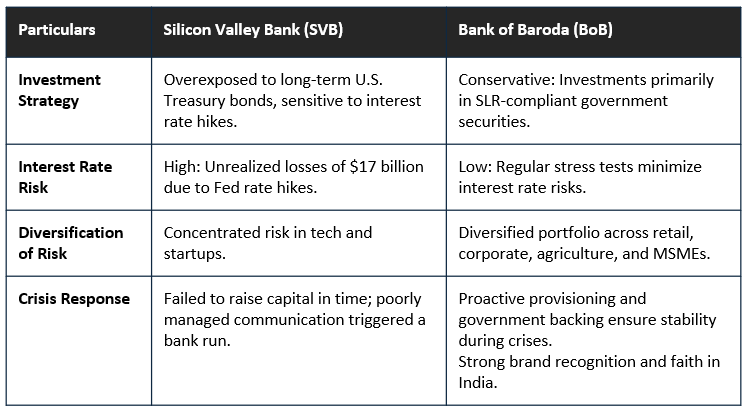

SVB invested over $91 billion in long-term U.S. Treasury bonds and mortgage-backed securities during the low-interest-rate period.

When the Federal Reserve raised interest rates in 2022-2023, these assets’ market value dropped significantly, leading to unrealized losses of $17 billion.

2. Liquidity Mismatch

SVB faced increased withdrawals as tech startups and venture-backed companies drew down deposits amid declining funding availability.

More than 93% of SVB’s deposits were uninsured (above the $250,000 FDIC limit), leading to higher depositor panic.

3. Panic and Bank Run

On March 8, 2023, SVB disclosed a $1.8 billion realized loss from selling securities to raise liquidity. This announcement caused depositors to withdraw $42 billion in a single day, creating a liquidity crisis.

4. Regulatory Loopholes

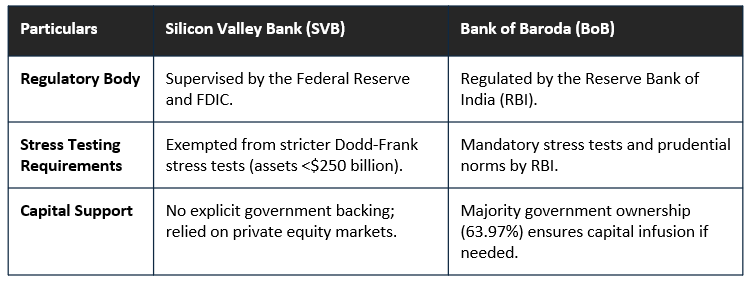

Due to the 2018 rollback of Dodd-Frank regulations, SVB, with less than $250 billion in assets, was not subject to stricter stress tests.

These regulatory gaps allowed vulnerabilities to go undetected.

Impact of the Collapse

1. Immediate Consequences

Bank seizure: The FDIC took control of SVB, and all depositors were guaranteed access to their funds, even those above FDIC limits.

2. Tech Ecosystem Disruption

Over 50% of U.S. venture-backed startups were customers of SVB. Many companies faced temporary operational disruptions due to frozen deposits.

3. Market Reactions

Banking stocks dropped globally, with significant declines in regional banks like First Republic Bank, which later failed as well.

Lessons and Recommendations

1. Risk Management: Banks must diversify assets to avoid overexposure to interest rate-sensitive securities. Stricter monitoring of liquidity risks is essential, especially for banks like SVB with concentrated depositor bases.

2.Regulatory Oversight: Reevaluate and extend stress-testing requirements to mid-sized banks. Revisit the 2018 Dodd-Frank rollback to ensure early identification of vulnerabilities.

3.Crisis Communication: Transparent and well-timed disclosures can prevent panic. SVB’s timing of announcing losses exacerbated the bank run.

Conclusion

The collapse of Silicon Valley Bank highlighted the critical interplay between interest rate risks, depositor confidence, and regulatory oversight. As financial institutions navigate a volatile macroeconomic environment, risk management and adequate oversight will be pivotal in ensuring stability.

Key Statistics and Facts

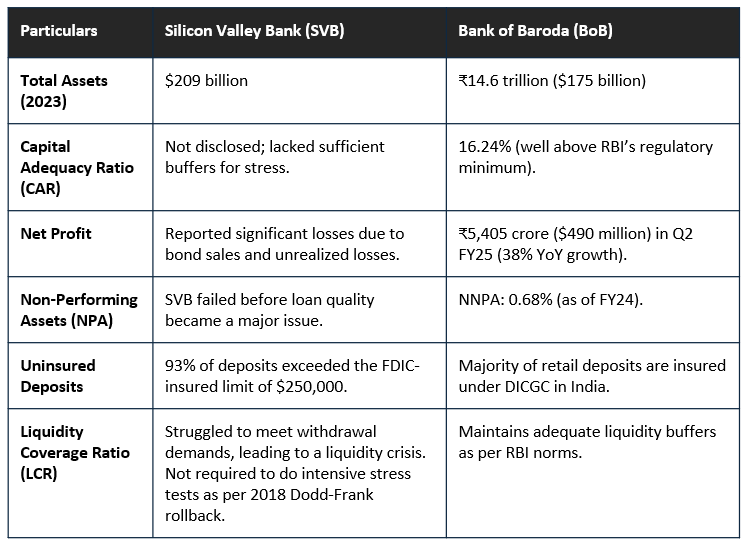

● SVB’s assets: $209 billion (2023).

● Unrealized bond losses: $17 billion.

● Withdrawals during the bank run: $42 billion in 24 hours.

● Uninsured deposits: 93% of total deposits.

● Federal Reserve rate hikes: Increased from 0.25% to 4.75%–5.00% (March 2022–March 2023).

Silicon Valley Bank (SVB) vs. BoB (BoB)

Introduction

The collapse of Silicon Valley Bank (SVB) in March 2023 exposed the vulnerabilities of poorly diversified banking models and weak risk management practices. In contrast, BoB (BoB), a public sector bank in India, showcases resilience due to its diversified portfolio, regulatory framework, and government support. This study compares SVB and BoB across key parameters to highlight why BoB remains a stable institution.

1. Business Model and Focus

2. Financial Metrics and Stability

3. Risk Management and Investment Strategy

4. Regulatory Oversight

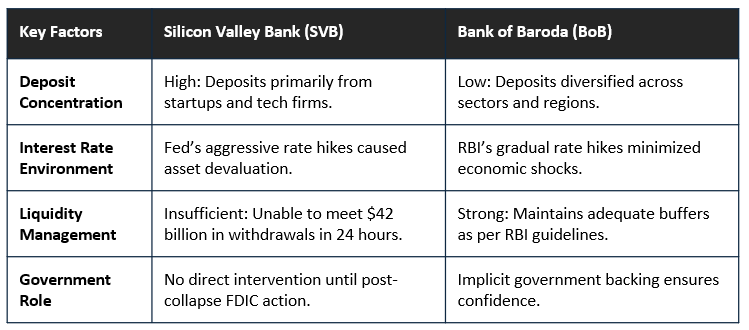

5. Causes of SVB’s Collapse vs. BoB’s Resilience

6. Lessons and Takeaways

Silicon Valley Bank

● A narrow business model reliant on startups and tech clients made SVB highly vulnerable to sector-specific downturns.

● Poor communication and risk management compounded the crisis, leading to a loss of depositor confidence.

BoB

● A diversified business model, government ownership, and strict regulatory compliance ensure resilience against global shocks.

● Proactive asset management and a focus on risk diversification have positioned BoB as a stable financial institution.

Conclusion

The Silicon Valley Bank collapse highlights the perils of a concentrated business model and inadequate risk management in a volatile economic environment. In contrast, BoB’s diversified portfolio, strong regulatory oversight, and public sector backing provide a foundation for its stability. While SVB serves as a cautionary tale, BoB exemplifies the importance of prudent banking practices and regulatory safeguards in ensuring long-term resilience.