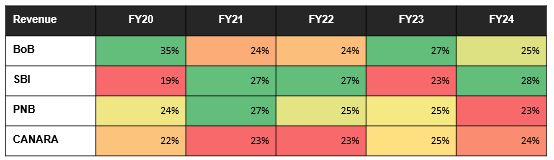

Revenue (in cr)

● SBI demonstrates the most consistent and growth, overtaking BoB in FY23 and maintaining leadership in FY24.

● BoB shows resilience, recovering partially after FY21 but loses its dominant share from FY20. This is a result of BoB’s strategic shift towards retail lending. While the bank’s corporate loan segment grew by 13.2% in FY23, its organic retail advances grew at a much faster rate of 26.8%. This focus on retail lending, which is considered less risky than corporate lending, could have contributed to the bank’s improved asset quality and hence revenue.

● PNB maintains stability but lacks significant growth momentum, while Canara Bank lags throughout the observed period with minimal gains.

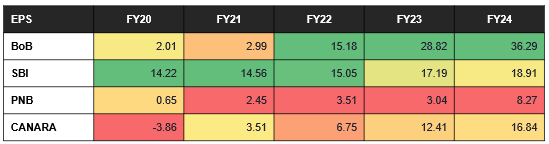

Earnings Per Share (in Rs.)

● The bank’s net interest income grew by 13.2% in FY2022, driven by a decline in interest expenses. Operating profit also saw a 5.6% increase, while profit after tax (PAT) saw a remarkable growth of almost 9 times, reaching `7272 crore. This growth in profitability directly contributes to the improvement in EPS.

● PNB remains the weakest performer, with an EPS far below its peers, despite a steady upward trajectory.

● Canara Bank shows a remarkable turnaround, moving from losses to a competitive EPS, signaling a successful recovery.

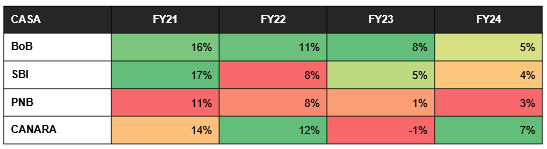

CASA Deposits YoY% Growth

● Consistent Decline Across Banks: All banks, except Canara Bank, show a steady decline in CASA growth over the period, reflecting rising competition for low-cost deposits and possible changes in depositor behavior.

● Driven by strategic initiatives like digital onboarding and targeted product launch BoB NOW, for opening current accounts for existing bank customers.

● Despite a dip in FY23, Canara Bank ends on a high note, surpassing its peers in FY24 with 7% growth, which is also on track with managements guidance of 7.5% for FY25.

● SBI’s Leadership Narrowed: SBI’s early lead diminishes by FY24 as its CASA growth matches the declining trend of peers.

● PNB’s Weakness: PNB consistently trails the group, suggesting challenges in improving its CASA mix and deposit base competitiveness.

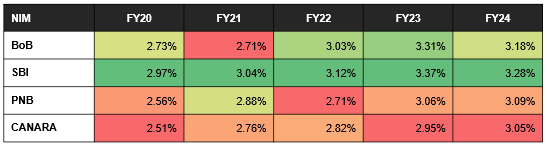

Net Interest Margin

● SBI consistently maintained the highest NIM among the four banks throughout the period, demonstrating its strong ability to generate profits from its lending operations. It showed steady improvement, peaking in FY23 before a slight dip in FY24.

● BoB started with a relatively lower NIM but showed significant improvement, particularly in FY22 and FY23. However, like SBI, it also experienced a slight decline in FY24. BoB’s improvement was attributed to strong earnings growth, declining provisions, and a focus on efficiency and digitalization and also precisely on track with management’s guidance of 3.15%

● PNB had a mixed performance. While it showed improvement in some years, its NIM remained volatile and generally lower than SBI and BoB.

● CANARA consistently had the lowest NIM among the group, though it did show gradual improvement over the years. It had the most significant jump in NIM in FY24 compared to the previous year.

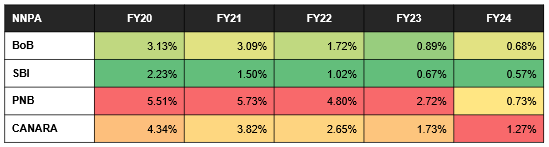

Net Non-Performing Assets

● SBI consistently maintained the lowest NNPA throughout the period.

● BoB started with a relatively higher NNPA but showed substantial improvement, particularly in FY22 and FY23. BoB has implemented a stressed asset management framework with a dedicated vertical and a network of specialized branches. SAM branches handle NCLT cases, while SARB branches manage other NPAs. Additionally, BoB focuses on prudent underwriting, lending to high-quality borrowers and employing risk-based pricing models to minimize defaults. It adopts a conservative provisioning approach, making 100% provisions for specific NPAs, including unsecured loans over six months old, secured loans with extended NPA status, and overdue agricultural loans like tractor financing.

● PNB had the highest NNPA in FY20 and FY21 but made significant progress, reducing it in FY24. Canara Bank, with higher NNPA than SBI and BoB, showed steady improvement but still needs to catch up to their levels.

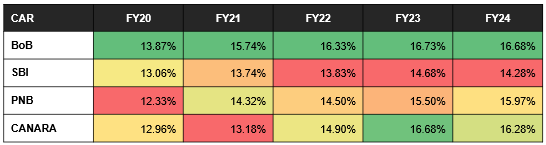

Capital Adequacy Ratio

● BoB consistently maintained the highest CAR among the four, BoB manages its capital proactively, using instruments like AT-1 bonds and replacing maturing bonds in FY24 for strategic capital planning. The bank has also successfully executed Qualified Institutional Placements (QIPs), raising ₹4,500 crore in FY21, attracting top investors and strengthening its capital adequacy. It has also successful achieved management’s guidance of CET ratio of 13%.

● PNB had the lowest CAR initially but showed gradual improvement, indicating steps taken to strengthen its capital position. Canara Bank’s CAR fluctuated, with increases in some years followed by stagnation or minor declines, suggesting a need for more consistent efforts to enhance capital adequacy.