NSE: EPACK

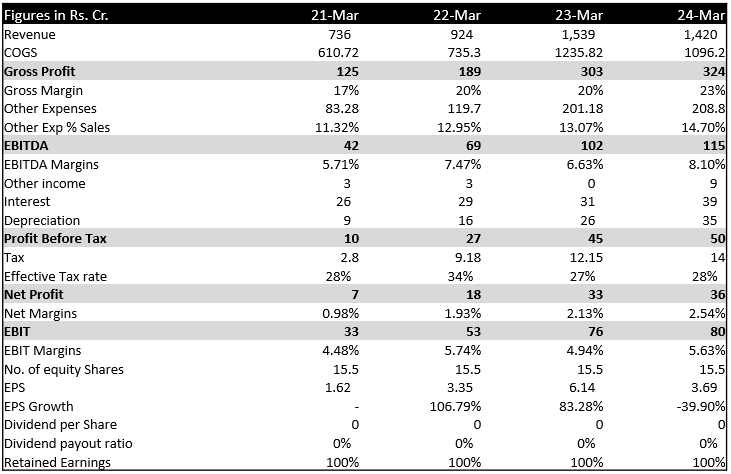

Profit & loss statement

• The company’s revenue declined by 9% in FY2023-24, mainly due to weather disruptions and inventory liquidation. However, Q1 FY25 saw a 77% YoY increase in revenue, indicating stronger demand during peak seasons. Future growth is expected from partnerships with Hisense for air conditioner manufacturing and Panasonic Life Solutions for component production, targeting $1 billion in revenue over five years with management projects a 40-50% revenue growth for FY ‘25. {72}

• The company’s COGS decreased by 11.2% in FY23-24, driven by a 6% reduction in raw material costs, including plastic, copper, aluminum, and stainless steel. This decline was mainly influenced by a significant drop in steel prices in India. As of August 2024, cold rolled steel (CRT) prices fell from ₹71,000 per tonne in December 2021 to ₹57,400, and hot rolled coil (HRC) steel prices dropped by 24%, from ₹66,000 to ₹50,300 per ton. This shows that dropping steel prices will give us low COGS and further increase Revenue. {73}

• The EBITDA margin grew steadily by 8.1%, as the reduction in COGS outweighed the decline in revenue, increasing operating profit. This is a potential recovery in revenue, combined with reducing steel prices and giving lesser COGS, positions the company to strengthen its profitability further in the coming financial year as the emphasis of the company is on raising capacity utilization.

• Interest expenses rose by 9% in FY23-24, primarily due to a 23% increase in finance costs. This was driven by a rise in the term loan for new manufacturing units in Andhra Pradesh, which increased from ₹8.4 crore in 2023 to ₹10.35 crore in 2024.

• Depreciation expense grew by 34% in FY23-24, primarily due to a 55% increase in plant and machinery following the establishment of a new manufacturing unit (Andhra Pradesh Sri city) in 2024. Additionally, land worth ₹50 crore was purchased during the year, contributing to the rise in depreciation.

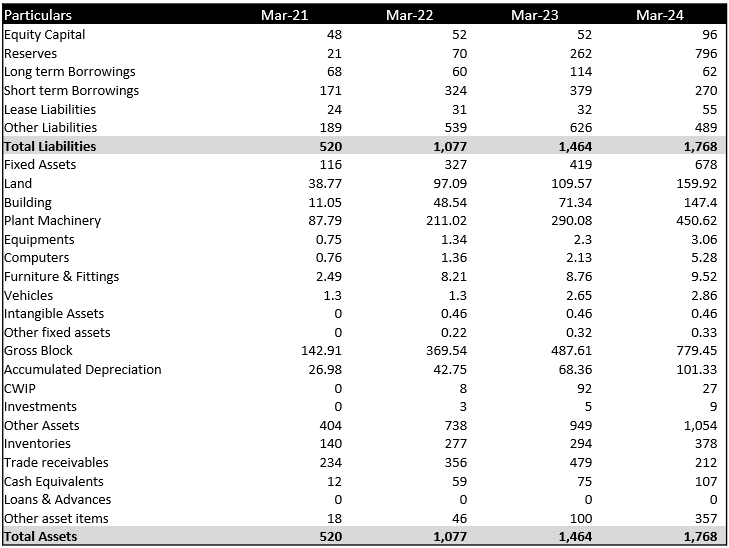

Balance sheet

• The company’s share capital increased in FY24 due to its listing on January 30, 2024, raising ₹26 crore from converting preference shares to equity and ₹17 crore from the IPO. The funds will support capital expenditure, debt repayment, and general purposes.

• The reserves increased by 203% from FY23 to FY24, primarily due to the fresh issue of shares and the securities being listed at a premium, resulting in a 300% rise in the securities premium. Additionally, retained earnings increased by 148% during the year FY23-24.

• Borrowings decreased by nearly 50% in FY23-24, which included a 73% reduction in the working capital demand loan and a 35% decline in term loans (non-current) from banks during FY24. This enhances the company’s financial stability and provides flexibility for future growth investments.

• In 2024, the company established a new manufacturing unit in Sri City, Chittoor, Andhra Pradesh. This led to a 55% increase in plant and machinery, a 45% rise in land, and a 107% growth in building assets during FY23-24, resulting in higher depreciation expenses in FY24.

• The Capital Work in Progress (CWIP) decreased by ₹62cr. from FY23 to FY24, as the amount was capitalized, leading to a corresponding increase in the net block by 61.8% in FY24. This increase was attributed to factory buildings, plant and machinery, electrical installations, office equipment, computers, and vehicles in Gross Block which is associated with the new manufacturing unit that commenced operations in FY24.

• Trade receivables decreased by 55% in 2024, primarily due to a significant 55% reduction in unsecured receivables during FY23-24. This improvement is reflected in the average receivable days, which reduced sharply from 115 days in 2023 to 55 days in 2024, highlighting better collection efficiency of the company.

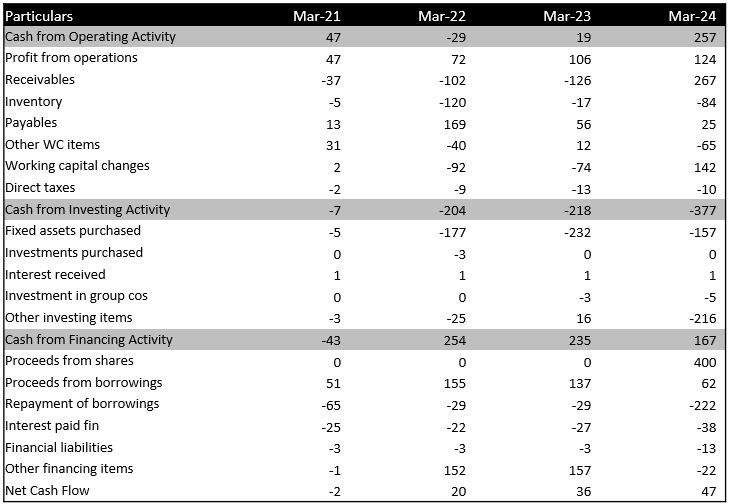

Cash Flow Statement