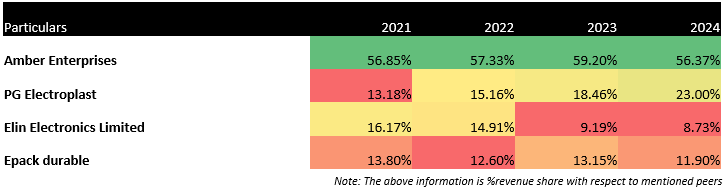

Revenue

• Amber enterprise remains the leader in absolute revenue with a steady revenue share of around 56-59% over the years, while PG electroplast showcases the strongest growth rate from 13.18% in 2021 to 23.00% in 2024.

• Compared to peers, Epack’s revenue share of 13.15% was recorded in 2023 followed by a fall of 8% in 2024 due to slower sales during off-peak seasons. Despite this drop, the company has shown potential for recovery with a surge of 112% in Q2FY25 revenue followed by initiatives like expanding its client base and focusing on product innovation to address market fluctuations and seasonal dependencies. Company aims to achieve 45-50% growth in revenue for FY25. {73}

• Elin Electronics’ revenue share has consistently declined, dropping from 16.17% in 2021 to 8.73% in 2024 which is more than Epack.

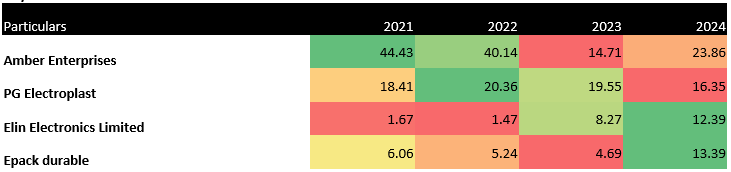

EV/EBITDA

• Amber Enterprises showed the most volatility, with EV/EBITDA declining sharply from 44.43 in 2021 to 14.71 in 2023 before partially recovering to 23.86 in 2024. PG electroplast maintained relatively stable EV/EBITDA values, peaking at 20.36 in 2022 and moderating to 16.35 in 2024.

• Compared to its peers, in FY24, Elin Electronics and Epack Durables achieved the highest EV/EBITDA of 12.39 & 13.39 compared to their past performance. This reflects their strong overall valuation and increasing operating performance by 49.8% and 185% in FY24 respectively, positioning them favorably in peer comparisons.

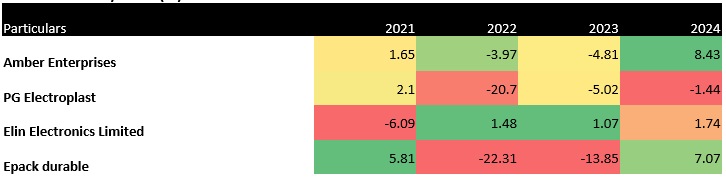

Free Cash Flow/Sales (%)

• Amber enterprise transitioned from negative FCF/Sales in 2022 and 2023 (-3.97%, -4.81%) to a healthy 8.43% in 2024, the highest among peers.

• Elin maintained positive FCF/Sales throughout the period, with modest growth from 1.48% in 2022 to 1.74% in 2024, indicating consistent but limited cash generation.

• Whereas, EPACK rebounded significantly in 2024, achieving a positive FCF/Sales ratio of 7.07%, after facing steep declines in 2022 (-22.31%) and 2023 (-13.85%), indicating its improved ability to convert sales into cash.

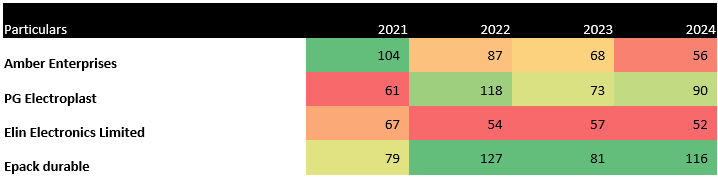

Inventory days

• Amber demonstrated a consistent improvement in inventory management, reducing inventory days from 104 in 2021 to 56 in 2024, showcasing operational efficiency.

• PG electroplast faced volatility in inventory days to be 90 in 2024, while Elin electronics led with the lowest at 52 days in 2024, reflecting better efficiency.

• EPACK’s inventory days increased from 81 in 2023 to 116 in 2024, reflecting potential overstocking and slower inventory turnover. This trend is concerning for the company as it indicates an inability to sell products at the same pace as they are being manufactured, leading to stock accumulation.