NSE: FEDERALBNK

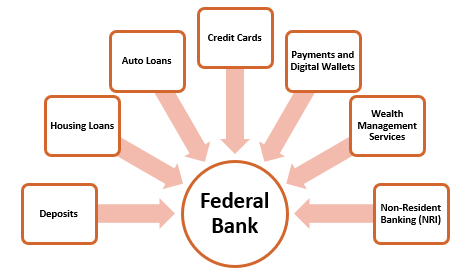

Retail Banking Division

FBL’s retail banking segment caters to the varied needs of individual clients and businesses with a wide range of tailored products and services. FBL retail banking strategy in FY 2024 showed strong growth across key areas. The retail credit book reached ₹119,493 crore, while retail deposits grew 18.35% year-on-year, boosting Net Interest Margin (NIM) through higher-yielding loan products.

High-margin lending in personal loans, credit cards, and microfinance saw significant growth, with personal loans and credit cards increasing by 78% and microfinance by 141%. Credit card adoption expanded to 2.5 lakh users, with spending doubling to ₹360 crore. 1

Products offered : 1

• Retail Banking: Deposits, mortgage-backed housing loans, retail loans against property (Retail LAP), auto loans, cards and payments, non-resident banking, and wealth management services.

• Business Banking: Business loans to Micro, Small and Medium Enterprises (MSMEs).

• CV/CE Financing: Purchase of new and used commercial vehicles and construction equipment for single-unit owners, fleet operators, and strategic clients.

• Agri Banking: Financing solutions for agriculture and the priority sector.

• Gold Loans: FBL uses innovative products to offer loans against gold.

• Microfinance: Financing solutions for improving financial inclusion in rural area and promoting inclusive growth.

During FY24, the bank offered tailored solutions in the MSME segment, with average ticket sizes ranging from ₹70 lakh for small businesses to ₹15-17 crore for medium-sized enterprises. However, Gold loans saw a decline in average ticket size, dropping below ₹30,000.

Exhibit 1: Retail banking services and products offered by Federal bank

Source: Annual report

Wholesale Banking Division

The wholesale banking segment offers a diverse range of financial solutions, including working capital and term loans, trade finance, cash management, supply chain finance, forex services, treasury products, gold metal loans, structured offerings, liability products, and digital banking solutions.

FBL’s wholesale banking segment comprises three key divisions:

• Commercial Banking (CoB): This division is dedicated to mid-market enterprises and Micro, Small, and Medium Enterprises (MSMEs), providing a broad range of customized financial solutions.

• Corporate and Institutional Banking (CIB): tailored for large corporates, multinational corporations (MNCs), public sector undertakings (PSUs), capital market clients, and financial institutions. This division focuses on delivering high-value, complex financial solutions.

• Government & Institutional Business (GIB): focuses on serving government departments, public institutions, and related entities. Its primary goal is to strengthen Federal Bank’s liability business while supporting public sector projects and services.

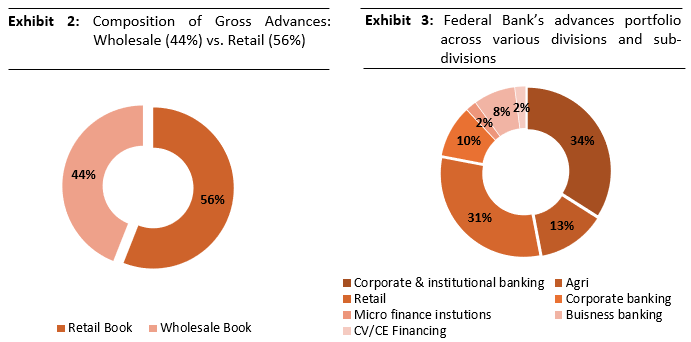

FBL wholesale credit business grew by 15% in FY 2024, reaching ₹95,083 crore. This included two main categories: corporate banking loans, which increased by 12% to ₹73,596 crore, and commercial banking loans, which grew by 27% to ₹21,487 crore.

The average loan size recorded in the wholesale banking segment was ₹23 crore. Supply Chain Finance (SCF) played a significant role in the growth of the wholesale portfolio. Over the recent years, The SCF book expanded from ₹1,420 crore to ₹7,134 crore in FY24, reflecting compounded annual growth rate (CAGR) of 71.3%. This indicates a focus on expanding financial offerings in this area. further the wholesale banking division played an important role in driving FBL’s overall fee income, which grew by 28% in FY 2024 to ₹512 crore. 1

Source: Annual report

Treasury and other banking operations:

The treasury division actively managed liquidity, investments, and risks, while also supporting the bank’s strategic focus on flow-based businesses. It plays a crucial role in managing the FBL’s liquidity, statutory reserves, and investment portfolio. It also provides a range of services to clients, including foreign exchange, derivatives trading, and risk management solutions

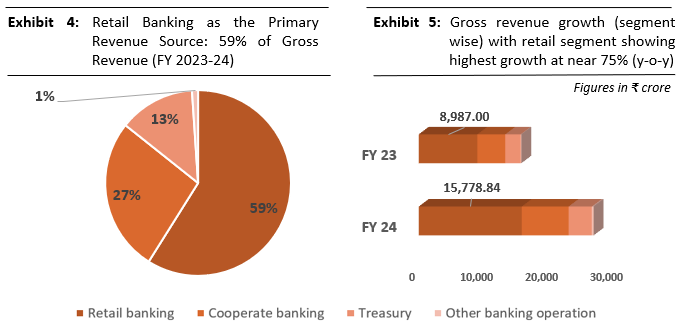

In FY 2024, the treasury segment generated ₹3,546.55 crore in revenue, accounting for a notable share of the bank’s total revenue of ₹26,776.31 crore. In terms of profitability, the treasury division reported a profit of ₹602.18 crore, contributing significantly to the bank’s overall net profit of ₹3,880.43 crore. 1

Other banking operations: Apart from the regular banking operations FBL also offers a wide range of insurance products, including life, health, and property insurance through multiple distribution channels, including branches, digital platforms, and telesales.

In FY 2023-24, insurance distribution emerged as the largest contributor to FBL’s non-banking fee income, generating ₹168 crore out of the total ₹181 crore from insurance and para-banking products. Additionally , fee income recorded from wealth management services was ₹21 crore.

FBL is active in the Non-Resident Indian (NRI) banking segment, offering remittance services for international fund transfers. The bank has a network of over 110 global remittance arrangements, serving a wide customer base These remittance services are supported by a network of more than 90 partners worldwide, providing broad coverage and accessibility to its customers.

In FY 2024, the bank facilitated inward remittances of over ₹1,80,000 crore through RDA. Additionally, the bank’s market share in personal inward remittances to India increased from 17% in FY 2022 to 19.30% in FY 2023, and further to 20% in FY 2024. 1

Source: Annual report

Subsidiary and associate companies: 1 2

• Fedbank Financial Services Limited (FedFina)

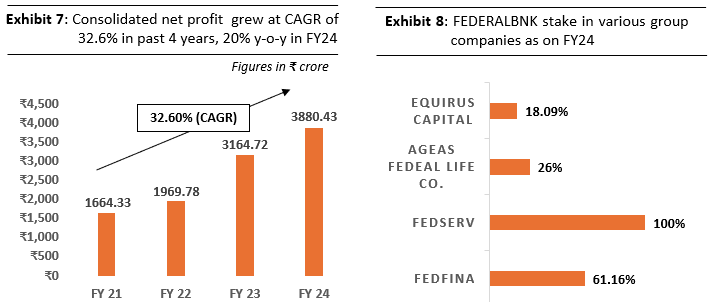

FBL holds a 61.58% stake in FedFina, which specializes in mortgage loans, gold loans, and business loans, targeting self-employed individuals and MSMEs underserved by traditional lenders. With a network of 621 branches across India, FedFina plays a vital role in marketing retail asset products and has established retail hubs in major centers across the country. It employs a dedicated mechanism for the swift processing of retail loans sourced through these channels.

In FY 2023-24, FedFina achieved disbursements worth ₹13,579 crore and Assets Under Management (AUM) of ₹12,192 crore, marking a 34% year-on-year growth. It also reported a Profit Before Tax (PBT) of ₹134.01 crore.

• Federal Operations and Services (FedServ)

FedServ is a wholly-owned subsidiary that delivers operational and technology-driven services to FBL. Located in Bangalore, Visakhapatnam, and Kochi, FedServ is designed to ensure excellence in service delivery, mitigate risks, and achieve cost efficiencies. The services include data entry, IT application support, and document scanning.

In FY 2023-24, FedServ generated ₹78.51 crore in revenue and contributed ₹7.18 crore in Profit Before Tax (PBT).

• Ageas Federal Life Insurance Company

FBL holds a 26% stake in Ageas Federal Life Insurance Company Limited, a joint venture with Ageas. The company began offering life insurance products in March 2008 and has since expanded to provide 31 life insurance solutions across wealth management, retirement, and protection categories.

In FY 2023-24, the company demonstrated strong performance, with new business premiums growing by 32% year-on-year, showcasing its strong market presence and financial health.

• Equirus Capital

Equirus Capital Private Limited, where FBL owns a 19.59% stake, focuses on investment banking, wealth management, and institutional equities. Its comprehensive services include insurance broking, portfolio management, and advisory solutions.

In FY 2023-24, Equirus Capital contributed ₹8.69 crore to FBL’s consolidated profit, further, it is strategically important for complementing the group’s financial service offerings.

Exhibit 6: Federal Bank Subsidiaries and Associate Companies

Source: Investor presentation

Source: Annual report

The subsidiaries and associate companies of Federal Bank maintained steady performance, contributing to the group’s consolidated net profit of ₹3,880.43 crore in FY24, compared to ₹3,164.72 crore in FY23. This reflects significant growth and strong financial outcomes for the group.

Subsidiaries and associates significantly bolster FBL’s consolidated performance through their focused offerings and consistent growth. FedFina remains the top contributor with strong disbursement growth and profitability. FedServ enhances operational efficiency for FBL. Ageas Federal and Equirus expand FBL’s reach into life insurance and investment banking, diversifying revenue streams.