NSE: FEDERALBNK

Balance Sheet

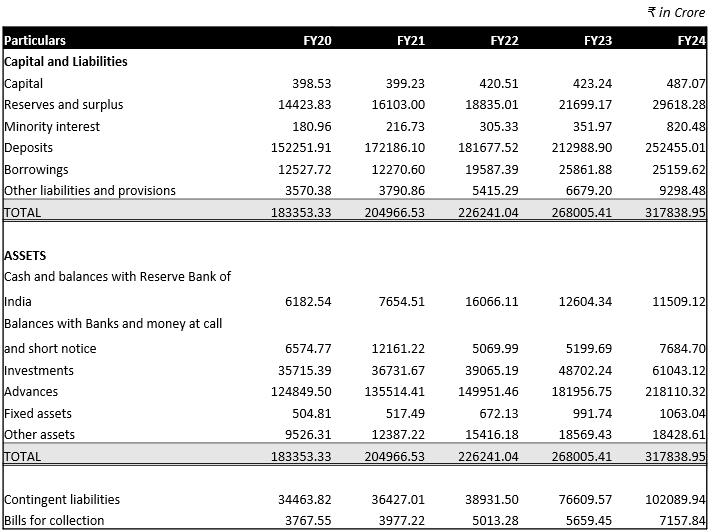

• FBL’s reserves and surplus grew at a strong CAGR of 15.5% over the last five years, driven mainly by consistently high operational profits. In FY24, reserves and surplus increased significantly by 36.5%, rising from ₹21,083 crore in FY23 to ₹28,607 crore. This growth was primarily due to FBL’s highest-ever annual net profit of ₹3,721 crore, a 24% increase compared to the previous year. Additionally, FBL boosted its share premium by issuing 230,477,634 equity shares through Qualified Institutional Placement (QIP) and 72,682,048 equity shares through a preferential allotment during FY24.

• FBL reported a significant 133% increase in minority interest during FY24, driven by two main factors. First, Federal Bank reduced its stake in Fedbank Financial Services Limited (FedFina) from 73.21% at the end of FY23 to 61.58% during the year. Second, FedFina issued additional shares, which contributed to the growth in minority interest. These issuances included 42,881,148 shares as part of the company’s Initial Public Offering (IPO) and 4,594,146 shares issued to employees exercising stock options.

• FBL achieved an impressive deposit growth of 18.35% during FY24, significantly surpassing the industry average of 13.47%. This growth can be attributed to FBL’s successful expansion strategy, which included adding 141 new banking outlets in FY24. FBL also focused on attracting customers to increase deposits.

Additionally, the introduction of innovative products, like Stellar, played a crucial role. Stellar offered a “fit-for-all” proposition with bundled wellness benefits and other attractive features, which quickly gained popularity. Since its launch in February 2024, the product helped FBL acquire around 17,000 New-To-Bank (NTB) customers. Moreover, FBL introduced SHRENI, a product tailored for the Trust, Association, Society, and Club (TASC) segment. SHRENI targeted both current and savings account portfolios through institutional accounts. Retail deposits accounted for 94% of total deposits in FY24, reflecting FBL’s strategic focus on this segment.

• FBL’s advances grew at a CAGR of 11.63% over the past five years, reaching ₹2,18,110 crore in FY24. This growth was driven by strong performance across its business segments, with the retail credit book growing by 25% year-on-year and wholesale banking advances increasing by 15% year-on-year. Federal Bank’s investment in digital platforms, such as its mobile banking app and WhatsApp lending platform, likely improved its reach and loan origination capabilities. Additionally, partnerships with FinTech companies and other institutions have expanded its distribution channels and enabled access to new customer segments

• FBL’s contingent liabilities grew by 162.23% in two years, reaching 32.12% of its total assets in FY24, driven mostly on account of mainly due to liabilities from outstanding forward exchange contracts. A recent study shows [1] that this trend is common among Indian banks, varying by business strategy and risk appetite. Public sector banks are cautious, with 41% exposure, while private banks, being more risk-oriented, show 110% exposure.

Profit & Loss Statement

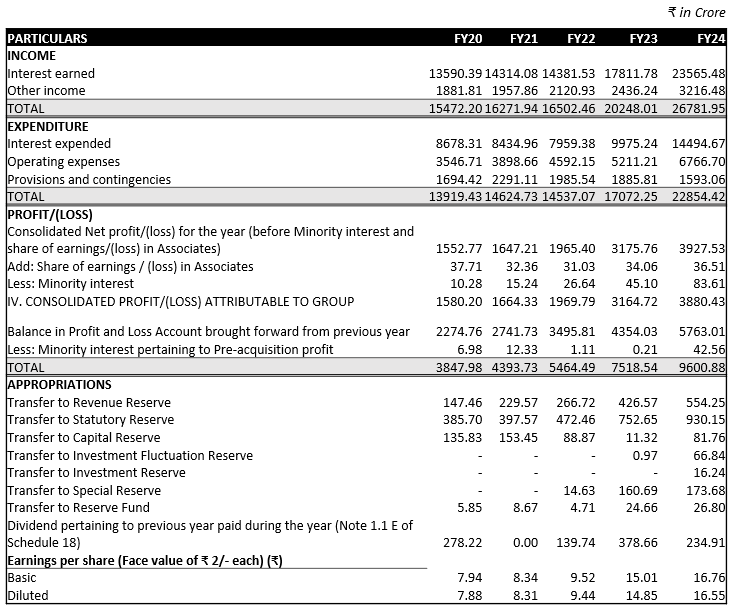

• In FY24 both interest income and other income increasing by 32.3%, net interest income surged by 15% year-on-year (YoY) to ₹8,293 Crore, driven by a 20% expansion in Net Advances, which reached ₹2,09,403 Crore. FBL’s Yield on Average Advances improved as well, rising to 9.35% in FY24 from 8.56% in the previous year.

• Non-Interest Income grew by substantial 32% YoY growth to ₹3,079 Crore, bolstered by a 19% increase in Fee Income, reflecting FBL’s efforts to diversify revenue beyond interest income. Subsidiaries like Fedfina played a significant role, with Fedfina’s total revenue increasing by 34%, driven by a 22% growth in its loan book.

• FBL is looking forward to pivot toward the retail segment, which generally offers higher yields compared to wholesale banking. Retail advances grew by 25% YoY to ₹67,435 Crore, now accounting for 31% of total advances. Microfinance saw remarkable growth of 141%, while the share of high-yielding unsecured products, such as credit cards and personal loans, increased, boosting profitability and effectively managing credit risk.

• To support sustained growth, FBL has been expanding its geographical footprint, particularly in high-growth regions like Gujarat, Maharashtra and Karnataka . It is also focusing on digital lending and forming partnerships with FinTech companies to enhance customer acquisition and outreach. These initiatives are expected to further drive revenue growth and tap into new customer segments.

• FBL experienced a rise in expenses during FY24. Both interest expenses and operating expenses showed substantial increases. Interest expenses, surged by 45.31% year-on-year while the operating expenses, rose by 29.85%.

• Federal Bank saw a significant 18% growth in deposits, reaching ₹ 2,52,534 Crore in FY24. While this growth is positive for FBL’s business, it also means higher interest costs to maintain those deposits. Moreover, the average interest rate FBL paid on deposits increased from 4.58% to 5.63%. This was driven by a few key trends like bank shift towards term deposits which showed a 24% y-o-y growth in FY24 and targeting high value customers like HNIs.

• Rising Interest Rate Environment; to curb inflation, the Reserve Bank of India (RBI) has steadily increased interest rates in recent years, leading to a higher overall cost of funds for banks. Since May 2022, the RBI has raised the repo rate by 250 basis points, bringing it to 6.5%. As of Q2 FY24, 51% of FBL’s loan book consists of loans based on the External Benchmark Lending Rate (EBLR), predominantly linked to the repo rate, making them highly sensitive to these rate changes.

• In addition to deposits, FBL’s borrowings from other sources also grew at an average rate of 19% over the last five years, adding to its interest expenses. Increase in operating expenses were primarily driven by its aggressive growth strategy and investments in technology. Expanding its branch network and entering new business areas led to higher costs related to staffing, infrastructure, and marketing.

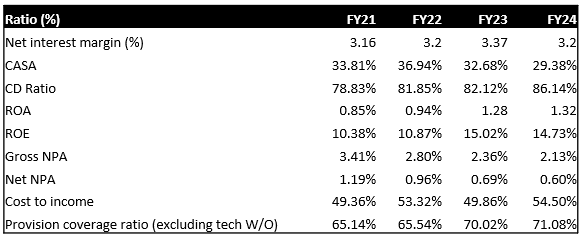

• The provisions and contingencies of Federal Bank have consistently declined, with a compound annual growth rate (CAGR) of -1.5% over the past five years and a notable year-on-year drop of about 15% in FY24. This trend indicates improved asset quality, evidenced by a Gross Non-Performing Assets (GNPA) ratio of 2.13% and a Net Non-Performing Assets (NNPA) ratio of 0.60% in FY24. Additionally, the Provision Coverage Ratio (PCR) rose by 106 basis points to 71.08%, reflecting a solid buffer against loan losses.

•Key improvements in asset quality stem from enhanced credit risk management practices, including rigorous credit assessments and stricter lending criteria, particularly for personal loans. Federal Bank has also diversified its portfolio by focusing on smaller retail loans, which reduces reliance on any single borrower or sector. Enhanced collection efforts through data analytics and digital tools further bolster recovery rates.

• In FY24, Federal Bank reported a 23.58% increase in standalone net profit, totaling ₹3,721 crore, driven by a 14.68% rise in Net Interest Income (NII) and a 32% increase in non-interest income. Although operating expenses surged by 30%, the growth in income compensated for these costs. The Net Interest Margin (NIM) peaked at 3.31% in FY23 but dipped to 3.20% in FY24 due to rising deposit costs, which increased to 5.63%.

• The cost-to-income ratio rose to 54.5% in FY24 as operating expenses escalated amid branch network expansion and digital infrastructure upgrades aimed at long-term growth. Despite these challenges, Federal Bank’s strategic focus on higher-yielding segments has improved returns while necessitating higher operating costs for customer acquisition and servicing.

Cash Flow Statement

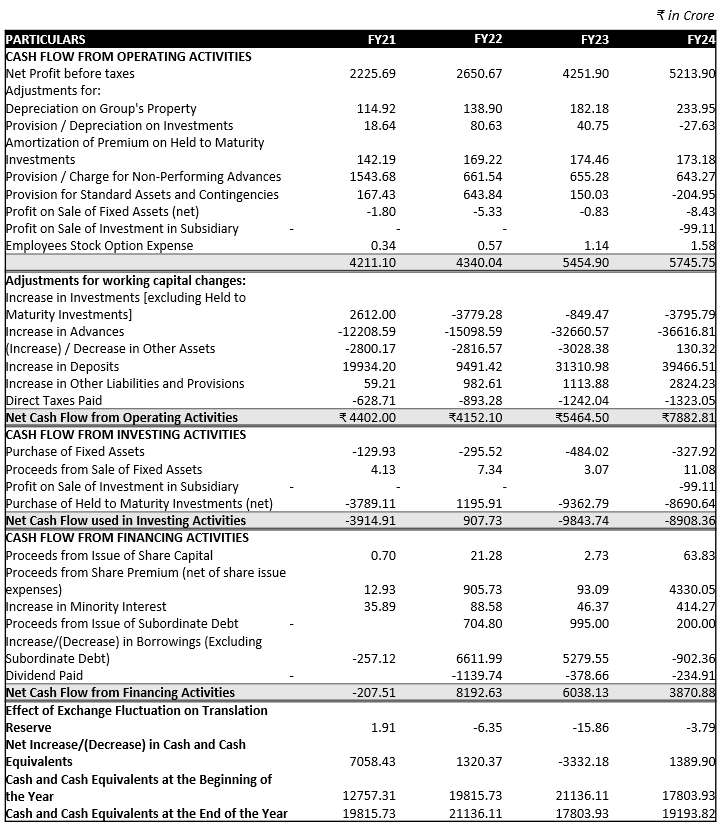

• The cash flow from operating activities in FY 24 rose significantly to ₹7,882.01 crore, compared to ₹5,454.90 crore in FY 23. This increase was mainly due to higher profits before taxes, which reached ₹5,745.75 crore, up from ₹4,251.90 crore in FY 23. Provisions for non-performing assets also increased to ₹204.95 crore from ₹83.65 crore in the previous year, while depreciation rose slightly to ₹233.95 crore. However, there was a notable outflow in investments (₹3,795.79 crore) and advances (₹39,466.51 crore), both much higher than FY 23. Tax payments also increased to ₹1,528.43 crore from ₹1,424.04 crore, reflecting better profits.

• The bank spent heavily on investments in FY 24, with a net cash outflow of ₹8,806.56 crore, similar to the ₹9,843.74 crore outflow in FY 23. Most of this came from purchases of long-term investments worth ₹8,690.64 crore and fixed assets costing ₹327.92 crore. On the other hand, proceeds from selling fixed assets were minimal at ₹3.07 crore. This shows the bank is focusing on building long-term assets despite high expenses.

• Cash flow from financing activities turned positive in FY 24, showing an inflow of ₹808.56 crore compared to an outflow of ₹1,192.65 crore in FY 23. The improvement was due to ₹63.83 crore raised from share capital and ₹4,330.05 crore from share premiums, a significant increase over ₹33.09 crore in FY 23. However, dividend payments to shareholders also went up to ₹486.05 crore from ₹378.66 crore, reflecting higher returns.

• The bank saw a sharp rise in cash balances in FY 24, with net cash increasing by ₹8,808.56 crore, up from ₹4,549.16 crore in FY 23. By the end of FY 24, cash and cash equivalents stood at ₹19,657.13 crore, compared to ₹17,093.93 crore in FY 23. This growth was supported by strong cash inflows from operations.

Future Projections

• FBL is focusing on digital transformation to enhance customer engagement, streamline operations, and increase fee income from digital transactions. The bank is also prioritizing high-margin retail products like personal loans and microfinance to improve net interest margins (NIM), which are expected to rise slightly to 3.25% in a best-case scenario. However, geopolitical factors, including potential U.S. policy changes and Middle East instability, may reduce remittance income by 10% over three years. Meanwhile, the Reserve Bank of India’s monetary policy, including a CRR cut, has added liquidity to the banking sector, supporting loan and deposit growth.

• Federal Bank is on a growth trajectory, with total deposits projected to reach ₹414,795 crore by FY27, growing at a 17% YoY rate. This growth will be driven by increasing digital adoption, supported by rising internet penetration in India and Federal Bank’s efforts to enhance its digital banking services. The recent policy adjustments by the RBI, including a CRR cut by 50bps, are expected to boost liquidity and further support deposit gathering. Additionally, the bank’s expansion into high-growth states and targeted marketing campaigns are likely to attract a broader customer base, improving deposit growth.

• Loan growth is projected to increase by 20% YoY under the base-case scenario, with the total loan book reaching around ₹375,665 crore by FY27. This growth is driven by strong demand for retail and MSME loans, supported by favorable economic conditions and increasing financial inclusion. Federal Bank’s shift towards granular retail products like personal loans and microfinance aligns with market demand and offers high-margin opportunities. The RBI’s accommodative monetary policy and stable interest rate environment further support credit growth

• The bank’s Net Interest Margin (NIM) is projected to improve to 3.25% due to effective cost management, including projected increase CASA deposits and a shift to granular retail portfolio. This, coupled with a stable interest rate environment and proactive rate management, will help the bank maintain favorable NIMs despite increased competition.

• GNPA ratio is projected to remain stable at 2.13% over the next few years. This stability is supported by a moderate economic environment, effective risk management practices, and sectoral diversification efforts. There might be slight uptick in NPA figures due to the localized risks in Kerala due to natural disasters like floods and landslides, which could impact repayment capabilities, despite that the bank’s proactive risk management and diversification strategies will help maintain good asset quality across its diverse portfolio.

• Net profit margin is likely to remain steady at 32.7%, this is primarily driven by fee income growth from digital banking services, expected to grow by more than 15% year-over-year. Additionally, operational efficiency, cost control, and a stable economic environment will support profitability even as the bank scales operations. FBL’s strategic focus on retail lending, combined with digital transformation and a balanced approach to managing macroeconomic risks, positions it well to adapt to changing market conditions. While external factors such as geopolitical events may impact remittance income, the bank’s proactive risk management and diversified revenue streams are expected to sustain profitability and growth over the next 3 to 5 years. 1

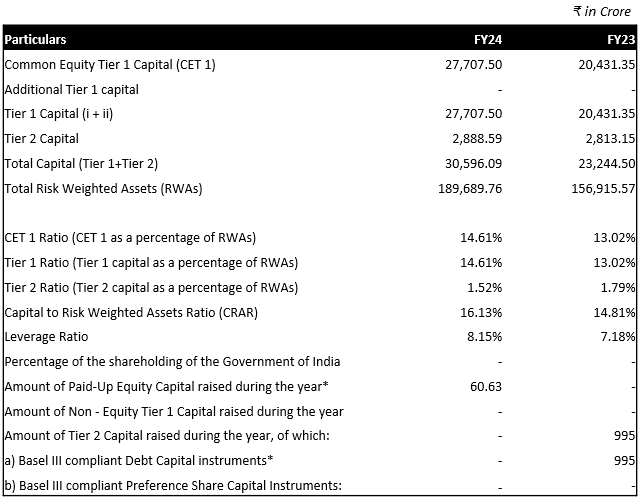

Financial Ratios: 1

Capital Adequacy Ratio: 1 2