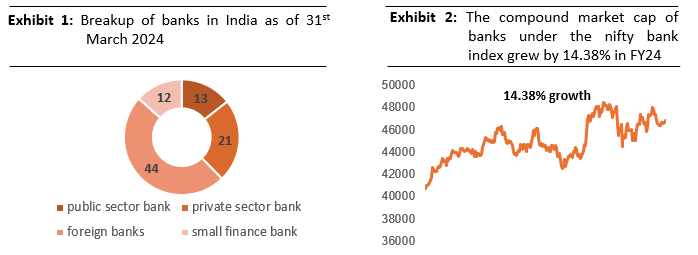

Current State of the Banking Industry: 5

In FY24 the Indian banking sector has showcased notable resilience despite global challenges like the Russia-Ukraine conflict. The Reserve Bank of India (RBI) maintaining the policy repo rate at 6.5%, aiming to control inflation and support economic growth. Even the economic environment saw several changes, such as the withdrawal of ₹2,000 notes, the merger of HDFC Ltd. with HDFC Bank, and the imposition of the incremental Cash Reserve Ratio (CRR), all of which influenced the banking sector’s operations.

Source: IBEF industry report

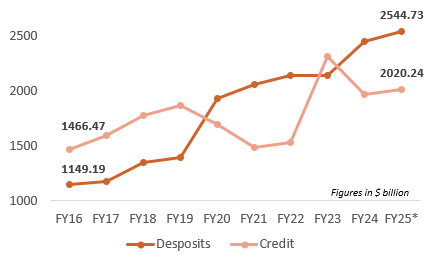

• As of July 2024, bank credit stood at ₹168.12 lakh crore (US$ 2,020 billion), while deposits reached ₹209.36 lakh crore (US$ 2,544.7 billion). Over the last decade, bank credit grew at a CAGR of 3.34%, and deposits at 9.23%, driven by rising incomes and robust savings.

• Credit growth across sectors remained strong, with Scheduled Commercial Banks (SCBs) disbursing ₹164.3 lakh crore, reflecting a 20.2% year-on-year increase in FY24. This was fueled by personal loans, housing credit, and agricultural lending.

• The asset quality of banks improved significantly, with the Gross Non-Performing Assets (GNPA) ratio dropping to 2.8% by March 2024, a 12-year low, from 11.2% in FY18. This improvement was due to better borrower selection, effective debt recovery, and stronger governance structures. The top 10 Indian banks maintained strong asset positions, with more than 50% of their assets in loans, making them resilient to rising interest rates

• Digital payments adoption has surged, with Unified Payments Interface (UPI) transactions crossing ₹15 lakh crore monthly. Additionally, the government’s efforts under the Pradhan Mantri Jan Dhan Yojana (PMJDY) have expanded banking access, resulting in over 50 crore accounts by FY2024, further boosting deposit mobilization, particularly in rural and semi-urban areas

• The banking sector experienced growth in agriculture, housing, and industrial lending. The government and RBI focused on low-cost loans for MSMEs and stable credit to the services sector. Housing loans rose significantly from ₹19.9 lakh crore in March 2023 to ₹27.2 lakh crore in March 2024.

Exhibit 3: Deposits Poised for Strong Growth (9.23% CAGR) as Credit Expansion Slows (3.62% CAGR) in the Years Ahead (FY16-FY25E)

Source: Annual report

Key Industry Developments: 5

• Digital Innovations: The Reserve Bank of India (RBI) launched a pilot project on Central Bank Digital Currency (CBDC) in November 2022 with the use case of settlement of secondary market transactions in government securities, hence making inter-bank markets more efficient.

• Cross-Selling Strategies: Indian banks have widely adopted cross-selling strategies, including selling retail insurance products, to diversify their offerings, leverage their vast customer base and data for delivering personalized products, and increase their income through fees and commissions.

• The industry invests heavily in expanding the ATM network, driving financial inclusion. Even the Indian government has worked to expand banking access, particularly in rural and underbanked areas. Over 2,796 ATMs were added in just four months of FY23, surpassing the numbers from the previous two years. This model improves customer convenience by ensuring ATMs are more accessible, reducing reliance on distant bank branches.

• Global Expansion: Indian banks expanded internationally through subsidiaries, resulting in a 0.5% increase in employee numbers for foreign branches and a 6.2% rise for subsidiaries.

• Rural Banking Progress: Efforts in rural lending aim to serve 60% of the underbanked rural population. All new rural accounts are now opened digitally.

• A digitalized system for Agri-finance, conceptualized by RBI and RBI Innovation Hub (RBIH), aims to simplify the delivery of Kisan Credit Card (KCC) loans.

Credit growth has been robust and inclusive, reaching all population groups (rural, semi-urban, urban, and metropolitan) and regions of the country. It spans public, private, foreign, regional rural, and small finance banks. India is also the largest market for Android-based mobile lending apps, accounting for 82% of global online lending.

Prospects for Indian banking sector: 5 6 7

• Credit growth in the banking sector stood at 15.6% year-on-year as of FY 2023-24, fueled by higher demand from retail, agriculture, and MSME sectors. Retail loans, which contribute significantly to credit growth, showed an annual growth rate of 18.2%, this trend is projected to continue, particularly in urban and semi-urban areas, as banks increase their focus on high-margin retail loans.

• Gross Non-Performing Assets (GNPA) for Indian banks declined to 3.9% in FY 2023-24, marking a significant improvement over the past five years. Continued emphasis on better borrower selection, improved debt recovery processes, and digital credit monitoring is expected to further stabilize GNPA levels at 2.5% by FY27. The Net NPA ratio, currently at 1.2%, is also anticipated to decline gradually, ensuring stronger balance sheets for banks.

• Digital payments are expected to account for 65% of all transactions by 2026, driven by Unified Payments Interface (UPI) adoption and rapid fintech growth. UPI transaction volumes, currently exceeding ₹15 lakh crore per month, are likely to grow at a CAGR of 25–30% over the next five years. Increased digital adoption will generate additional fee-based income, enhance operational efficiency, and improve customer engagement for banks.

• Government initiatives towards financial inclusion like the Pradhan Mantri Jan Dhan Yojana (PMJDY) continues to drive financial inclusion, with over 50 crore accounts opened as of FY 2024. These efforts have contributed to higher deposit mobilization and expanded the banking sector’s reach into rural areas, fostering inclusive growth in the future.

• With a government focus on supporting the MSME sector, credit to MSMEs saw a growth of 23.7% in FY 2024, providing a key area of growth for banks. Green financing is gaining traction, with a shift towards financing renewable energy projects and sustainable initiatives, which aligns with global environmental goals.

The Indian banking sector continues to show immense potential for growth, driven by robust economic expansion, government reforms, and technological advancements. With India’s GDP growth projected at 7 to 7.5% for FY 2024-25, the banking sector is poised to benefit from the increasing demand for credit across industries. 16

Rapid adoption of digital technologies, a growing FinTech ecosystem, and strong government initiatives aimed at financial inclusion are further transforming the sector. Rising incomes, urbanization, and an expanding working-age population are expected to drive sustained growth in banking services, including retail, housing, and MSME lending. These factors collectively position India’s banking sector to be on a trajectory to become the third-largest globally by 2050. 15