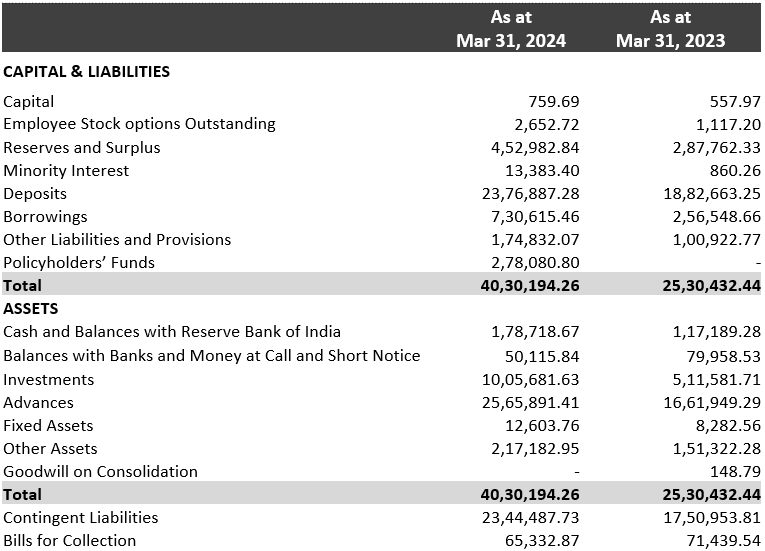

The Financial Year 2023-24 was the year of the merger. The Balance Sheet size grew by 46.7% in the fiscal, with a 26.% increase in Deposits and a 55.2% growth in Advances. The Bank consolidated its position as the largest private sector bank by Balance Sheet size in India without compromising its asset quality.

Increase in capital & reserves:

HDFC Bank is now the largest private sector bank in India with top 3 position in highest capital after its merger with HDFC limited which lead to a market cap of Rs. 12,00,000 cr . This is the reason for increase in capital & reserve in bank.

Increase in deposits & advances:

• Both the metrics increased, but advances increased by 54% due to the merger as the term loans for housing given by HDFC Ltd were now also included in bank’s advances portfolio.

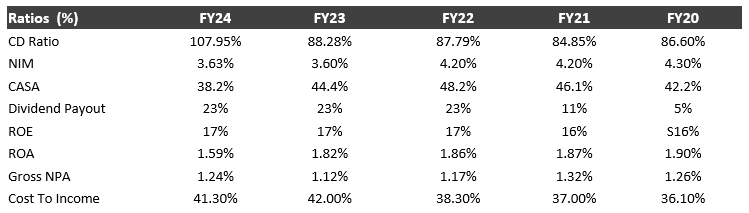

• Compared to increase of 26% in deposits because HDFC Ltd. Is an NBFC which does not lead to any addition in deposits of the bank rather it increased the burden on bank by impacting its CD ratio and taking it to 107% in Fy24.

Future outlook: Bank’s advances to grow at a rate of 17% to 18% over the next few years, with a focus on retail loans, including home loans and personal loans.

• Retail deposits are expected to continue growing robustly, with a target of around INR 1 trillion in accretion over the next few quarters. The bank has reported a year-on-year growth of 21.5% in retail deposits, which is likely to sustain.

Increase in borrowings & liabilities:

The increase in borrowings & liabilities is due to the high cost borrowings brought in due to merger . As, HDFC LTD. Used to finance its advances through bonds which led to higher interest expenses.

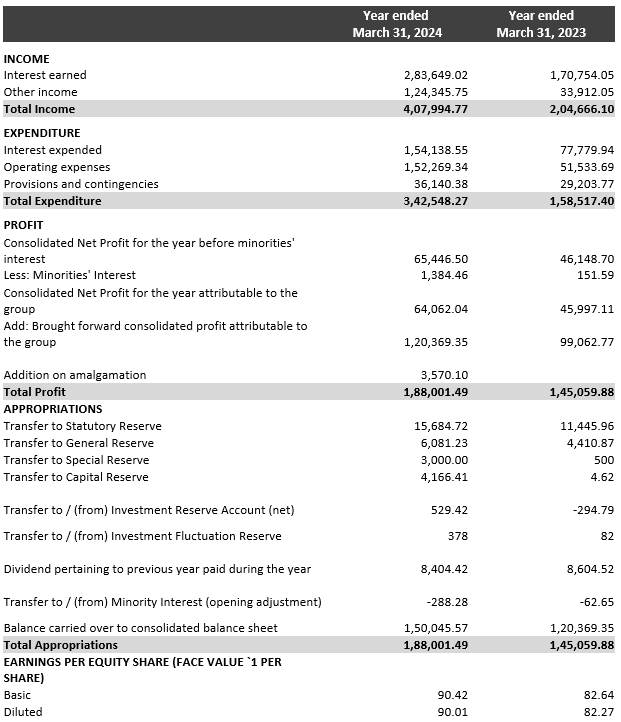

Increase in income & expenses:

• Increase in income by 99% is due to increase in interest earned as the merger contributed to this by combining the loan portfolios and also by increase in other income due to enhanced cross selling opportunities and broader product portfolio.

• Increase in expenses by 116% is due to increased interest expense due to higher borrowing cost inherited from HDFC’s loan book and increased operational expenses due to integration cost & expanded operations post merger.

Increase in CD ratio:

• Sudden increase in CD ratio is due to increased credit due to merger as the HDFC Ltd. Credit were also included in credit profile of HDFC bank but no contribution of merger in deposits because HDFC ltd., was an NBFC and it was not allowed to accept deposits.

No impact on NIM:

No positive impact was seen on NIM even after such a huge merger due to high cost borrowings brought in by the merger and other increased expenses.

Future Outlook: NIM expected to grow steadily, driven by strong advances growth and an increasing retail deposit base. The bank aims to maintain a core net interest margin around 4.1% to 4.3%.

Profit & Loss Statement

Balance Sheet

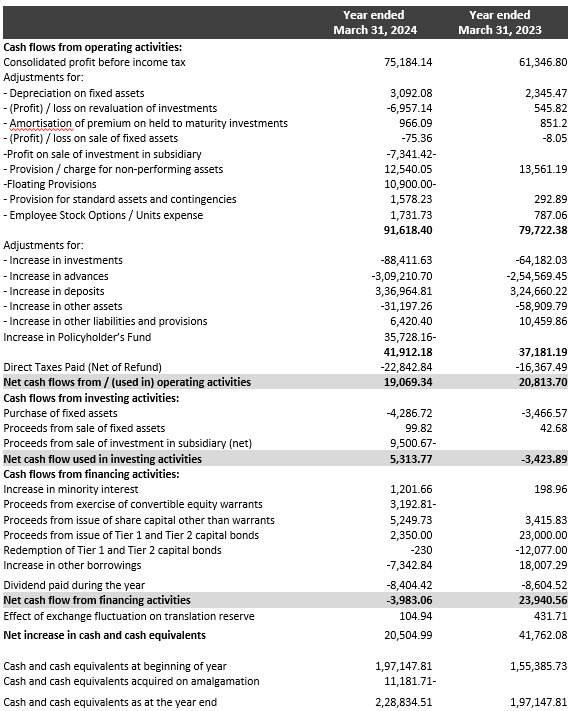

Cash Flow Statement

Financial Ratios

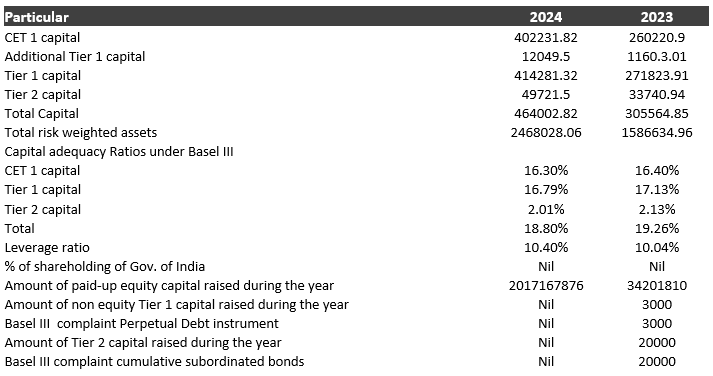

Capital Adequacy Ratio