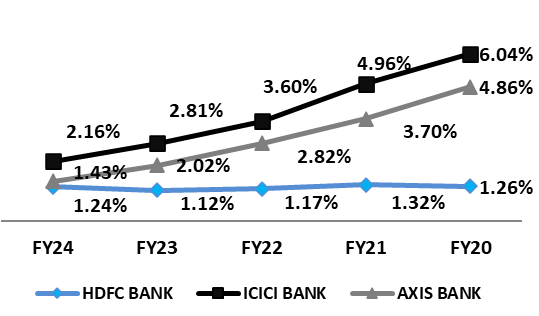

Exhibit 1: Continuous decline in Gross NPA from 6.04% to 2.16% in HDFC Bank

•HDFC bank has maintained a low and stable Gross NPA, indicating strong asset quality and effective risk management.

• ICICI Bank and Axis Bank, both have made significant strides in reducing their Gross NPAs, reflecting successful strategies in managing and recovering bad loans.

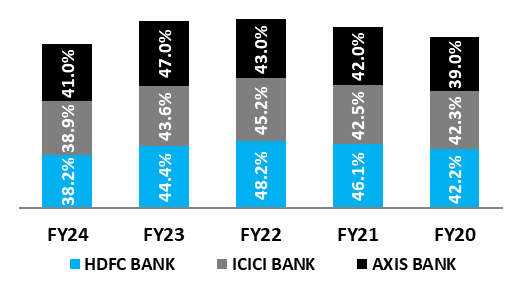

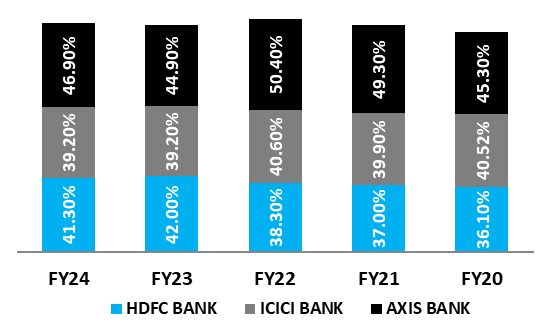

Exhibit 2: 6% decline in CASA of HDFC Bank in FY24

•Initial increase in CASA Ratio suggests improved deposit mobilization in low-cost accounts, but subsequent decline indicate a change in deposit mix due to a higher proportion of term deposits from HDFC Ltd., which typically have higher interest costs compared to current and savings accounts.

• Axis Bank shows fluctuating trend & ICICI Bank shows consistent increase in low cost deposits.

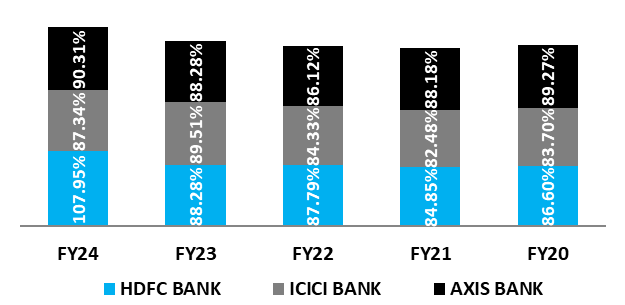

Exhibit 3: Sudden increase from 88% to 107% in CD ratio of HDFC Bank

• CD Ratio of HDFC bank shows a huge spike which occurred due to increase in credit due to the merger of HDFC Bank & HDFC Ltd and no deposits brought in by HDFC Ltd., as it is an NBFC. HDFC bank should focus on bringing down the CD ratio for a stable liquidity position.

•ICICI Bank shows a conservative approach with a significant drop in CD ratio, improving liquidity & Axis Bank exhibits fluctuations but maintains a CD ratio around 90%.

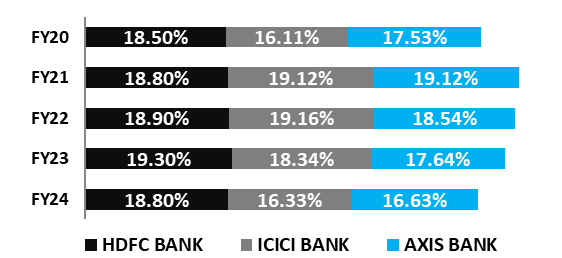

Exhibit 4: Stable capital adequacy ratio of HDFC Bank

•HDFC Bank: The CRAR has shown a consistent upward trend, indicating strong capital adequacy and a robust financial position.

• ICICI Bank: The CRAR has also increased over the years, reflecting improved capital strength and risk management.

• AXIS Bank: The CRAR has fluctuated but generally shows an upward trend, suggesting efforts to maintain adequate capital levels.

Exhibit 5: Slight rise in Cost to income ratio in all 3 banks

A lower cost-to-income ratio is preferable as it indicates higher efficiency. The trends suggest that while HDFC Bank has maintained steady efficiency, ICICI, and AXIS Banks have faced more variability in their operational efficiency.

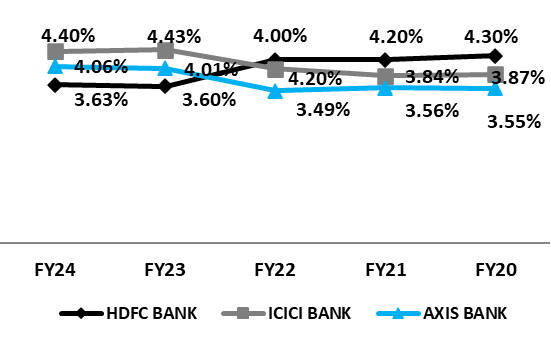

Exhibit 6: Improvement in NIM in all 3 banks but no positive impact of the merger on NIM of HDFC bank

• Overall, all three banks have shown improvements in their NIM over the five-year period, which is a positive sign for their financial health and operational efficiency.

• But, HDFC bank does not show any impact on NIM in FY24 even after the merger due to high cost liabilities (borrowings) brought in by the merger, change in interest rates by RBI to control inflation, increasing the cost of funds for bank. Also, change in CD ratio impose pressure on NIM due to higher interest expenses on bank.

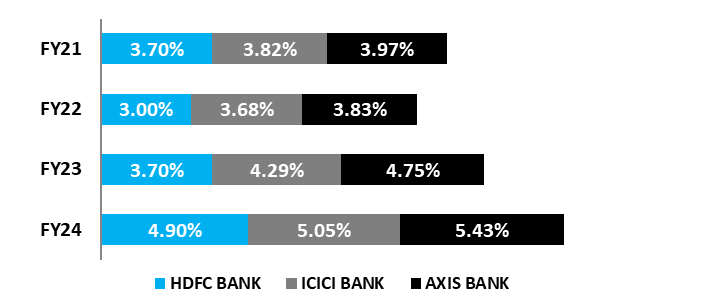

Exhibit 7: Increase in cost of borrowing from 3.70 in Fy23 to 4.90 in FY24 due to high-cost borrowings brought in by the merger

Overall, while all three banks have experienced slight increases in their cost of borrowing, HDFC Bank has managed to keep its costs relatively stable compared to ICICI Bank and AXIS Bank.

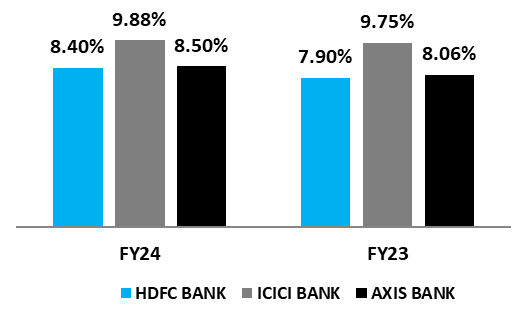

Exhibit 8: Continuous increase in yield on advances

HDFC, Axis, and ICICI Bank show an increase in yield on advances, which suggests that the bank has been able to generate higher interest income from its loans.

Performance

Catalysts

Merger with HDFC Limited:

The merger of HDFC Bank with HDFC Ltd., will enhance capital base of bank, reduce unsecured loan exposure of bank, increase scale and market presence which would provide a solid foundation for future growth and expansion.

Digital Transformation and Technology Investments:

HDFC Bank has been heavily investing in digital transformation initiatives. The bank’s focus on enhancing its digital banking capabilities, including mobile banking, internet banking and use of AI or machine learning, is expected to drive customer acquisition and improve operational efficiency.

Expansion of Retail and SME Segments;

The bank is expanding its presence in the retail and small and medium-sized enterprise (SME) segments. This includes increasing its branch network and leveraging digital channels to reach a broader customer base. The growth in these segments is expected to contribute significantly to bank’s revenue & growth.

Micro market focused Multi Format Distribution:

Transforming branch banking into a multi-format model based on a granular micro market approach. This involves using a multi-variate model to identify high potential markets, considering factors such as population demographics, deposits and advances data, delinquency insights, climate risk assessments and future trends. Branch formats may vary from full service physical branches to smart banking lobbies or digital banking units with self-service kiosks as well as business correspondent-based models.

By expanding their presence in identified locations through multiple formats, bank would not only increase their catchment area but also benefit from network effects.

Capturing flows from Government & Institutional (G&I) Business:

• Through continued dominance in agency business, it is the largest collector of Goods and Service Tax demonstrating its market leadership, and a major player1 in direct tax collections and customs duty. The Bank is actively integrated with 9 States/Union Territories for the collection and settlement of various state taxes.

• Partnering with government to go granular like Bank has facilitated digitalization of payments associated with the land acquisition process by aiding district level Government authorities to expedite beneficiary identification and related disbursements.