NSE: IDFCFIRSTB

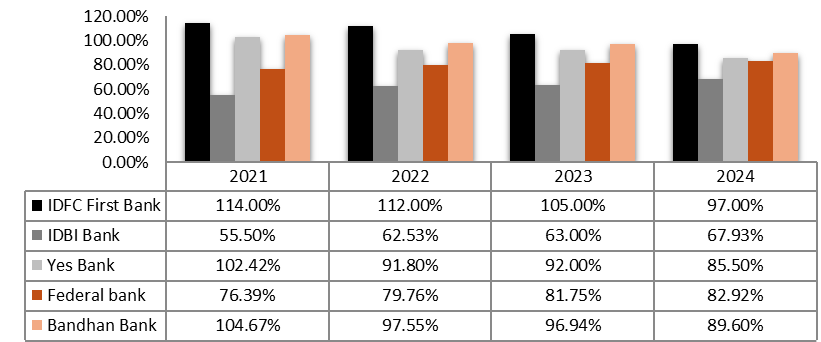

Credit Deposit Ratio (%)

• IDFC banks shows decline in CD ratio because bank is now focusing to rely on deposits only for lending purpose and avoiding borrowings.

• Also, Yes Bank and Bandhan Bank have higher CD ratios (85.50% and 89.60% respectively), suggesting a more aggressive approach in utilizing deposits for lending activities.

• IDBI Bank and Federal Bank have moderate CD ratios (67.93% and 82.92% respectively), showing a balanced approach to deposit utilization for lending.

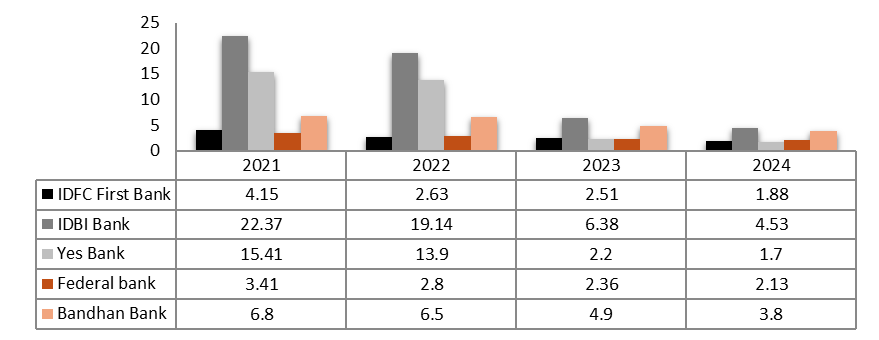

Gross NPA (%)

• IDFC First Bank, IDBI Bank, Yes Bank, Federal Bank, and Bandhan Bank have all shown improvements in Gross NPA percentages over the years.

• Asset Quality: Lower Gross NPA percentages generally indicate healthier asset quality, which is crucial for financial stability and investor confidence.

• IDFC FIRST Bank & Yes Bank has the lowest NPA Levels which is a positive indicator showing high asset quality.

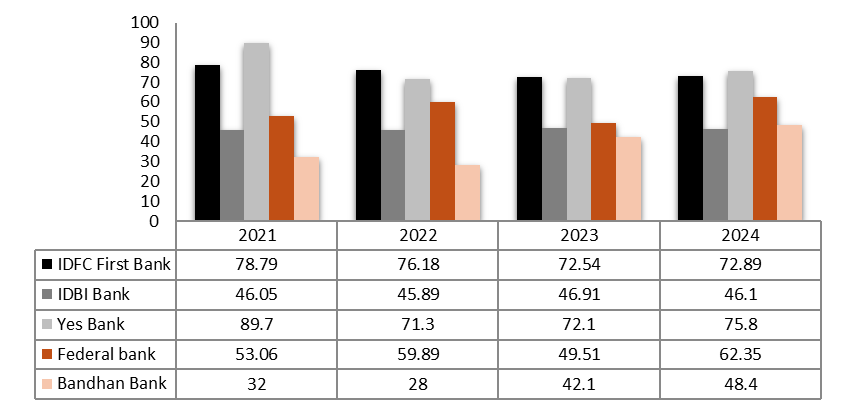

Cost to Income (%)

• IDFC First Bank and Yes Bank demonstrate significant improvements in Cost to Income ratio, indicating enhanced operational efficiency.

• IDBI Bank maintains a stable Cost to Income ratio over the years.

• Federal Bank and Bandhan Bank show fluctuations in their Cost to Income ratios, suggesting varying levels of efficiency in managing operational expenses.

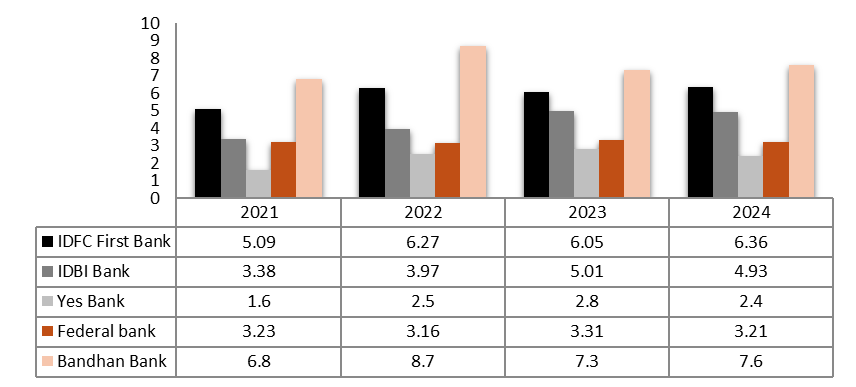

Net Interest Margin (%)

• IDFC First Bank and Bandhan Bank: Both banks demonstrate relatively higher NIMs, suggesting efficient management of interest income and stronger profitability from interest-earning assets.

• IDBI Bank: Shows improvement in NIM over the years, indicating enhanced efficiency in interest income generation.

• Yes Bank and Federal Bank: Both banks show lower NIMs compared to others, but Yes Bank has shown improvement over the years.

Catalysts

Expansion of Retail Lending:

• The bank is focusing on expanding its retail lending portfolio, which is anticipated to be a significant driver of growth. With the Indian credit market projected to grow substantially, capturing a larger share of retail loans, including personal loans, home loans, and auto loans, will enhance revenue streams.

Micro, Small, and Medium Enterprises (MSMEs) Financing:

• Targeting the MSME sector presents a substantial opportunity for growth.

• As the government emphasizes support for small businesses, IDFC First Bank can leverage this trend by offering tailored financial products and services to this segment, thereby increasing its loan book and revenue

Digital Transformation:

• The bank’s investment in digital banking and technology is a critical catalyst for growth.

• By enhancing customer experience through digital channels, streamlining operations, and reducing costs, IDFC First Bank can attract more customers and increase transaction volumes, leading to higher revenues.

Improvement in Deposit Mobilization:

• A strong focus on increasing deposits, particularly through Current Account Savings Accounts (CASA), will help reduce the cost of funds and improve net interest margins (NIM).

• The bank’s goal of achieving a CASA ratio of around 46.5% is a positive indicator for future profitability.

Financial Inclusion Initiatives:

• The bank’s commitment to financial inclusion, particularly in rural and underserved areas, can drive growth by expanding its customer base.

• Offering products tailored to the needs of these segments can lead to increased lending and revenue generation.

=> This would lead to loan growth of around 22-23%, deposit growth of 28%-30%. Also, Bank believe that the next five to ten years will be critical for the bank’s development, and they are focused on executing their strategic plans to capitalize on the growth opportunities in the Indian economy and also follow and achieve their Guidance 2.0 plan long with continued focus on catalysts