NSE: IDFCFIRSTB

• IDFC FIRST Bank was founded by the merger of Erstwhile IDFC Bank and Erstwhile Capital First on December 18, 2018. It is a new age Universal Bank in India built on the foundations of Ethical Banking, Digital Banking, and Social Good Banking.

• As part of technology led banking, the Bank has built a modern technology stack and has built an advanced mobile app with 250+ features.

• As part of the Social Banking theme, the Bank’s business model is naturally geared to social banking. It has developed unique capabilities for financing bottom of pyramid customers with consistently high asset quality.

• The Bank has financed over 40 million customers including 0.3 million SMEs, 0.9 million livelihood (cattle loans), 16 million lifestyle improvement loans (for laptops, washing machine, etc.), 1 million sanitation loans (toilets, water fittings), 6.5 million mobility loans (2-wheelers and cars), and home financing (over 100,000 homes), and 15 million loans to 4.3 million women-entrepreneurs. It also offers other retail and rural loans such as Kisan Credit Cards, harvest financing, gold loans etc.

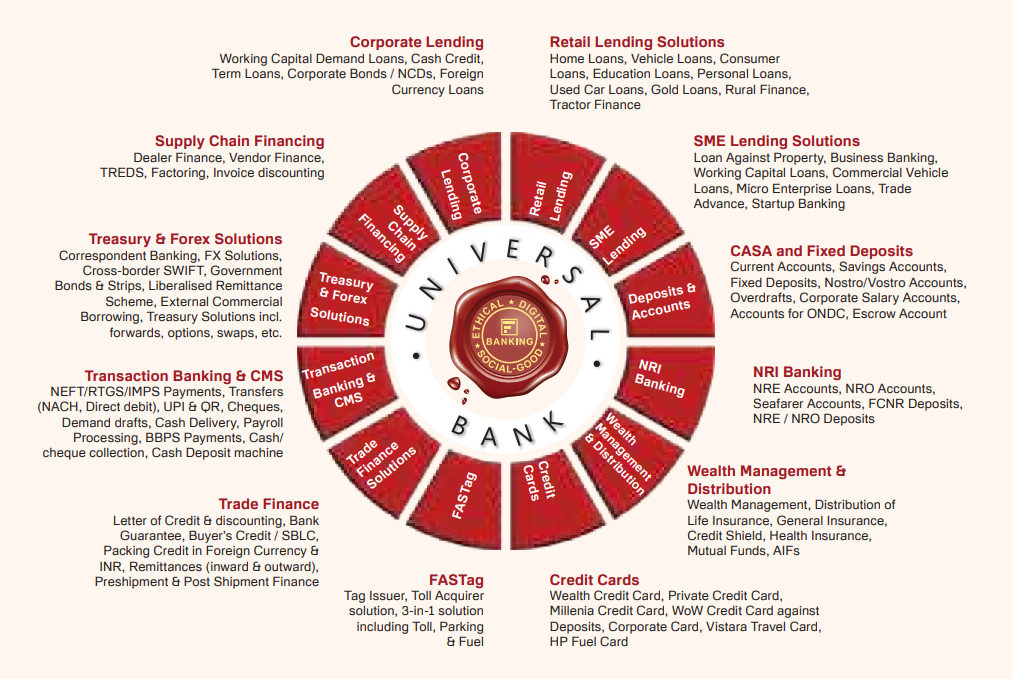

• It is an Universal Bank, and offers end to end Corporate Banking, Trade Finance, Treasury products, SME Banking, Wealth Management, NRI banking, etc.

It deals in various segments like retail banking (60%), treasury (26.9%), corporate/wholesale banking (11.5%) and others (1.7%) which include selling & distribution of third party products.

• It has around 809 branches,249 assets service centers 925 ATMs, and 606 rural business correspondent centers across the country This extensive network indicates a broad presence in 25 states & 3 UTs and suggests that urban and semi-urban regions, where most branches are likely located, contribute significantly to its business.

• It has a market share of around 1.2% in Bank Advances, 0.98% in Bank Deposits,1.8% in credit card transactions, 0.81% in debit card transactions, 1.38% in mobile banking transactions, 1.98% share in Net Interest income, 1.19% in internet banking.

• Also the Bank showed 24% YOY increase in loans & advances, 47% YOY increase in customer deposits with a capital adequacy ratio of 16.82%, ROA of 1.13% and ROE of 10.95%.

About Merger

IDFC FIRST Bank was founded by the merger of Erstwhile IDFC Bank and Erstwhile Capital First on December 18, 2018.

Erstwhile IDFC BANK Ltd.

IDFC Limited was a leading and reputed infrastructure financing Domestic Finance Institution. The institution diversified into Asset Management, Institutional Broking and Investment Banking. It applied for and acquired a Commercial Banking License from RBI. IDFC Bank laid the foundation for a strong banking framework and created necessary systems, risk management, infrastructure, IT architecture and processes for future growth. It created efficient cash management system and treasury and for managing trading.

Erstwhile CAPITAL FIRST Ltd.

The NBFC had businesses of financing such segments within consumer and micro-entrepreneurs that not financed by existing banks, by using alternative and advanced technology led models. Capital First was a successful NBFC, growing its loan book and net profits at a 5 year CAGR of 29% and 56% respectively, with stable asset quality of Gross NPA of <2% and Net NPA of <1% for nearly a decade. Inspite of being a successful consumer and MSME financing entity since 2012 with a strong track record of growth, profits and asset quality,the company was looking out for a banking license to convert to a bank as a part of the original strategy of Mr. Vaidyanathan.

An aspiration for accelerated and sustained growth paved the way for the merger of erstwhile IDFC Bank Ltd and erstwhile Capital First Ltd on December 18, 2018

Issues: Because IDFC Bank was created from an infrastructure DFI, the merged entity had certain issues.

As of December 31, 2018,

a) The Bank had low CASA at 8.68%

b) The Bank had low NIM at 1.9% (H1 FY 19) and low PPOP (Pre-Provisioning Operating Profits) of 0.32% (H1 FY 19)

c) Only 8.04% (Rs. 10,400 crores) was retail Deposits and the rest was institutional deposits & borrowings.

d) The Bank had large exposure in infrastructure and corporate Loans

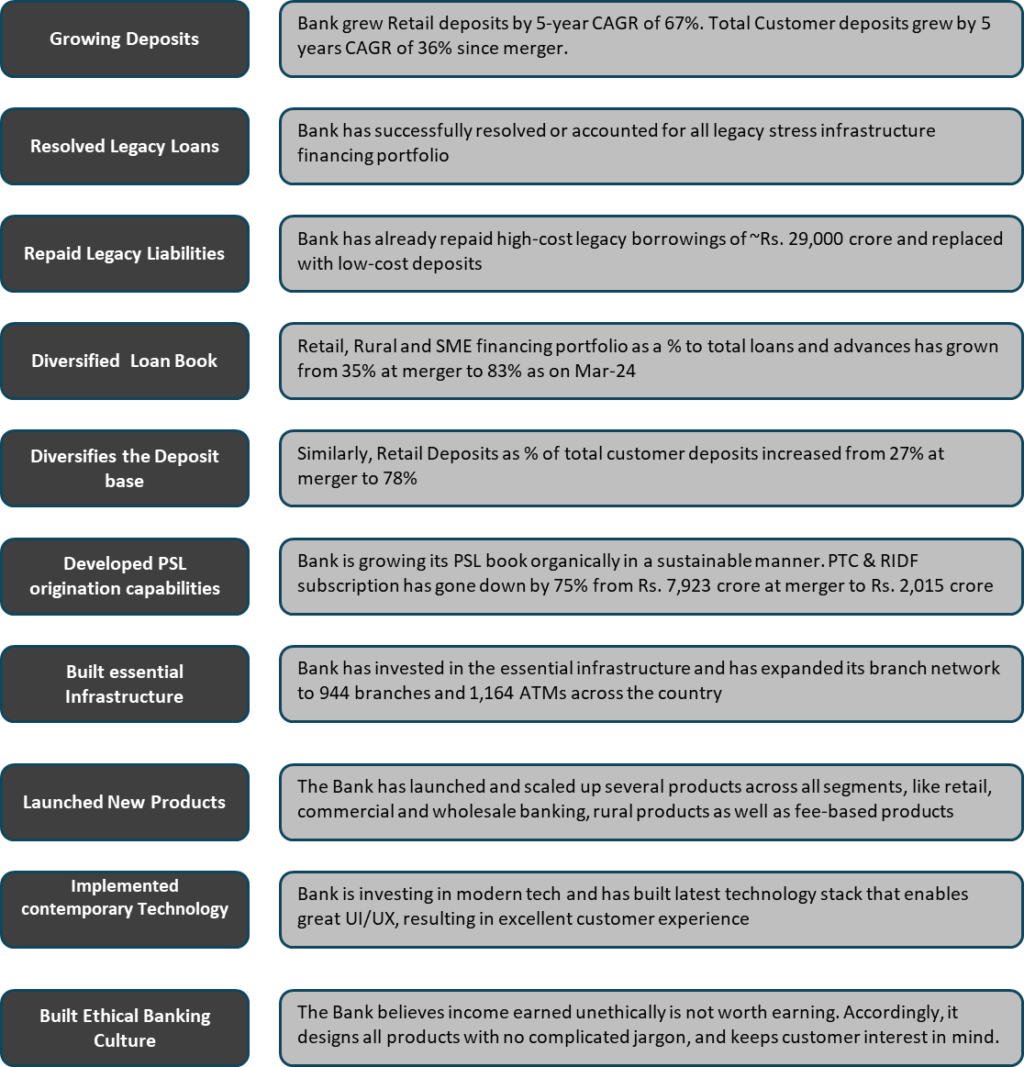

Issues Addressed: Between FY 19-FY 24, the bank has addressed all the issues relating to infrastructure and corporate loans. Infrastructure exposure has reduced from Rs. 21,459 crore to Rs. 2,830 crore, CASA has grown to 47.25%, and profitability has increased to 2,957 crores in FY24.

Achievements of 5 Years since merger

Wide Product Suite of IDFC FIRST Bank