NSE: PAYTM

Payment Services

Paytm’s revenue from Payment Services grew 26% to ₹6,236 Cr. in FY24 from ₹4,930 Cr. in FY23. Net payments margin from FY22 to FY24 grew at a CAGR of 108.61% going from ₹697 Cr. in FY22 to ₹2,955 Cr. in FY24.[5]

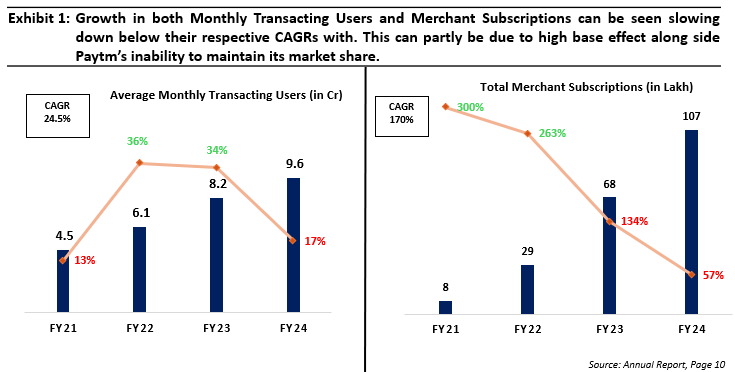

Paytm charges merchants a transaction fee based on a percentage of the Gross Merchandise Value (GMV). Due to the increased adoption of on-app/online payment methods, Paytm’s Monthly Transacting Users (MTU) grew by 17.07% year-on-year (YoY) to 9.6 Cr. in FY24, up from 8.2 Cr. in FY23.[10]

Government of India has provided incentive to digital payment apps like Paytm and PhonePe to promote RuPay Cards and low-value BHIM UPI transactions for P2M transactions. (₹182 Cr. was paid in FY23).[3]

Mid-sized and large retailers use Paytm’s POS devices for mobile and card payments, generating Merchant Discount Rate (MDR) and subscription revenues. Online and omnichannel merchants benefit from Paytm’s payment gateway, generating MDR revenue and platform fees.

Fees for the respective payment mediums are provided in the table below. [3]

Soundbox and Other Subscription Revenue- Merchants use Paytm’s payment devices like Soundboxes and EDC machines. The number of deployed payment devices rose from 68 lakh in 2023 to 107 lakh in 2024, with 1 Cr.+ merchants currently subscribed.

The price point for the Paytm Soundbox starts at ₹299 if purchased, and merchants pay ₹125 per month if it is taken on rent.[4] The Soundbox has a 12-day battery backup and comes in 11 regional languages. The EDC (electronic data capture/card machine) devices come at a monthly subscription price of ₹3,499.[4]

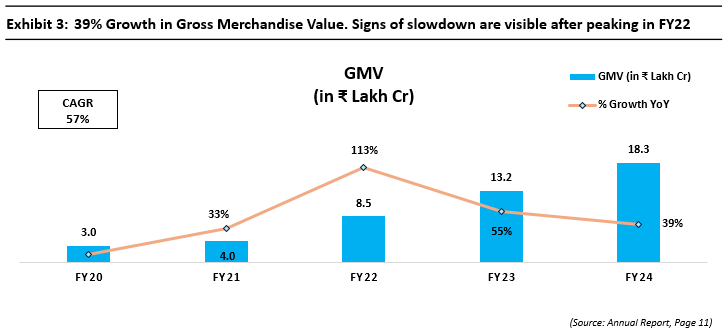

The company’s Gross Merchandise Value (GMV) grew 39% YoY, reaching ₹18.3 lakh Cr. in FY24, up from ₹13.2 lakh Cr. in FY23 driven by increased user and merchant engagement. [11]

Financial Services

Financial Services and Others include the revenues Paytm generates from its financial services partners and consumers of its offerings, primarily loan distribution. Financial Institutions use Paytm to enter into bilateral agreement with customers and Paytm does not lend from its balance sheet.

Revenue is earned by way of sourcing fee which is typically between 2.5% and 3.5% of loan value and a collection fee of 0.5%-1.5% of current disbursement value.[15]

Paytm is also focusing on insurance and equity brokerage business.[13]

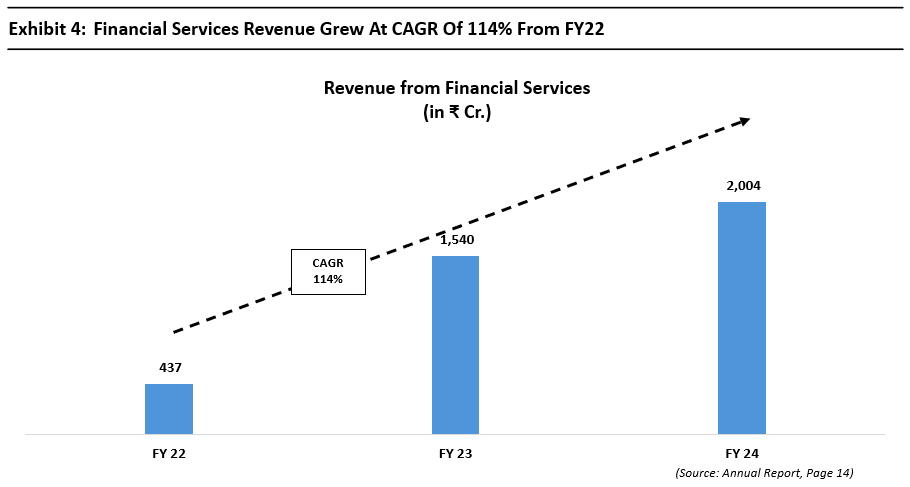

Revenue from financial services grew at 30% to ₹2,004 Cr. in FY24 from ₹1,540 Cr. in FY23, primarily driven by 48% YoY growth in the value of loans processed in FY24. The loan portfolio stands ₹52,390 Cr., from ₹35,378 Cr. in FY23.

Paytm’s Financial Service Facilitators[14]

1. Paytm Postpaid:

• Paytm Postpaid is a Buy Now, Pay Later facility offered by Paytm’s NBFC partners. With Postpaid, users get credit of up to ₹60,000 every month at 0% interest for up to 30 days.

• Average monthly bill size is ₹7,000 as on Sep’23 quarter. Lender partners charge a convenience fee of 0% to 3% on monthly spends made using Paytm Postpaid, depending on the risk policy, customer profile, payment behavior.

• Separately, some of the merchants pay MDR for payments made through Postpaid and on late payments, consumers pay late fees. This product provides good insight into consumers’ ability to take credit and repay on time and hence acts as a good funnel for personal loans and credit cards.

2. Personal Loans:

• Paytm, through its lending partners, offers up to ₹3 lakh in personal loans to its customers. Typically, loans are less than 2 years. The average ticket size of these loans for the Q2FY25 quarter was ₹165,000 with an average tenure of 16 months.

• Over 35% of personal loans disbursed come from existing Paytm Postpaid users.

3. Merchant/Business Loans:

• Paytm, through its lending partners, offers working capital loans to merchants who are using Paytm for accepting digital payments.

• 85% of merchant loans are given to customers who also use Paytm devices (such as Soundbox, Card Machines). Device owning merchants tend to have higher engagement for digital payments resulting in higher payment volumes. This provides insight into their cash collections and their ability to repay the loans.

• Additionally, these loans are offered to merchants with high vintage and stable transaction histories, providing comfort regarding the collectability of the loans.

Other financial services

Insurance Distribution: Paytm emphasizes product innovation for streamlined distribution and improved claims experiences, especially in health insurance. It is operated through a subsidiary, Paytm Insurance Broking Private Ltd. and reported revenue of ₹32.33 Cr. in FY24 with a PAT of ₹8.34 Cr.

Equity Broking and Mutual Fund Distribution: The company continued to scale its broking and mutual fund distribution, leveraging SIPs and other wealth management solutions.

Marketing Services

Paytm helps merchant partners grow their businesses by leveraging its consumer traffic, offering marketing services like selling tickets, deals, and gift vouchers. The company also provides advertising, loyalty services, and distributes co-branded credit cards with SBI Card, HDFC Bank, and Kotak Bank. As of FY24, Paytm had 12 Lakh activated co-branded credit cards. Paytm earns upfront revenue from card activation and receives a portion of the interchange fee for the lifetime of the card.

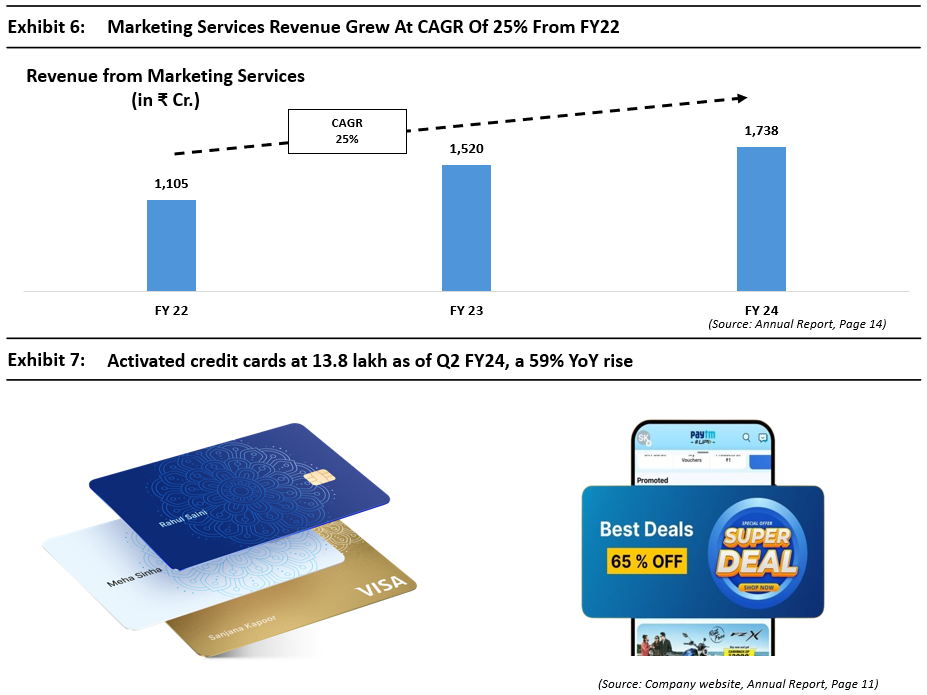

Revenue from Marketing Services (previously known as commerce and cloud services) grew 14.34% to ₹1,738 Cr. in FY24 from ₹1,520 Cr. in FY23. Paytm’s revenue streams include transaction fees charged to merchants and convenience fees to customers, typically a percentage of the transaction value for services such as travel, entertainment, and deals. Additionally, Paytm generates revenue through subscription and volume-based fees for its cloud and software solutions provided to merchants. Advertising partners contribute to revenue based on the scale and type of campaigns.[12]

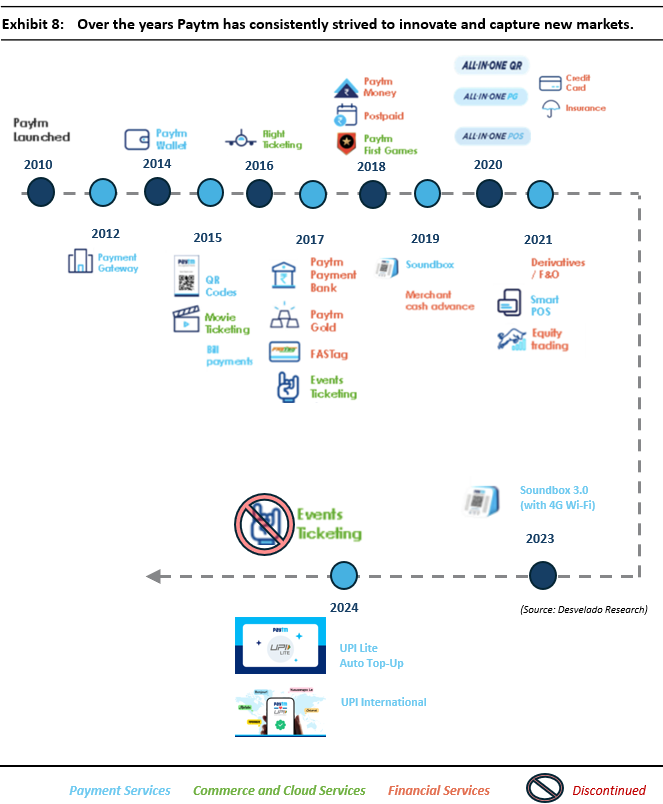

Paytm’s Journey Through the Years