Global Fintech Environment [39]

The payments segment dominates fintech investment globally, attracting over ₹1.76 Lakh Cr. in H1’24. Within the payments space, there was growing interest in use-case-driven payments companies, such as payments insurance, unsecured lending, and insurance claims.

AI remains a major priority for fintech investors.

Following broader investment trends, AI continued to be an area of interest to fintech investors, particularly in the US.

Trends to watch for in FY24

Larger focus on Central Bank Digital Currencies (CBDC) and regulated stablecoins. Increasing interest in middle and front-office solutions related to investment management. Growing investor focus on AI-powered fintech offerings in emerging areas like behavioral intelligence. Increasing investor attention on less traditional fintech markets, including Africa and parts of Southeast Asia—such as Indonesia and the Philippines. ESG fintechs continue to gain attention, particularly in areas like carbon measurement and tracking.

Global Scenario For Digital Payments[16]

The global digital payment market was valued at ₹8.082 Lakh Cr. (in Revenue) in 2023 and is forecasted to grow at a CAGR of 21.1% from 2024 to 2030. By the end of 2021, over two-thirds of adults globally were engaged in digital payments, with this number set to increase. Key growth drivers include:

• Widespread smartphone adoption and improved internet accessibility.

• The rapid shift towards cashless transactions driven by the pandemic.

• Government incentives encouraging the use of digital payment systems.

Innovative payment solutions like cryptocurrency, Buy Now Pay Later (BNPL), Open Banking, and Embedded Finance are transforming how transactions are made globally.

As of December 2023, 530 Cr. people (or 65.7% of the global population) were internet users, with 84% of mobile devices in use being smartphones, driving the digital payments surge.

Point of Sale (POS) segment was the largest revenue contributor in 2023, benefiting from faster checkouts and multiple payment options in retail. It had contributed ₹1.784 Lakh Cr. In the previous year.

Payment Gateway segment is expected to show the fastest growth between 2024 and 2030, with in-store retail increasingly using gateways for smartphone-based payments.

While the market has significant growth potential, fraudulent activities remain a critical challenge. Global payment frauds could cost ₹3.41 Lakh Cr. by 2027E, underscoring the need for enhanced security measures and fraud prevention strategies.

Leading global market players include PayPal, Global Payments Inc., ACI Worldwide, and Mastercard.

Macroeconomic Overview

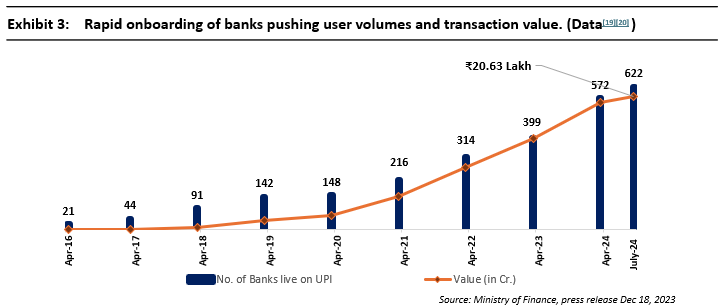

Currently the backbone of India’s digital payments ecosystem is formed by UPI (Unified Payments Interface) which has significantly boosted the adoption of cashless transactions.

UPI is a system that integrates multiple bank accounts into a single mobile app, offering seamless fund routing, merchant payments, and banking features. It also facilitates peer-to-peer (P2P) payment requests, which can be scheduled and paid as needed. [21]

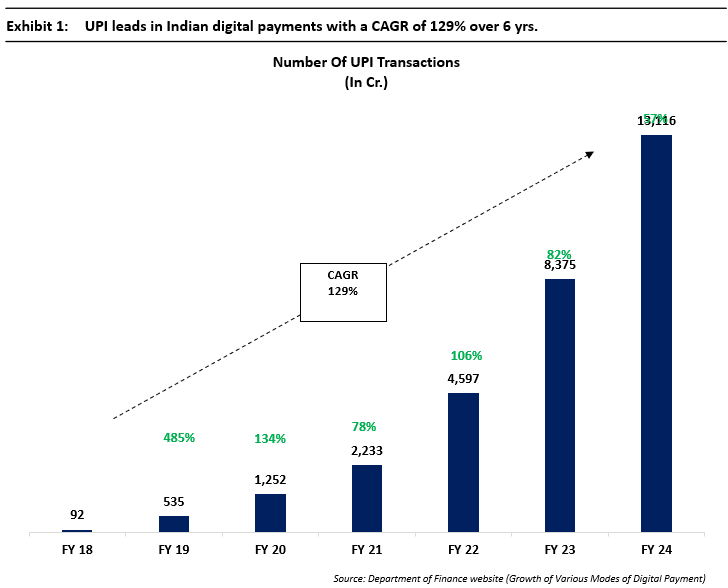

User traffic resulting from UPI Payments[17]

UPI transactions have grown from 92 Cr. in FY18 to 13,116 Cr. in FY24 at a CAGR of 129%. Around 46% of the global real-time payment transactions are happening in India. UPI accounted for 70% of digital payment transactions in FY24. In May 2024, UPI recorded over 1,403 Cr. transactions in a single month for the first time.

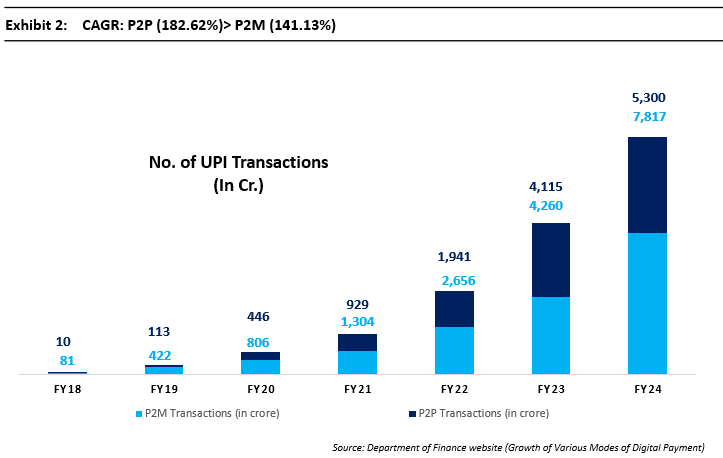

Bifurcation of UPI Transaction[17]

• P2P (Person-to-Person):

Transactions involve a transfer of funds between two individual users or individual accounts through UPI. P2P transactions also show a considerable jump between FY22 and FY24, growing from 1,940.60 Cr. to 5,299.60 Cr. P2P transactions grew at a CAGR of 182.62% from FY18 to FY24.

• P2M (Person-to-Merchant):

Transactions involve payments through UPI made from an individual to merchants or service providers. A notable jump in P2M transactions occurs between FY22 and FY24, from 2,656.20 Cr. to 7,817 Cr. P2M Transactions grew at a CAGR of 141.13% over the same period.

Both categories exhibit a clear upward trend from FY18 to FY24 and indicate an exceptionally rapid increase in each type of UPI transaction with P2P transactions growing at a significantly faster rate.

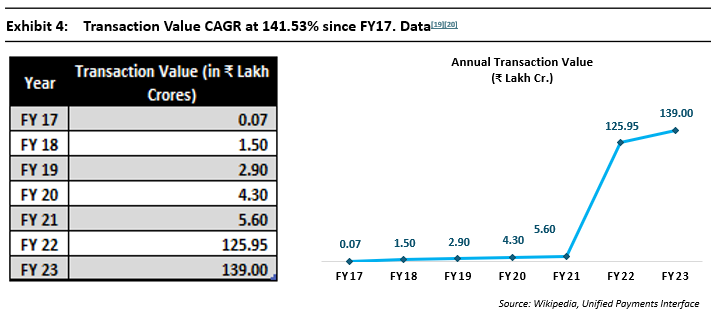

Total Transaction Value of UPI and shifting preferences

Total UPI transaction value in July 2024 reached ₹20.64 lakh Cr. The average daily transaction value in July 2024 was ₹4.66 lakh Cr. Transaction value in July 2024 increased by 2.84% compared to June. In the first four months of FY25, transactions amounted to ₹80.79 lakh Cr. Debit card transactions declined by 43% year-on-year in FY24 suggesting a notable shift in the mode of payment preferred by people.[18]

Internationalization of UPI

At present UPI is fully functional and lives in UAE, France, Bhutan, Sri Lanka, Nepal, Singapore, and Mauritius.

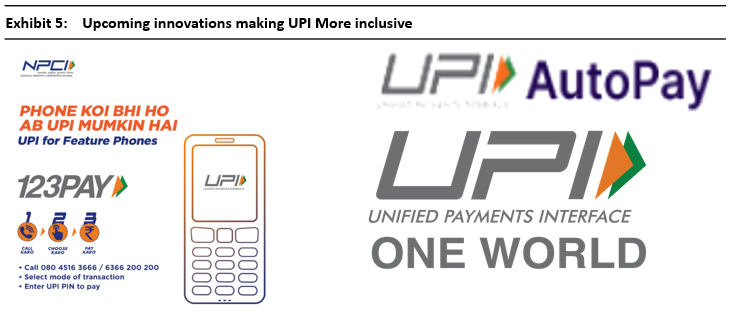

Upcoming Innovations in UPI expected to increase the reach of market layers[30]:

UPI 123Pay – Offline Payments

UPI 123Pay is intended to cater to feature phone users. The RBI’s UPI 2.0 extension brought forth a solution independent of phone type or internet connectivity. 123Pay allows feature phone users to engage in digital transactions through multiple approaches, including Interactive Voice Response (IVR), a feature phone-based apps, missed calls, or proximity sound payment methods. It has also been made accessible in regional languages to increased its user base.

UPI AUTOPAY – Recurring Payments

UPI Autopay allows the authorization and management of pre-approved debits from users’ bank accounts. Users can set up one-time authentication for automatic payments, sparing them from further involvement in the payment process. It offers various use cases, including utility bills, online subscriptions, loan EMIs, insurance premiums, etc.

UPI One World – Empowering Foreign Travelers

UPI One World, offers accessibility for foreign travelers in India, enabling payments across all merchant outlets accepting QR-based UPI payments. These wallets will be accessible at select Indian airports, with further plans to extend this feature to incoming nationals visiting India.

Sector Overview

The Current State

The FinTech Industry in India is currently revolutionizing India’s financial landscape due to widespread internet access (82 Cr. active users)[26], governmental digitalization initiatives (13 initiatives with a total outlay of ₹14,903 Cr. in 2023)[27], and the increasing use of smartphones (65.9 Cr. users in 2022)[28].

FinTech startups in India are introducing innovative solutions that challenge traditional banking and financial services. The number of registered fintech startups in India has grown by approximately five times in the past three years, from 2,100 in 2021 to 10,200 in 2024.[29]

Global Leadership

India ranks third globally in terms of the number of fintech unicorns, trailing only the United States and China. India is home to 26 fintech unicorns with a combined market value of ₹7.57 Lakh Cr.[29]

The most significant disruptions are in digital payments, insurance, and financial services. Additionally, P2P lending platforms are democratizing lending, providing individuals and small businesses with access to funds without the need for traditional financial institutions.[25]

The Fintech sector in India has witnessed funding accounting for a 14% share of Global Funding. India ranks #2 on deal volume. The Fintech Market Opportunity is estimated to be ₹176.68 Lakh Cr. by 2030. Indian fintechs were the 2nd most funded start-up sector in India in 2022.[40]

The Fintech revolution has been characterized by the use of new technologies such as AI and Machine Learning, increased computing power, and the use of APIs that leverage Big Data in providing financial services.

At highest adoption rate of 87%, the sector is suitably positioned for further expansion, with tier II and III cities emerging as new hubs. The leading states for Fintech in India are Karnataka, Maharashtra, and Tamil Nadu, with Karnataka being at the forefront, anticipated to form 50% of India’s contribution to the sector by 2030 and to have 50 Fintech Unicorns by 2030.[39]

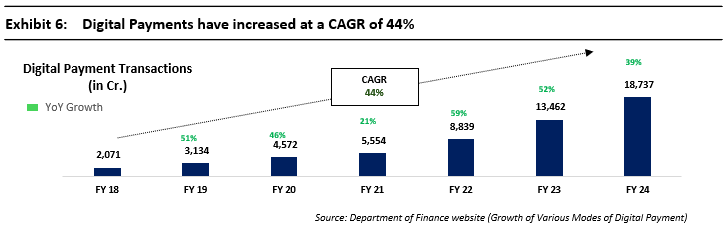

All Digital Payments (including UPI): Potent traffic generators for Fintechs

Digital Payments significantly increased in recent years with total payment transactions volume increasing from 2,071 Cr. in FY18 to 18,737 Cr. in FY24 at a CAGR of 44%. Digital Payments include modes such as NACH, IMPS, UPI, AePS, NETC, Debit Card, Credit Card, NEFT, RTGS, Prepaid Payment Instruments, Internet Banking, Mobile Banking, etc. (all intrabank transactions). [17]

Fintech Innovations

After 8 years of its launch UPI based payment methodologies such as QR codes, transfer to phone numbers, etc. along with an increasing number of banks signing up with the UPI platform there has been a proliferation of apps that have attracted consumer traffic as facilitators of UPI/digital transactions. They have used this consumer traffic to offer other services to customers such as insurance, investments (IPO, etc.), and BNPL on the individual customer side and enhanced their revenues by offering marketing services such as advertisements, credit/debit card collaborations, and other marketing campaigns on the B2C side.

These apps also act as payment gateways in India thus increasing digital transactions and acting as facilitators of Platform As Service (PaaS) companies such as Zomato, Swiggy, BookMyShow, and others that have the option for online payments.

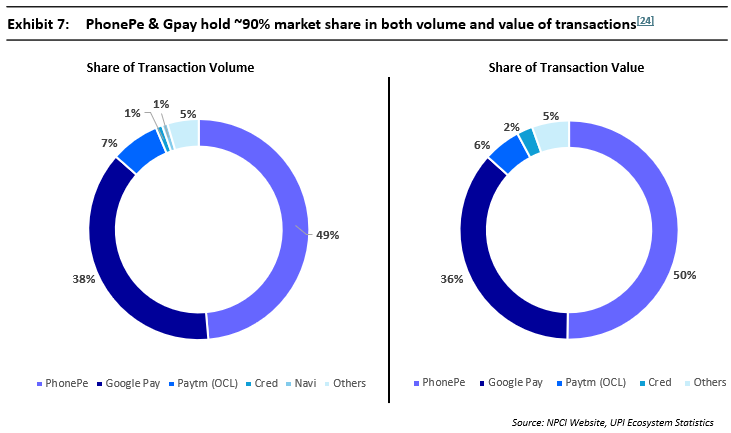

Notable Fintechs using the UPI payment Platform ecosystem.

The most notable companies in the sector are:

1.PhonePe

2.Google Pay (Gpay)

3.Paytm

4.CRED

5. Others include: Axis Bank Apps, Amazon Pay, Navi, ICICI Bank, WhatsApp Pay, Grow, Slice, MobiKwik, and Flipkart UPI.