Written By: Rhythm Garg

Now that we’ve explored our first phase of Advance options trading strategies, it’s time to delve deeper into second phase of advance option trading strategies that are more complex. These advanced techniques are widely used among option traders and can significantly enhance your potential returns and risk management. These strategies require a more sophisticated understanding of options mechanics and market dynamics.

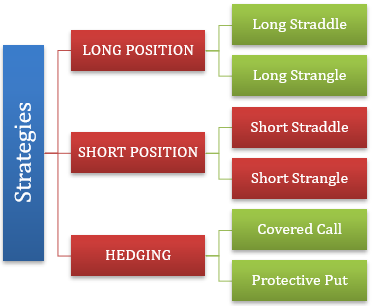

1. Long Position (Straddle & Strangle)- This position means you are strong Bullish or Bearish on the market and will reap returns if the market goes up or down but will at loss if market remains the same due to a concept called theta decay or time decay.

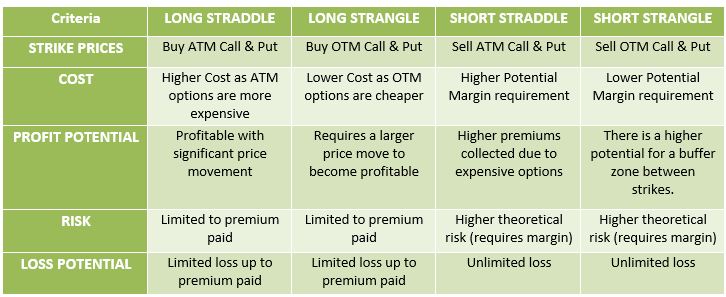

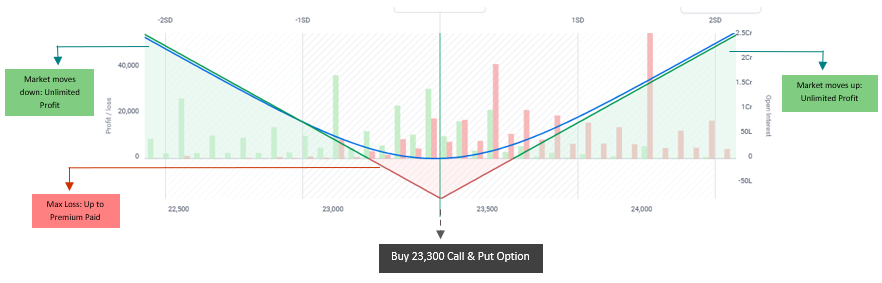

i. Long Straddle: A long straddle is an options strategy where a trader buys both a call and a put option on the same underlying asset with the same strike price and expiration date. This strategy is used when the trader expects a significant price movement in the underlying asset but is unsure of the direction.

Example 1, Imagine it’s a week before a major policy announcement by the Reserve Bank of India (RBI). You believe this announcement will cause significant volatility in the Nifty 50 index, but you’re unsure whether the market will react positively or negatively. Nifty 50 is currently trading at 23,300 and you implement the following options-

– Buy a Call Option: Purchase a call option with a strike price of 23,300. This gives you the right to buy the Nifty 50 at 23,300 with a premium of ₹ 200.

– Buy a Put Option: Buy a Put option with a same strike price of 23,300. This gives you the right to buy the Nifty 50 at 23,300 with a premium of ₹ 200.

– Net Premium Received: ₹ 200 (from buying the call) + ₹200 (from buying the put) = ₹ 400

Scenario 1: Positive Market Reaction

– The RBI announcement is perceived as positive, and the Nifty rallies to 23,700.

– Your call option is now in-the-money, with an intrinsic value of ₹500 (23,700 – 23,300).

– Your put option expires worthless.

– Profit: ₹500 (call value) – ₹400 (premium paid) = ₹100

Scenario 2: Negative Market Reaction

– The RBI announcement is perceived as negative, and the Nifty falls to22,800.

– Your put option is now in-the-money, with an intrinsic value of ₹500 (23,300 – 22,800).

– Your call option expires worthless.

– Profit: ₹500 (put value) – ₹400 (premium paid) = ₹100

Scenario 3: Minimal Market Reaction

– The RBI announcement has little impact, and the Nifty remains around 23,300.

– Both your call and put options expire worthless.

– Maximum Loss: ₹400 (premium paid)

In the above strategy If the Nifty moves significantly in either direction, your profit potential is unlimited. But if Nifty remains the same then the Maximum loss in this strategy will be the premium paid.

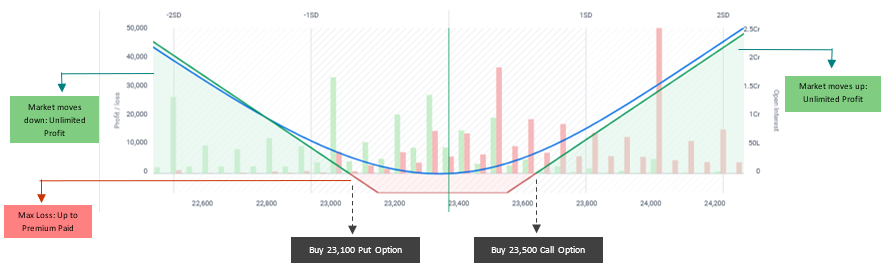

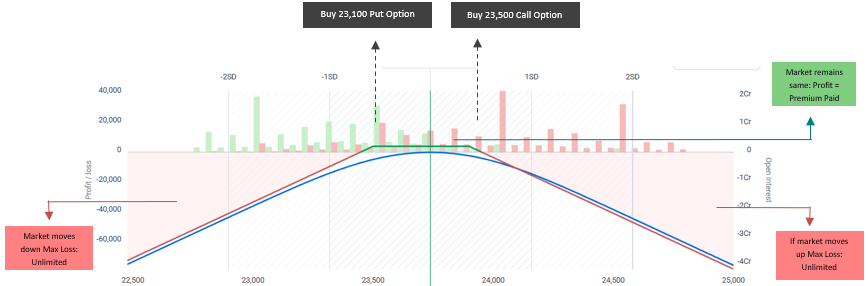

ii. Long Strangle: A long strangle is an options strategy where a trader buys both a call and a put option on the same underlying asset and same expiration date but with the different strike prices. This strategy is used when the trader does not expect a significant price movement in the underlying asset but within a range-based momentum. Think of it like a long straddle, but with a wider range of potential profit.

Example 1, Imagine it’s a week before a major policy announcement by the Reserve Bank of India (RBI). You believe this announcement will cause significant volatility in the Nifty 50 index, but you’re unsure whether the market will react positively or negatively. Nifty 50 is currently trading at 23,300 and you implement the following options-

– Buy a Call Option: Purchase a call option with a strike price of 23,500 (Out-of-the-money). This gives you the right to buy the Nifty 50 at 23,500 with a premium of ₹150.

– Buy a Put Option: Buy a Put option with a same strike price of 23,100 (Out-of-the-money). This gives you the right to buy the Nifty 50 at 23,100 with a premium of ₹100.

– Net Premium Received: ₹150 (from buying the call) + ₹100 (from buying the put) = ₹250

Scenario 1: Nifty Rises Significantly

– The RBI announcement is perceived as positive, and the Nifty rallies to 23,800.

– Your call option is now in-the-money, with an intrinsic value of ₹ 300 (23,800 – 23,500).

– Your put option expires worthless.

– Profit: ₹300 (call value) – ₹250 (premium paid) = ₹50

Scenario 2: Nifty Falls Significantly

– The RBI announcement is perceived as negative, and the Nifty falls to22,800.

– Your put option is now in-the-money, with an intrinsic value of ₹300 (23,100 – 22,800).

– Your call option expires worthless.

– Profit: ₹300 (put value) – ₹250 (premium paid) = ₹50

Scenario 3: Nifty Stays Range- Bound

– The RBI announcement has little impact, and the Nifty remains around 23,300.

– Both your call and put options expire worthless.

– Maximum Loss: ₹250 (premium paid)

In the above strategy If the Nifty moves significantly in either direction, your profit potential is unlimited. But if Nifty remains the same then the Maximum loss in this strategy will be the premium paid.

2. Short Position (Straddle & Strangle)- This position means you are can be Bullish or Bearish or looking for range bound market and will reap returns if the market goes up, down or if market remains the same due to a concept called theta decay or time decay. Both short straddles and short strangles are high-risk options strategies that are suitable for experienced traders who expect low volatility and are comfortable with the risk of potentially unlimited losses. We can say it’s a win-win strategy for option traders who are shorting the market.

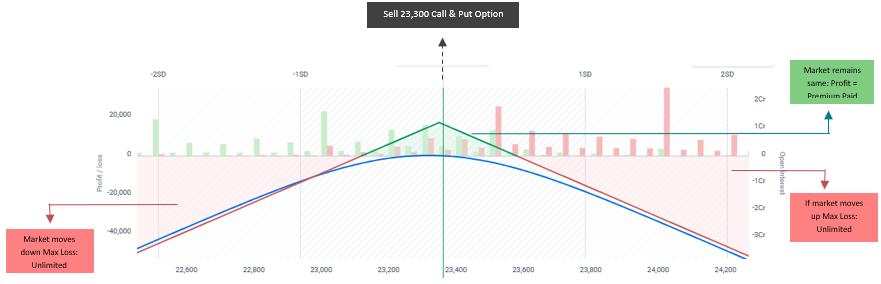

iii. Short Straddle: A short straddle is an options strategy where a trader sells both a call and a put option on the same underlying asset with the same strike price and expiration date. This strategy is used when the trader expects the price of the underlying asset to remain relatively stable.

Example 1, Let’s say the Nifty 50 is currently trading at 23,300. You believe it will stay within a tight range until the option expiration date.

– Sell a Call Option: Sell a call option with a strike price of 23,300 (at-the-money). This gives you the obligation to sell Nifty 50 at 23,300 with a premium of ₹ 200.

– Sell a Put Option: Sell a Put option with a same strike price of 23,300 (at-the-money This gives you the obligation to sell Nifty 50 at 23,300 with a premium of ₹ 150.

– Net Premium Received: ₹ 200 (from selling the call) + ₹150 (from selling the put) = ₹ 350

Scenario 1: Nifty Stays Close to 23,300 on expiration date

– The Nifty remains within a narrow range around 23,300.

– Both options expire worthless

– Profit: ₹350 (you keep the entire premium)

Scenario 2: Nifty Rises Significantly

– Nifty rises above 23,300.

– The call option buyer exercises their right, and you are obligated to sell the Nifty at 23,300, even though it’s trading at a higher price.

– Your put option expires worthless.

– Loss: Potentially unlimited, depending on how high the Nifty rises.

Scenario 3: Nifty Falls Significantly

– Nifty falls below 23,300.

– The put option buyer exercises their right, and you are obligated to buy the Nifty at 23,300, even though it’s trading at a lower price.

– Your call option expires worthless.

– Loss: Potentially unlimited, depending on how high the Nifty falls.

In the above strategy If the Nifty does not move significantly in either direction, your profit potential is limited to the premium received. But if Nifty moves significantly in either direction then the Maximum loss in this strategy will be unlimited (theoretically) as premium can be increased to any amount. But the above strategy can be said as slightly safer than “Long strategies” because of time decay which means as option reaches close it its expiry, it will start to lose value which it previously had in the beginning of the beginning of the contract.

iv. Short Strangle: A short strangle is an options strategy where a trader sells both a call and a put option on the same underlying asset and same expiration date but with the different strike prices. This strategy is used when the trader does not expect a significant price movement in the underlying asset but within a range-based momentum. Think of it like a long straddle, but with a wider range of potential profit.

Example 1, Let’s say the Nifty 50 is currently trading at 23,300. You believe it will stay within a tight range until the option expiration date.

– Sell a Call Option: Sell a call option with a strike price of 23,500 (Out-of-the-money). This gives you the obligation to sell Nifty 50 at 23,500 with a premium of ₹ 150.

– Sell a Put Option: Sell a Put option with a same strike price of 23,100 (Out-of-the-money). This gives you the obligation to sell Nifty 50 at 23,100 with a premium of ₹ 100.

– Net Premium Received: ₹150 (from selling the call) + ₹100 (from selling the put) = ₹250

Scenario 1: Nifty Rises Significantly

– Nifty rises and rallies to 23,600.

– The call option buyer exercises their right. You are obligated to sell the Nifty at 23,600, even though it’s trading higher.

– Your put option expires worthless.

– Loss: Potentially significant, depending on how high the Nifty rises. In this example, at 23,600, the loss would be ₹300 per Nifty unit (23,600 – 23,300 = 300) * contract size – ₹250 (premium received) = ₹50

Scenario 2: Nifty Falls Significantly

– If Nifty falls to 23,000.

– The put option buyer exercises their right. You are obligated to buy the Nifty at 23,000, even though it’s trading lower.

– Your call option expires worthless.

– Loss: Potentially significant, depending on how high the Nifty falls. In this example, at 23,000, the loss would be ₹300 per Nifty unit (23,300 – 23,000 = 300) * contract size – ₹250 (premium received) = ₹50

Scenario 3: Nifty Stays Range- Bound

– The Nifty stays between 23,500 and 23,100 until expiration.

– Both your call and put options expire worthless.

– Maximum Profit: ₹250 (premium paid)

In the above strategy If the Nifty does not move significantly in either direction, your profit potential is limited to the premium received. But if Nifty moves significantly in either direction then the Maximum loss in this strategy will be unlimited (theoretically) as premium can be increased to any amount.

3. Hedging Strategies- Hedging with options is a risk management strategy that involves using options to offset potential losses in your investment portfolio which include strategies like covered call, protective put, collar etc.

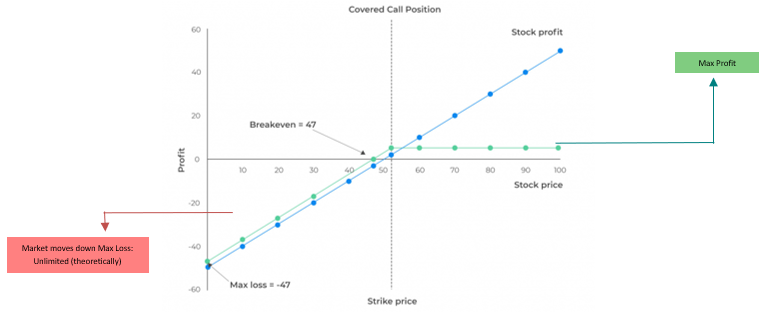

v. Covered Call: In this strategy you sell a call option on an asset you already own and get Long on Cash Market. A call option gives the buyer the right to buy the asset from you at a specific price (the strike price) by a certain date (the expiration date) while you have the obligation to sell.

Example 1, Imagine you own 100 shares of Reliance Industries, currently trading at ₹1,300 per share. You believe Reliance will either stay at its current price or rise moderately in the near future, but you don’t expect a huge surge.

– (Long Stock) Own the Stock: You already own 100 shares of Reliance Industries.

– (Short Call) Sell a Call Option: You sell one call option contract (representing 100 shares) with the following details (This “covers” your obligation to sell the shares if the option is exercised):

– Strike Price: ₹1,400 (Out-of-the-money)

– Premium Received: ₹50 per share (₹50 x 100 = ₹5,000 total).

– Expiration Date: Let’s say three months out.

Scenario 1: Reliance Stays Below ₹1,400

– The price of Reliance Industries stays below ₹1,400 until the option expiration date.

– The call option expires worthless

– Profit: You keep the ₹5,000 premium and your 100 shares of Reliance. This is the ideal scenario for a covered call.

Scenario 2: Reliance Rises At ₹1,400

– The price of Reliance Industries rises above ₹1,400 (e.g., to ₹1,500)

– The call option buyer exercises their right to buy your shares at ₹1,400.

– Profit: You sell your 100 shares at ₹1,400, making a profit of ₹100 per share (₹10,000 total) plus the ₹5,000 premium. Your total profit is ₹15,000. (If the Price rises significantly like say ₹1,500 then short call position will incur a loss as call option buyer will exercise their right to buy at a lower price than the current trading in market. Therefore, Total Profit in that case will be = ₹10,000 – ₹5,000 = ₹5,000.)

Scenario 3: Reliance Shares Falls ₹1,400

– The price of Reliance Industries falls (e.g., to ₹1,250).

– The call option expires worthless

– Loss: You still own your 100 shares, but they are now worth less so you sell the shares at a loss of ₹15,000 ((₹1400 – ₹1,250) x 100). However, the ₹5,000 premium you received helps to offset some of this loss. So, you are at a Net Loss of ₹10,000 (₹15,000 – ₹5,000).

A covered call is a strategy to generate income and slightly reduce downside risk on a stock you already own, but it limits your potential profit if the stock price rises significantly. From the payoff chart we can see that the net position of a covered call strategy looks like ‘short put’ with a strike of 1400. This is because the Covered call restricts the ‘upside’ or gains from the position while leaving a scope for unlimited losses. Hence, the covered call is called a ‘synthetic short put’ position.

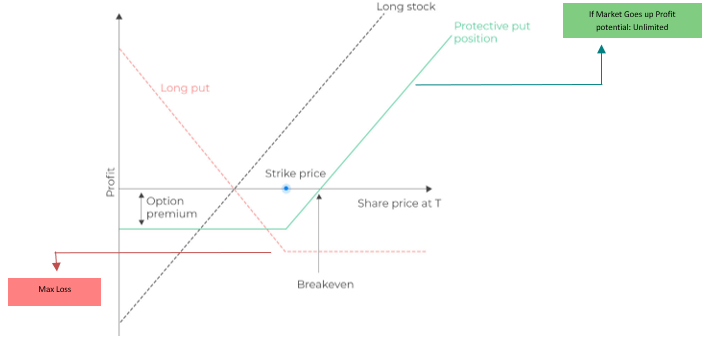

vi. Protective Put: In this strategy you buy a put option on an asset you already own and get Long on Cash Market. A put option gives you the right to buy the asset from you at a specific price (the strike price) by a certain date (the expiration date) while the seller has the obligation to sell. This acts like an insurance policy for your stock.

Example 1, Imagine you own 100 shares of Infosys, currently trading at ₹1,900 per share. You’re optimistic about Infosys’ long-term prospects but concerned about potential market volatility or a correction in the IT sector.

– (Long Stock) Own the Stock: You already own 100 shares of Infosys.

– (Long Put) Buy a Put Option: You buy one put option contract (representing 100 shares) with the following details: (You’re “protecting” your long position in Infosys by buying a put option. The put option acts as a safety net if the stock price declines)

– Strike Price: ₹1,900 (At-the-money or slightly out-of-the-money)

– Premium Paid: ₹40 per share (₹40 x 100 =₹4,000 total premium)

– Expiration Date: Let’s say three months out.

Scenario 1: Infosys Price Rises

– Infosys’ price rises to ₹2,000 or higher.

– Your put option expires worthless (you lose the ₹4,000 premium).

– Net Result: You gain on your Infosys shares which is ₹10,000 (₹100 x 100), offsetting the put option cost which is ₹4,000 (Put option Premium), Total Net Profit = ₹6,000 (₹10,000- ₹4,000)

Scenario 2: Infosys Price Stays the Same

– Infosys’ price remains around ₹1,900.

– Your put option also expires worthless.

– Net Loss: You lose the ₹4,000 premium.

Scenario 3: Infosys Price Falls

– Infosys’ price falls to ₹1,800.

– Your put option becomes valuable. You can exercise it and sell your 100 Infosys shares at ₹1,900, even though they’re worth ₹1,800 in the market.

– Net Result: You limit your loss. Your Put Option Premium has increased to ₹160 which resulted in gain of ₹120 (Net Premium gain ₹120 x 100 = ₹12,000), but you incur a loss on your stock which is worth less in the cash market so by offsetting the loss of ₹10,000 in cash market, you are remained with the Net Profit of ₹2,000 (₹12,000 – ₹10,000).

A protective put is a hedging strategy that allows you to participate in potential stock price gains while limiting your losses if the price falls. It’s like buying insurance for your stock portfolio. For all falls in the market, the long put will be profitable, and the long stock position will be loss-making, thereby reducing the overall losses only to the extent of premium paid. A protective put payoff is similar to that of a long call. This is because a protective put position offers the scope of unlimited gains with a limited loss, which is also the payoff profile of a long call position. Hence the protective put is called a ‘synthetic long call’ position.

A deep understanding of these strategies, including protective puts, covered calls, and straddles/strangles, empowers investors to proactively mitigate risk and navigate the complexities of the market. Therefore, understanding and effectively utilizing hedging strategies with options is crucial for investors seeking to navigate market volatility and safeguard their portfolios against unforeseen downturns. A thorough grasp of these techniques can lead to potentially enhanced returns, transforming market uncertainty from a threat into a calculated opportunity.