Overview of the Indian Banking Industry

The Indian banking industry is one of the largest in the world, comprising 12 Public Sector Banks (PSBs), 21 Private Sector Banks, 46 Foreign Banks, and 43 Regional Rural Banks (RRBs). With over 150,000 branches and more than 2,00,000 ATMs, it serves as the backbone of India's financial system. Public sector banks like BoB dominate the market but face increasing competition from private players and digital-first banks.

The Reserve Bank of India (RBI) is the primary regulatory authority, ensuring financial stability, enforcing prudential norms, and promoting financial inclusion. Key milestones include liberalization in the 1990s, the rollout of reforms like the Insolvency and Bankruptcy Code (IBC), and the push for digital banking post-2016.

Industry Structure and Market Size

As of FY24, total banking assets in India stood at ₹281 trillion, with Public Sector Banks (PSBs) accounting for over 60% of this. Credit growth surged to 15.4% YoY, reaching a base expansion of ₹1,70,000 crores, driven by retail and MSME lending. The deposit base expanded to ₹2,20,000 crores, growing at 9.4% YoY. PSBs, including Bank of Baroda (BoB), collectively hold a 70% market share in rural and semi-urban regions, owing to their extensive branch networks.

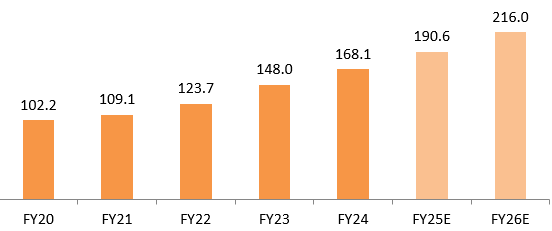

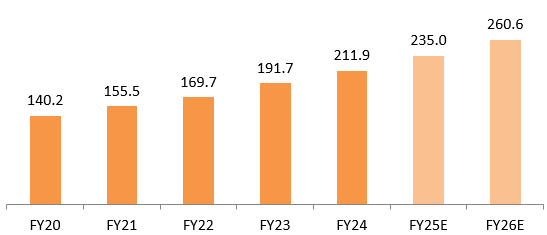

Advances are projected to increase from ₹102.19 lakh crore in FY20 to ₹216.04 lakh crore in FY26E. This growth is driven by factors such as increasing credit demand from various sectors, and especially government programs like PM VISHWAKARMA (Collateral free loans), and Pradhan Mantri Mudra Yojana priority sectors. The Indian banking industry is witnessing a steady growth in deposits as well. The deposits are expected to increase from ₹140.20 lakh crore in FY20 to ₹260.61 lakh crore in FY26E.

Exhibit: Advances base expected to grow at 13% YoY and reach ₹2.15 lakh Cr by FY26 (Data in Lakh Cr)

Source: Tijori Finance

Exhibit: A Deposit base expected to grow at 11% YoY, and reach ₹2.5 lakh Cr. by FY26 (Data in Lakh Cr.)

Source: Tijori Finance

Macroeconomic Environment and Key Drivers

India's economy is poised for growth, with a projected GDP expansion of 6.3% in FY24. The macro environment supports sustained credit demand, driven by industrial activity, a resurgence in private investment, and strong domestic consumption. With inflation moderating to 4.2% as of October 2024, the Reserve Bank of India (RBI) is likely to maintain a neutral monetary stance in the near term, keeping the repo rate stable at 6.5%.

This stability is expected to ease borrowing costs and foster greater financial activity. On the digital front, India continues to lead in payment innovation, with Unified Payments Interface (UPI) transactions surpassing a monthly volume of ₹15 trillion. The rapid adoption of digital banking solutions will likely fuel fintech partnerships and redefine customer engagement in traditional banking.

Potential headwinds include lingering impacts of high interest rates, which could suppress private capital expenditure in some sectors, and global economic uncertainty, particularly if advanced economies face a slowdown. Nonetheless, government-led infrastructure spending, favorable demographics, and reforms aimed at boosting ease of doing business should provide a cushion against external shocks.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.