NSE: FEDERALBNK

Balance Sheet

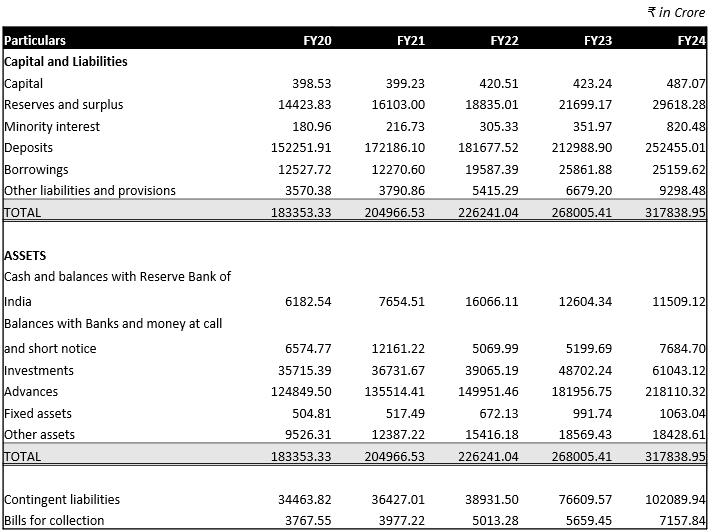

• FBL’s reserves and surplus grew at a strong CAGR of 15.5% over the last five years, driven mainly by consistently high operational profits. In FY24, reserves and surplus increased significantly by 36.5%, rising from ₹21,083 crore in FY23 to ₹28,607 crore. This growth was primarily due to FBL’s highest-ever annual net profit of ₹3,721 crore, a 24% increase compared to the previous year. Additionally, FBL boosted its share premium by issuing 230,477,634 equity shares through Qualified Institutional Placement (QIP) and 72,682,048 equity shares through a preferential allotment during FY24.

• FBL reported a significant 133% increase in minority interest during FY24, driven by two main factors. First, Federal Bank reduced its stake in Fedbank Financial Services Limited (FedFina) from 73.21% at the end of FY23 to 61.58% during the year. Second, FedFina issued additional shares, which contributed to the growth in minority interest. These issuances included 42,881,148 shares as part of the company’s Initial Public Offering (IPO) and 4,594,146 shares issued to employees exercising stock options.

• FBL achieved an impressive deposit growth of 18.35% during FY24, significantly surpassing the industry average of 13.47%. This growth can be attributed to FBL's successful expansion strategy, which included adding 141 new banking outlets in FY24. FBL also focused on attracting customers to increase deposits.

Additionally, the introduction of innovative products, like Stellar, played a crucial role. Stellar offered a "fit-for-all" proposition with bundled wellness benefits and other attractive features, which quickly gained popularity. Since its launch in February 2024, the product helped FBL acquire around 17,000 New-To-Bank (NTB) customers. Moreover, FBL introduced SHRENI, a product tailored for the Trust, Association, Society, and Club (TASC) segment. SHRENI targeted both current and savings account portfolios through institutional accounts. Retail deposits accounted for 94% of total deposits in FY24, reflecting FBL's strategic focus on this segment.

• FBL's advances grew at a CAGR of 11.63% over the past five years, reaching ₹2,18,110 crore in FY24. This growth was driven by strong performance across its business segments, with the retail credit book growing by 25% year-on-year and wholesale banking advances increasing by 15% year-on-year. Federal Bank’s investment in digital platforms, such as its mobile banking app and WhatsApp lending platform, likely improved its reach and loan origination capabilities. Additionally, partnerships with FinTech companies and other institutions have expanded its distribution channels and enabled access to new customer segments

• FBL’s contingent liabilities grew by 162.23% in two years, reaching 32.12% of its total assets in FY24, driven mostly on account of mainly due to liabilities from outstanding forward exchange contracts. A recent study shows that this trend is common among Indian banks, varying by business strategy and risk appetite. Public sector banks are cautious, with 41% exposure, while private banks, being more risk-oriented, show 110% exposure.

Profit & Loss Statement

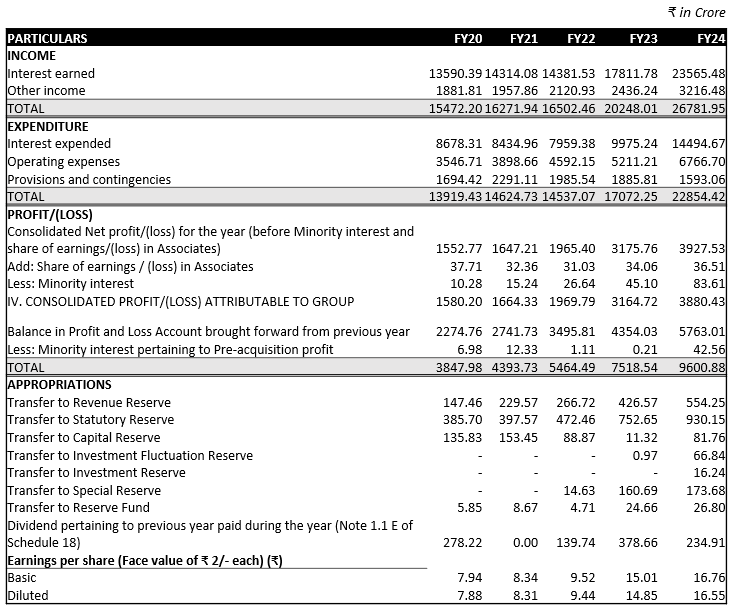

• In FY24 both interest income and other income increasing by 32.3%, net interest income surged by 15% year-on-year (YoY) to ₹8,293 Crore, driven by a 20% expansion in Net Advances, which reached ₹2,09,403 Crore. FBL’s Yield on Average Advances improved as well, rising to 9.35% in FY24 from 8.56% in the previous year.

• Non-Interest Income grew by substantial 32% YoY growth to ₹3,079 Crore, bolstered by a 19% increase in Fee Income, reflecting FBL's efforts to diversify revenue beyond interest income. Subsidiaries like Fedfina played a significant role, with Fedfina’s total revenue increasing by 34%, driven by a 22% growth in its loan book.

• FBL is looking forward to pivot toward the retail segment, which generally offers higher yields compared to wholesale banking. Retail advances grew by 25% YoY to ₹67,435 Crore, now accounting for 31% of total advances. Microfinance saw remarkable growth of 141%, while the share of high-yielding unsecured products, such as credit cards and personal loans, increased, boosting profitability and effectively managing credit risk.

• To support sustained growth, FBL has been expanding its geographical footprint, particularly in high-growth regions like Gujarat, Maharashtra and Karnataka . It is also focusing on digital lending and forming partnerships with FinTech companies to enhance customer acquisition and outreach. These initiatives are expected to further drive revenue growth and tap into new customer segments.

• FBL experienced a rise in expenses during FY24. Both interest expenses and operating expenses showed substantial increases. Interest expenses, surged by 45.31% year-on-year while the operating expenses, rose by 29.85%.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.