Current State of the Banking Industry: 5

In FY24 the Indian banking sector has showcased notable resilience despite global challenges like the Russia-Ukraine conflict. The Reserve Bank of India (RBI) maintaining the policy repo rate at 6.5%, aiming to control inflation and support economic growth. Even the economic environment saw several changes, such as the withdrawal of ₹2,000 notes, the merger of HDFC Ltd. with HDFC Bank, and the imposition of the incremental Cash Reserve Ratio (CRR), all of which influenced the banking sector's operations.

Source: IBEF industry report

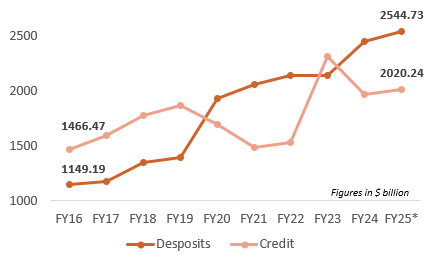

• As of July 2024, bank credit stood at ₹168.12 lakh crore (US$ 2,020 billion), while deposits reached ₹209.36 lakh crore (US$ 2,544.7 billion). Over the last decade, bank credit grew at a CAGR of 3.34%, and deposits at 9.23%, driven by rising incomes and robust savings.

• Credit growth across sectors remained strong, with Scheduled Commercial Banks (SCBs) disbursing ₹164.3 lakh crore, reflecting a 20.2% year-on-year increase in FY24. This was fueled by personal loans, housing credit, and agricultural lending.

• The asset quality of banks improved significantly, with the Gross Non-Performing Assets (GNPA) ratio dropping to 2.8% by March 2024, a 12-year low, from 11.2% in FY18. This improvement was due to better borrower selection, effective debt recovery, and stronger governance structures. The top 10 Indian banks maintained strong asset positions, with more than 50% of their assets in loans, making them resilient to rising interest rates

• Digital payments adoption has surged, with Unified Payments Interface (UPI) transactions crossing ₹15 lakh crore monthly. Additionally, the government's efforts under the Pradhan Mantri Jan Dhan Yojana (PMJDY) have expanded banking access, resulting in over 50 crore accounts by FY2024, further boosting deposit mobilization, particularly in rural and semi-urban areas

• The banking sector experienced growth in agriculture, housing, and industrial lending. The government and RBI focused on low-cost loans for MSMEs and stable credit to the services sector. Housing loans rose significantly from ₹19.9 lakh crore in March 2023 to ₹27.2 lakh crore in March 2024.

Exhibit 3: Deposits Poised for Strong Growth (9.23% CAGR) as Credit Expansion Slows (3.62% CAGR) in the Years Ahead (FY16-FY25E)

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.