NSE: BANKBARODA

BoB operates a diversified business model, combining retail and corporate banking with treasury, international banking, and digital services, aimed at delivering comprehensive financial solutions across domestic and global markets.

1. Retail Banking

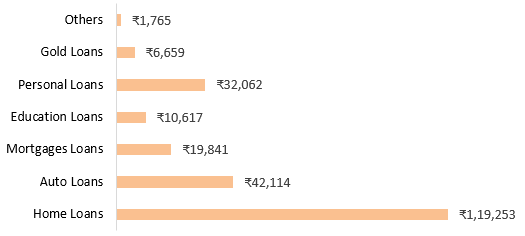

Retail Banking segment at BoB focuses on providing a wide range of financial products to individual customers, including personal loans, home loans, auto loans, education loans, savings and deposit accounts, and credit cards. The segment aims to increase customer outreach through digital channels and a vast branch network, catering to both urban and rural customers across India.

As of FY24, the retail advances portfolio accounted for about 23% of the bank’s total domestic advances, with retail loans totaling around ₹2.3 lakh crore. The segment achieved growth in home loans and personal loans, contributing significantly to the bank’s overall revenue, with retail interest income amounting to over ₹25,000 crore.

BoB has a large retail customer base of over 150 million, attributed by digital presence and product offerings on platforms like the BoB World app. Digital transactions through BoB World grew by around 60% year-over-year, reflecting the bank’s push towards digital banking and customer engagement.

Exhibit 1: Home Loans composed more than 50% of retail advances for 2 years(₹ Cr.)

2. Corporate/Wholesale Banking

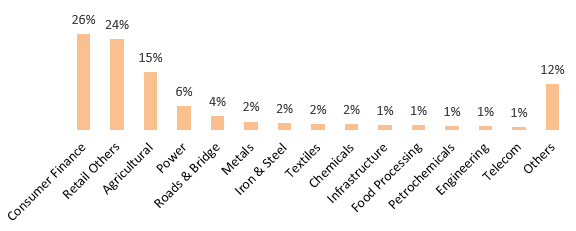

Corporate Banking segment of BoB provides financial solutions to large and mid-sized corporate clients, including lending, trade finance, cash management, and structured finance services. This segment focuses on key industries such as infrastructure, energy, real estate, and manufacturing, offering products like working capital loans, term loans, project financing, and treasury solutions tailored to corporate needs.

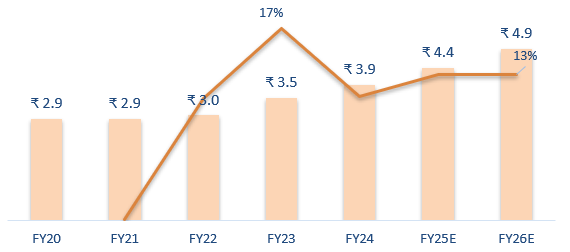

In FY24, the corporate advances segment constituted approximately 42% of BoB’s total loan portfolio, with corporate advances totaling around ₹3.4 lakh crore. The segment has maintained a steady growth rate, contributing over ₹25,500 crore in income.

BoB’s corporate banking segment has been actively managing asset quality, achieving a gross non-performing asset (NPA) ratio for corporate loans around 3.5%, showing improvement over previous years. The bank employs stringent credit appraisal, monitoring systems, and sector-specific risk assessments to maintain portfolio health and mitigate risks in its corporate lending activities.

Recently Bank has entered into an MOU with IREDA for collaboration (BoB Earth) in areas of Co-Lending for Renewable Energy Projects as well as Loan Syndication and Underwriting. Bank has an outstanding of ₹ 15,268 crore for financing renewable energy projects under Corporate Credit segment.

Exhibit 2: Power with maximum allocation of corporate advances: 6.27% share

Exhibit 3: Corporate advances expected to reach ₹4.9 lakh crore by FY26, with 13% YoY growth

3. Treasury Banking

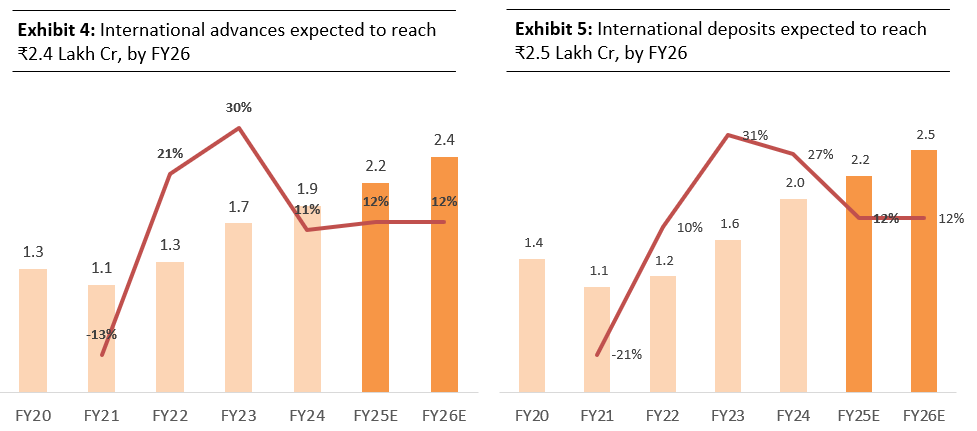

Treasury Banking segment at BoB manages the bank's liquidity, investment portfolios, and trading activities across domestic and international markets. The core functions include investments in government and corporate securities, foreign exchange trading, derivatives, and money market operations. The bank’s treasury department also handles asset-liability management (ALM), ensuring risk mitigation through effective hedging and regulatory compliance.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.