/

Research and Report by: Kartikey Chug

Desvelado India

Imagine a world where companies pretend to be something they're not, all to make money. Well, that's exactly what happened with Add-Shop E-Retail Limited and White Organics Agro Limited, and the truth has finally come to light.

Two companies, Add-Shop E-Retail Limited and White Organics Agro Limited, were caught in a web of deceit. They were accused of not being honest about how they do business and how well they are doing. This is a big problem because when companies lie, it can hurt the people who invest their money in them.

These companies tried to make themselves look better than they really were. It's like when someone wears a fancy costume to a party to impress others. Add-Shop E-Retail Limited and White Organics Agro Limited were pretending to be successful and well-run companies when, in reality, they were not doing things the right way.

Thankfully, there are rules in place to make sure companies play fair. The authorities, like the Securities and Exchange Board of India, found out about the companies' tricks. They noticed that something wasn't right with how these companies were behaving. Just like how a detective solves a mystery, the authorities investigated and uncovered the truth.

Lets Understand

Dummy Companies and inflating Sales (Case Study)

Dummy companies, often referred to as shell companies, are entities that exist only on paper with no significant operations, employees, or assets. Dummy companies can be used for a variety of purposes, including money laundering, tax evasion, fraud, and hiding the true ownership of assets. Goods or services are "sold" to the dummy companies at the end of a reporting period to artificially boost sales figures temporarily. These goods or services are often returned or the transactions are reversed after the reporting period ends.

Mechanism of Dummy companies to inflate numbers -

- Creation of Dummy companies - Companies set up multiple shell entities with minimal legal and operational footprints. These entities typically have basic documentation, such as registration papers, but lack actual business operations, employees, or tangible assets.

- Fictitious Sales Transactions - The primary company generates fake invoices for sales to these dummy companies. These sales are recorded in the primary company’s books as legitimate revenue.

- Circular transactions and round tripping - Money is moved between the primary company and its dummy companies in a circular manner. The primary company might record a sale to a dummy company, which then transfers the same money back to the primary company through a series of complex transactions.

- Channel Stuffing - Goods or services are "sold" to the dummy companies at the end of a reporting period to artificially boost sales figures temporarily. These goods or services are often returned, or the transactions are reversed after the reporting period ends.

- Complex Network of Transactions - Multiple dummy companies can be created to form a complex web, making it difficult for auditors and regulators to trace the transactions and uncover the fraud.

We will discuss the situation with example of Satyam Computers

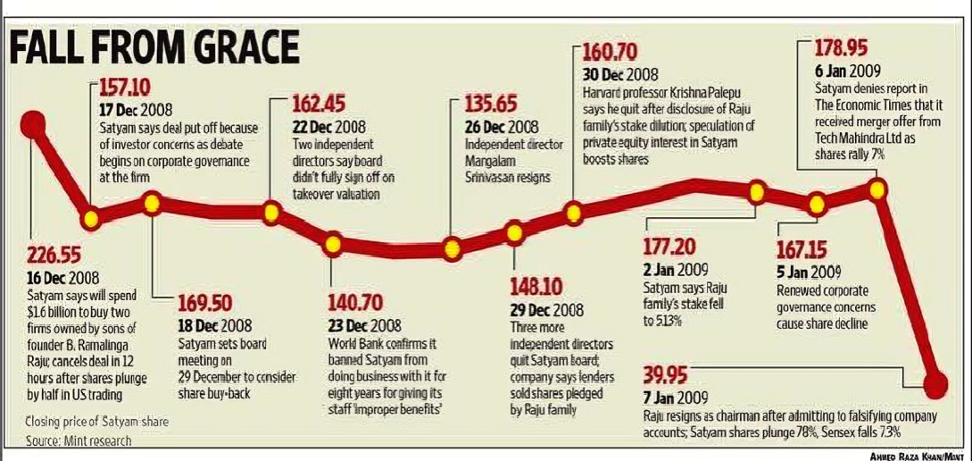

In the Satyam Computers scandal, the company's management executed a massive financial fraud by manipulating accounting records and creating fictitious revenue. They established a network of dummy companies and fabricated invoices for services that were never provided. The false transactions were recorded as sales, significantly inflating the company's revenue and profit figures. This deception allowed Satyam to present an image of rapid growth and strong financial health, attracting investors and boosting its stock price.

The fraud was meticulously concealed through complex financial maneuvers and document falsifications, making it challenging for auditors and regulators to detect. However, the deceit eventually unravelled in 2009 when the company’s chairman, Ramalinga Raju, confessed to the fraud, revealing the extent of the manipulation. The fallout was catastrophic, leading to a sharp decline in the company's market value, legal action against its executives, and a severe loss of investor trust.

The below timeline shows how the stock price of Satyam computers plunged 78% when the news of fraudulent activities came out.

Key metrices for assessment

What factors and metrics, an investor can see and analyse to avoid such situations and plan their entry or exit points.

- Inventory turnover ratio – Inventory turnover ratio is a vital metric used to assess how efficiently a company manages its inventory. It tells how many times a company can turn its inventory around in a year. With increasing sales but constant or decreasing turnover ratio, there can be an indication of violation or misrepresentation.

- Sales, Trade Receivables, Bad debts, and Debtor Ageing – Trade receivable represents the credit sales that the company did in the financial year. Bad debts represents the part of trade receivables that the company don’t expect to receive. Debtor ageing is a schedule that track the monetary value of their accounts receivable, so they know how much money is at risk of not being paid. An investor should monitor these numbers closely. If the company relies heavily on credit sales and its debtors are not paying, as reflected in the debtor schedule, it could indicate potential manipulation in the accounts.

- Purchase & Sales authenticity by Auditor – The auditor documents all findings and provides remarks based on the company's accounting policies in the audit report. They verify and authenticate whether purchase and sale orders have been properly executed. If the auditor identifies any irregularities, they include their observations in the report.

- Capex and Depreciation - Proper alignment ensures that long-term investments (CapEx) result in corresponding depreciation over time, reflecting accurate asset utilization. Significant discrepancies, such as high CapEx without corresponding depreciation increases, or vice versa, can signal improper capitalization practices or underinvestment in the business. This analysis helps ensure the company’s financial health and accounting integrity.

Add Shop E Retail Ltd. used Dada Organics as its dummy company who also tried to make merry by raising money via IPO on the back of its rising sales and filed a DRHP with exchanges; however, it could not succeed and withdrew the DRHP.

Related to the concepts, we have looked before, a complaint dated September 2023, against Add Shop E Retail Ltd and White Organics Ltd for alleging irregularities pertaining to related party transactions, fake announcements regarding supply orders etc., SEBI initiated an investigation for the period April 1, 2020, to March 31, 2023.

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.