NSE: MONTECARLO

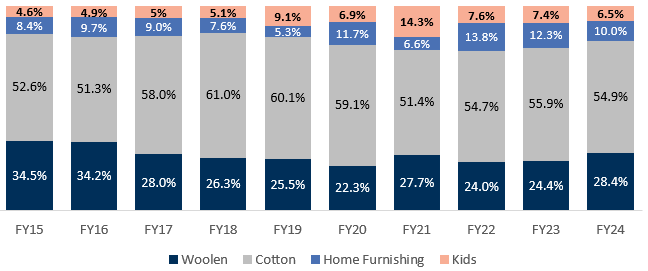

The strength of MCFL is the woollen portfolio under the Monte Carlo brand (28% of sales). Within its segment, this has more than 50% market share of the organized segment. Monte Carlo woollen sweaters command high gross margins and this segment is the main source of income for the company. The problem has been that the woollen business has been a dog in terms of growth (sub 17% growth). The woollen portfolio has penetrated the northern and eastern parts of the country and has a limited market in the warmer parts. It grows in the mid-single digits, at best.

• MCFL has been investing in growing its non-woolen portfolio, which is cotton apparel. Within cotton too, a fair share of the portfolio is tilted towards winter wear (jackets) but the same is suitable for relatively less harsh winter regions of the country. The share of cotton has grown steadily over the years and now makes up 55% of sales. Other growth drivers have been segments such as home furnishings and kids’ apparel, which together make up 16.5% of sales.

• Historically, woolen apparel has been made in-house with all the raw material sourced from the erstwhile parent and now group company, OWM. For cotton apparel, some of the job work is outsourced to another group company – Nahar Spinning Mills Ltd.

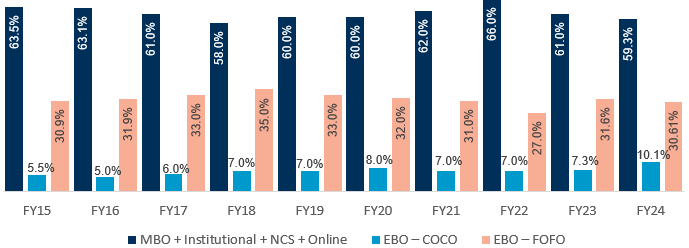

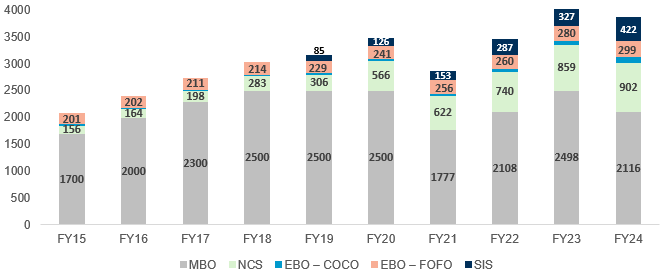

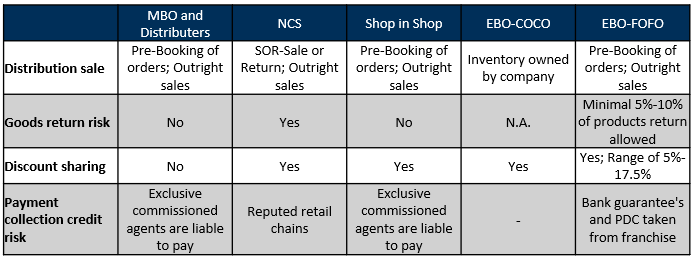

• In terms of distribution, MCFL has had an over-reliance on the multi-brand outlets (MBO) channel (50%+) in the past but that has been under some stress post demonization and introduction of goods and services tax (GST). The company has attempted to correct the same in the last few years with a larger focus on LFS (large format stores) and online channels. The latter come with lower margins, call for discount sharing, and buy on a consignment basis. At the same time, they are important given they attract an incrementally higher number of consumer footfalls. LFS and online, each contribute 10% of sales and are fast-growing.

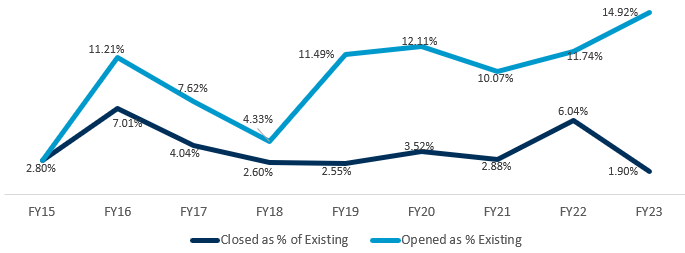

• MCFL also draws a fair share of 40% from the exclusive brand outlets (EBO) channel (400+ EBOs). EBO count has grown at 5% CAGR over the last seven years with EBO sales growing 10% i.e. 6% implied same-store sales growth (SSSG). 85% of the EBOs are franchised with a store closure rate of 13% (stores closed/stores opened). These metrics are not ideal, and the company should look to invest more in its EBOs as well. The store closure rate is on the higher side, too. However, on both these metrics, MCFL scores much better than KKCL. Also, please notice that the implied store SSSG of 6% is healthy and suggests potentially good store economics. The company’s own EBO count has increased 5x from 21 to 112 between FY18 and FY24. This is a move in the right direction.

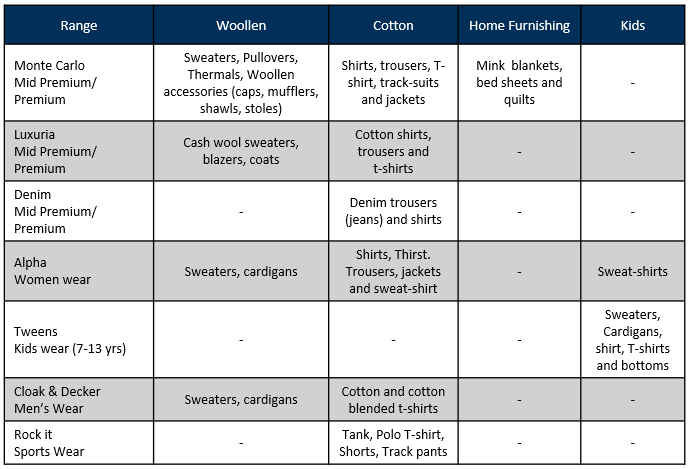

The company offers a diverse selection of products under the “Monte Carlo” brand:

- 'Luxuria' caters to the premium menswear segment.

- 'Denim' features a dedicated line of denim apparel.

- 'Alpha' represents the exclusive collection for womenswear.

- 'Tweens' offers a specialized range for kidswear.

- 'Cloak & Decker' serves as the budget-friendly option for menswear.

- 'Rock.it' provides high-end sports and fitness wear.

- 'Monte Carlo Home' offers a comprehensive range of home textile products.

Revenue Mix By Geography

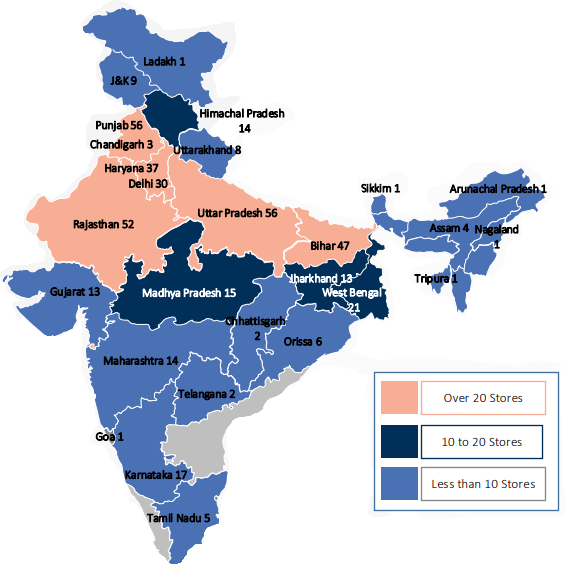

• NORTH – North India has been the major contributor to Monte Carlo’s revenues (53.3% in FY24). Revenue in this region has grown by 10.8% CAGR in the last 9 years. (FY15: 298.8 cr, FY24: 755.3 cr).

Comments

Log in to comment and join the discussion.

No comments yet. Be the first to comment.