Research By: Saizal Agarwal

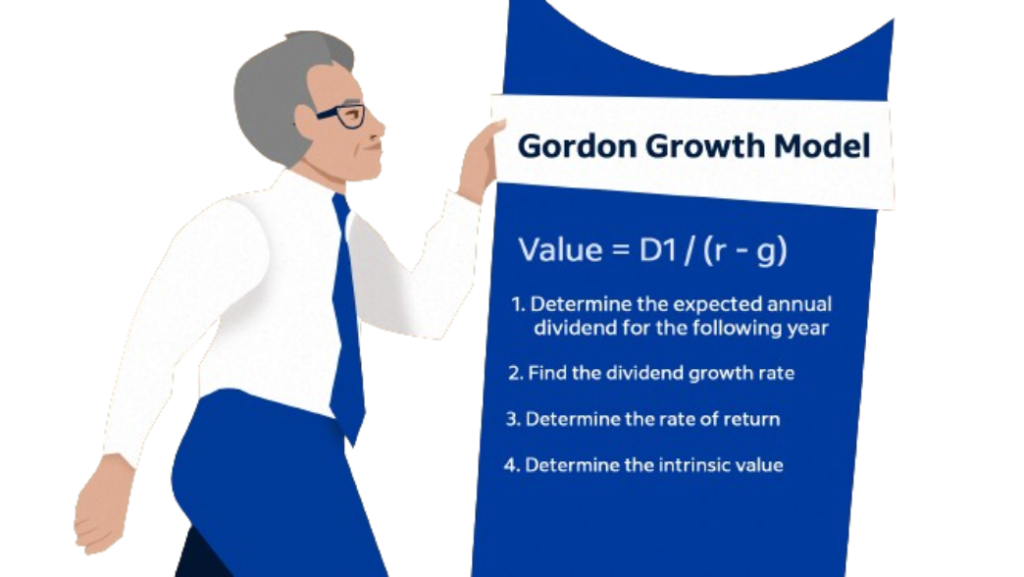

Gordon Growth Model (GGM) is a technique which is used to calculate the intrinsic value of a stock based on a sequence of future dividends that will increase at a steady rate. This is a widely used and uncomplicated version of the dividend discount model (DDM). The GGM solves for the present value of an endless series of future dividends under the assumption that dividends will grow at a constant rate in perpetuity.

The Gordon Growth Model (GGM), named after economist Myron J. Gordon, calculates the fair value of a stock by examining the relationship between three variables:

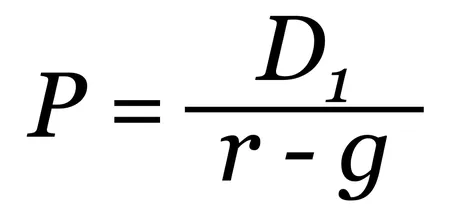

Formula:

Where,

g = Expected yearly growth rate of the dividend per share is shown by the dividend growth rate. This growth rate is taken to stay constant over the course of the valuation period in the single-stage Gordon Growth Model.

r = This figure determines the lowest rate at which equity owners must be willing to consider making an investment in a company. This rate accounts for the typical return expected from other stock market opportunities with comparable risks.

D1 = Declared dividend amount for each outstanding equity share, expressed as a per-share figure that represents the expected revenue for shareholders, is known as the Dividend Per Share.

Assumptions of the Gordon growth Model:

- Company exists forever and pays dividends per share that increase at a constant rate.

- The company’s business model is stable; i.e. there are no significant changes in its operations.

- The company has stable financial leverage

- The company’s free cash flow is paid as dividends

Example: ITC Limited, a major Indian conglomerate, is known for its consistent dividend payments and could be a good example for applying the GGM.

Steps to Calculate Intrinsic Value using GGM

- Determine the Dividend Per Share (DPS):

- Suppose ITC paid a dividend of ₹11 per share in the last financial year.

- Estimate the Growth Rate (g):

- Analyze the historical growth rate of dividends. Let’s assume the dividends have grown at a 6% annual rate over the last few years.

- Determine the Required Rate of Return (r):

- The required rate of return can be calculated using the Capital Asset Pricing Model (CAPM), or it can be an investor’s expected rate of return. Assume this is 10% for ITC.

- Apply the GGM Formula:

Intrinsic Value = D1 / (r – g) = 11 / (0.10 – 0.06) = 11 / (0.04) = ₹275

Thus, the intrinsic value of ITC Limited using the GGM model would be ₹275 per share.

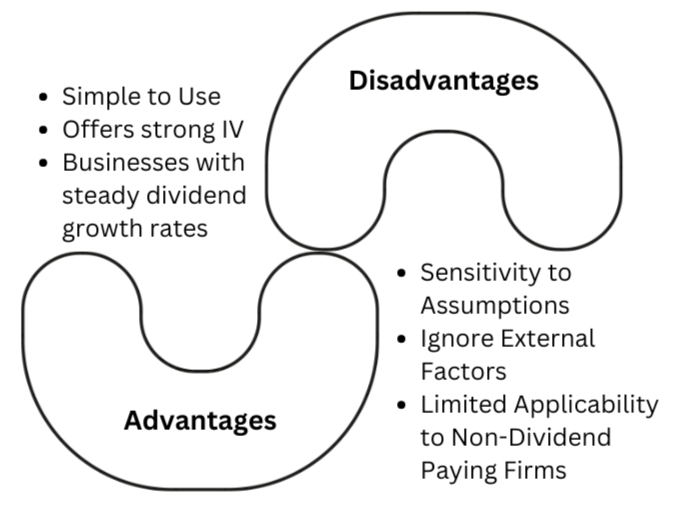

Advantages of GGM

- Simple to Use:

One of the main advantages of the Gordon Growth Model is its simplicity. With just three variables to consider—expected dividend, needed rate of return, and dividend growth rate—the GGM provides a simple method for determining a stock’s intrinsic value. Because of its simplicity, the model can be used by a wide range of investors and finance professionals, even those with no background in financial research.

- Offers a Robust Stock Value Estimate:

Applying the Gordon Growth Model correctly to the right kind of companies can provide a credible assessment of a stock’s intrinsic value. Focusing on dividends and their growth, the model emphasizes how important it is for a business to be able to produce future cash flows.

- Applicable to Businesses Showing Steady Growth Rates:

The GGM is very useful for assessing businesses with steady dividend growth rates. Particularly well-suited for established businesses in non-cyclical sectors that frequently exhibit consistent dividend increases in line with the model’s presumptions.

Disadvantages of GGM

- Sensitivity to Assumptions:

The precision of the Gordon Growth Model’s assumptions, mainly the dividend growth rate and discount rate, determines the model’s accuracy. Variations in predicted stock value can be large even with minor changes to these assumptions.

- Ignorance of External Factors Affecting Growth Rates:

The Gordon Growth Model ignores outside variables that may have an impact on a company’s growth rates, such as modifications to the market, advances in technology, or changes in regulations. Valuation estimates could become inaccurate as a result of this omission.

- Limited Applicability to Non-Dividend Paying Firms:

The model is less useful for firms that don’t pay dividends because it depends on them for value. Accurate valuation using this technique is hampered by companies that prioritize alternate kinds of shareholder returns, such as stock buybacks or reinvestments.

Example 1: High-growth companies like Zomato typically do not pay dividends as they reinvest earnings to fuel expansion. The GGM cannot be applied since it requires a steady dividend payout and growth rate.

Example 2: While Reliance Industries does pay dividends, the amount and frequency have varied significantly over time. The GGM assumes a constant growth rate in dividends, making it unsuitable for companies with irregular or unpredictable dividend policies.

In these cases, alternative valuation methods, such as the Discounted Cash Flow (DCF) model, price-to-earnings ratios, or other models tailored to growth or non-dividend-paying companies, are more appropriate.

Conclusion

Despite several limitations, the Gordon Growth Model is a useful tool for making financial decisions & for valuing dividend-paying stocks, particularly in stable industries where growth can be reasonably predicted. It clarifies how growth rates, discount rates, and valuation interacts, creating a clear link between valuation and return.

If the market price is higher than the intrinsic value determined by the Gordon Growth Model, the share is considered undervalued and investors have an attractive opportunity to purchase it. On the other hand, if the market price is higher than the model’s intrinsic value, this indicates that the share is overpriced and investors should exercise care.

However, its application is limited to companies with consistent dividend policies and predictable growth rates. For companies outside these parameters—such as high-growth firms, those with irregular dividends, or non-dividend-paying companies—alternative valuation methods are necessary. Investors should use the GGM with caution, understanding its assumptions and limitations, and complement it with other valuation techniques to obtain a more comprehensive view of a company’s intrinsic value.