NSE: BLUESTARCO

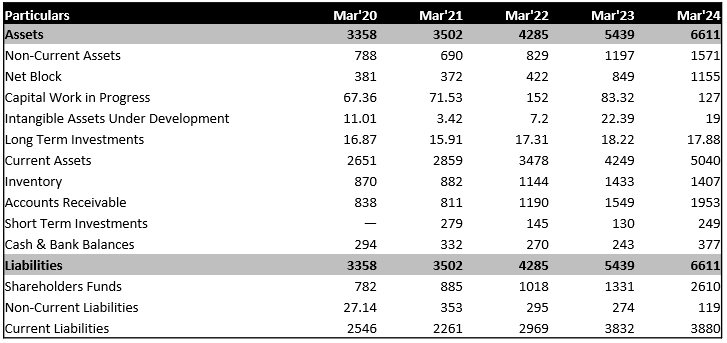

Balance Sheet

Equity Base Strengthening:

• In FY24, the company strengthened its equity base through initiatives. It issued 9.63 crore bonus equity shares in a 1:1 ratio following shareholder approval and raised ₹1,000 crores via a Qualified Institutional Placement (QIP) of 1.29 crore shares at ₹770 per share. {3}

• These actions raised the total equity shares to 20.56 crores and the equity share capital to ₹41.12 crores, strengthening the capital structure and enhancing shareholder value. In FY24, the company spent ₹143.47 crores on research and development, marking a significant 94% increase from ₹73.89 crores in FY23. This reflects the company’s continued investments in manufacturing capacity, R&D, and digitalization initiatives. Additionally, the company plans to strengthen its presence in the USA and Europe.

Trade Receivables:

• As of March 31, 2024, the company’s trade receivables increased to ₹1,952.56 crore from ₹1,548.82 crore in FY23, with ₹42.37 crore of receivables over three years old, down from ₹135 crore in the previous year. {2}

• The allowance for doubtful debts rose to ₹147.33 crore from ₹127.99 crores, driven by ₹56.08 crore in new impairment losses, offset by ₹34.78 crore written off as bad debts and ₹1.96 crore of reversals. These figures reflect the company’s effective credit risk management and focus on resolving long-standing receivables.

Investment:

• As of March 31, 2024, the company’s current investments in mutual funds increased substantially to ₹248.92 crore from ₹129.88 crore in FY23, driven by higher allocations to growth-focused schemes. {2}

• Key investments included ₹32.52 crore in HDFC Mutual Fund, ₹38.78 crore in UTI Mutual Fund, and ₹69.56 crore in Aditya Birla Mutual Fund, along with new investments totaling ₹82.74 crore in ICICI, Nippon India, and SBI Mutual Funds. Conversely, investments in Axis and Kotak Mutual Funds decreased, indicating a strategic portfolio realignment.

• This shows the company’s efforts to get better returns from liquid assets while managing risks wisely.

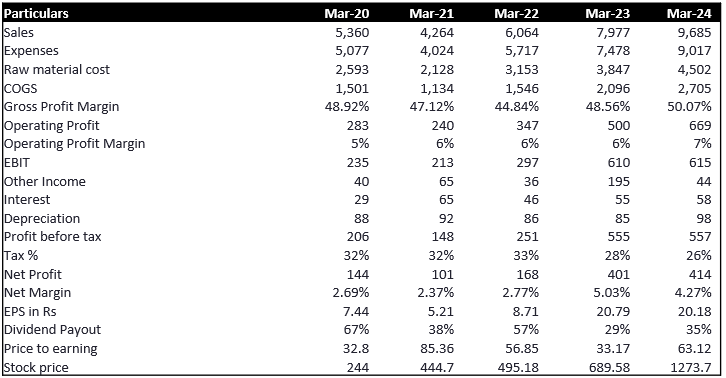

Profit & Loss Statement

Revenue Growth:

• The company recorded a 21.4% revenue growth in FY23-24, with segment-wise contributions including a 32.6% increase to ₹1,428.42 Cr in Q2FY25 from Electro-Mechanical Projects & Commercial Air Conditioning Systems, a 5.1% rise to ₹767.00 Cr from the Unitary Products segment, and a 3.8% growth to ₹80.54 Cr from Professional Electronics and Industrial Systems. {2}

• It continues to project a 20-25% top-line growth and an 8.5-9% operating margin for FY25, driven by developments in international markets, particularly in Europe and the US. Additionally, FY24 saw a strong 25% growth in online sales, significantly contributing to the overall revenue. {3}

Order Book:

• As of March 31, 2024, the company’s order book reached ₹5,697.34 crore, with operating margins improving to 6.9% from 6.2% in FY23. By September 30, 2024, the order book grew by 9.8% to ₹6,598.20 crore, driven by an order inflow of ₹1,899.06 crore in Q2FY24. {3}

• The company saw growth in its manufacturing and data center segments, along with progress in infrastructure project execution. Management expects strong performance to continue in the Room AC, Electro-Mechanical Projects, and Commercial Air Conditioning businesses in FY25. Additionally, product testing and validation are progressing in international markets, particularly in Europe and the US. {2}

Raw Material Cost:

• The raw material cost increased by 17% in FY24, driven by a 16% rise in the cost of materials consumed during FY23-FY24 and a 27% increase in project costs in FY24. {2}

• The company utilized 752.56 metric tons of Copper in FY23, which rose to 1,181 metric tons in FY24. Aluminum consumption increased from 470 metric tons in FY23 to 685.78 metric tons in FY24. To mitigate price volatility, the company employed commodity hedging strategies for copper, aluminum, and other raw material inputs in FY24, ensuring stability in future cash flows. {2}

Profitability:

• Net profit grew by 3.5% in FY23-24, significantly lagging the 21.4% increase in revenue during the same period. The net profit margin declined by 15%, primarily due to a surge in raw material costs and higher employee benefit expenses. While these factors impacted profitability, the company maintained steady revenue growth. {2}

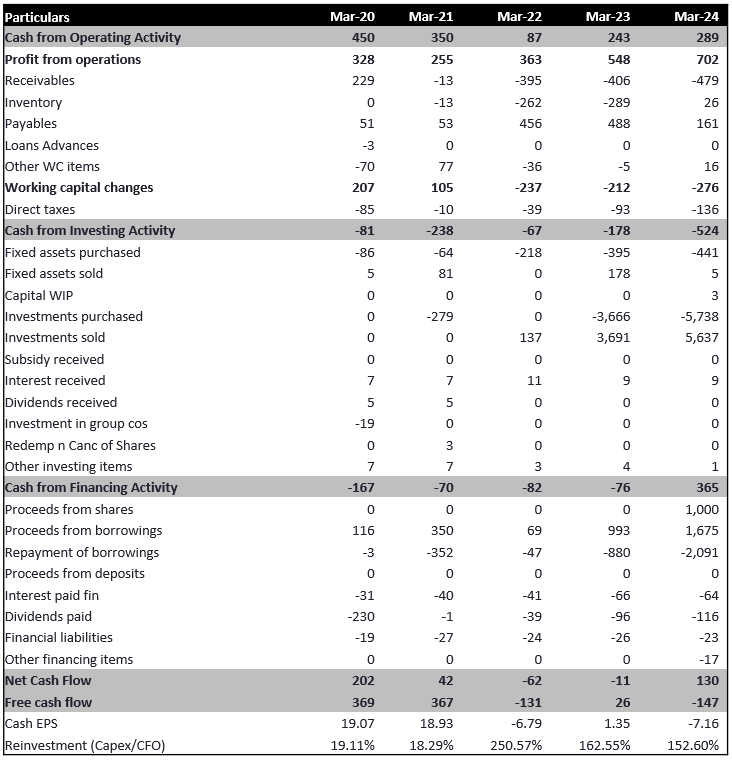

Cash Flow Statement