Overview of the Indian Banking Industry

The Indian banking industry is one of the largest in the world, comprising 12 Public Sector Banks (PSBs), 21 Private Sector Banks, 46 Foreign Banks, and 43 Regional Rural Banks (RRBs). With over 150,000 branches and more than 2,00,000 ATMs, it serves as the backbone of India’s financial system. Public sector banks like BoB dominate the market but face increasing competition from private players and digital-first banks.

The Reserve Bank of India (RBI) is the primary regulatory authority, ensuring financial stability, enforcing prudential norms, and promoting financial inclusion. Key milestones include liberalization in the 1990s, the rollout of reforms like the Insolvency and Bankruptcy Code (IBC), and the push for digital banking post-2016.

Industry Structure and Market Size

As of FY24, total banking assets in India stood at ₹281 trillion, with Public Sector Banks (PSBs) accounting for over 60% of this. Credit growth surged to 15.4% YoY, reaching a base expansion of ₹1,70,000 crores, driven by retail and MSME lending. The deposit base expanded to ₹2,20,000 crores, growing at 9.4% YoY. PSBs, including Bank of Baroda (BoB), collectively hold a 70% market share in rural and semi-urban regions, owing to their extensive branch networks.

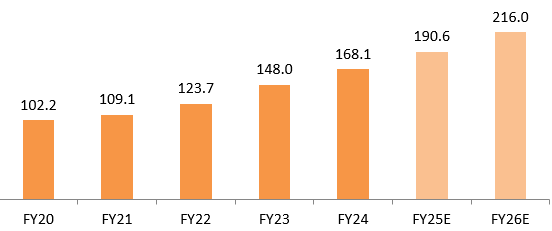

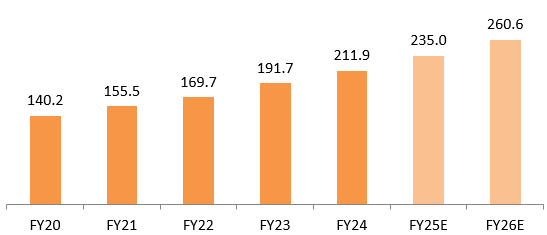

Advances are projected to increase from ₹102.19 lakh crore in FY20 to ₹216.04 lakh crore in FY26E. This growth is driven by factors such as increasing credit demand from various sectors, and especially government programs like PM VISHWAKARMA (Collateral free loans), and Pradhan Mantri Mudra Yojana priority sectors. The Indian banking industry is witnessing a steady growth in deposits as well. The deposits are expected to increase from ₹140.20 lakh crore in FY20 to ₹260.61 lakh crore in FY26E.

Exhibit: Advances base expected to grow at 13% YoY and reach ₹2.15 lakh Cr by FY26 (Data in Lakh Cr)

Source: Tijori Finance

Exhibit: A Deposit base expected to grow at 11% YoY, and reach ₹2.5 lakh Cr. by FY26 (Data in Lakh Cr.)

Source: Tijori Finance

Macroeconomic Environment and Key Drivers

India’s economy is poised for growth, with a projected GDP expansion of 6.3% in FY24. The macro environment supports sustained credit demand, driven by industrial activity, a resurgence in private investment, and strong domestic consumption. With inflation moderating to 4.2% as of October 2024, the Reserve Bank of India (RBI) is likely to maintain a neutral monetary stance in the near term, keeping the repo rate stable at 6.5%.

This stability is expected to ease borrowing costs and foster greater financial activity. On the digital front, India continues to lead in payment innovation, with Unified Payments Interface (UPI) transactions surpassing a monthly volume of ₹15 trillion. The rapid adoption of digital banking solutions will likely fuel fintech partnerships and redefine customer engagement in traditional banking.

Potential headwinds include lingering impacts of high interest rates, which could suppress private capital expenditure in some sectors, and global economic uncertainty, particularly if advanced economies face a slowdown. Nonetheless, government-led infrastructure spending, favorable demographics, and reforms aimed at boosting ease of doing business should provide a cushion against external shocks.

Looking ahead, the Indian banking sector is expected to benefit from this positive macroeconomic trajectory, with credit growth anticipated across key segments such as MSMEs, retail, and infrastructure financing. Asset quality is likely to remain stable, supported by improving corporate health and policy support for stressed sectors.

Key Trends and Developments

Public Sector Banks (PSBs), including the Bank of Baroda, are set to benefit from key emerging trends and macroeconomic support. The rapid adoption of digital lending platforms, AI-based credit assessment tools, and mobile banking solutions is driving faster loan disbursements and operational efficiency.

With digital payments expected to account for 65% of all transactions by 2026, PSBs are poised to capture significant growth in retail and SME lending, particularly in Tier-2 and Tier-3 cities. Retail lending, a key growth driver, is projected to grow at a 16%-18% CAGR, fueled by rising demand for personal and housing loans.

Asset quality improvements remain a highlight, with the Gross NPA ratio already reducing to 5.5% in FY24. Continued recoveries through frameworks like IBC and SARFAESI, alongside strong provisioning buffers, are expected to maintain this positive trajectory. The recent wave of mergers, such as Bank of Baroda’s integration with Vijaya Bank and Dena Bank, has enhanced economies of scale and operational efficiency, paving the way for higher profitability and better capital utilization.

Additionally, financial inclusion initiatives, including PMJDY’s addition of over 500 million accounts, and the growing focus on green finance, position PSBs to expand their rural reach and align with global ESG mandates. However, challenges persist in the form of rising competition from private players and fintechs, along with the need for ₹2 trillion in fresh capital by FY26 to meet Basel III norms.

Despite these challenges, PSBs are projected to achieve loan growth of 11%-13% CAGR over the next three years, supported by strong retail and MSME credit demand. Improved profitability, stable margins, and enhanced balance sheet health are expected to cement their role as key contributors to India’s economic growth.

Industry Opportunities

Financial inclusion initiatives, such as PMJDY, have added over 500 million bank accounts, enabling PSBs like Bank of Baroda to expand rural penetration and tap into underserved markets. With rural India contributing nearly 46% of national income, targeted banking services in these areas present significant growth potential.

The MSME sector, accounting for over 30% of GDP and employing 110 million people, offers a lucrative opportunity for credit expansion. Government programs like ECLGS have supported over ₹3.7 lakh crore in credit, underscoring the sector’s importance as a key growth driver for banks.

Green Finance: Banks are exploring sustainable financing opportunities, with RBI promoting ESG-aligned lending and SEBI introduces BRSR core, which applies to the top 150 listed companies by market capitalization from FY2024. [1]

Industry Challenges

PSBs will continue to face significant challenges in the coming years, particularly related to asset quality and profitability. Despite improvements, the high Gross NPA ratio of 5.5% for PSBs, compared to 2.5% for private banks, remains a key concern. While ongoing efforts to resolve stressed assets through mechanisms like IBC are likely to improve asset quality, NPAs will continue to weigh on profitability. The Return on Equity (ROE) of 9% for PSBs in FY23 is considerably lower than 15% for private banks, reflecting ongoing struggles with cost efficiency and capital utilization.

The rise of FinTechs and digital-first private banks is intensifying competition, particularly in urban markets, which could further erode PSBs’ market share. With digital banking gaining momentum, PSBs must accelerate their transformation to stay competitive. Moreover, PSBs are under pressure to comply with Basel III capital adequacy norms, requiring ₹2 trillion in fresh capital by FY26. This necessitates a strategic focus on improving operational efficiency, digital innovation, and cost optimization. If these challenges are not addressed, PSBs may struggle to enhance profitability and meet future growth expectations, especially in a rapidly evolving banking landscape.

Competitive Landscape

In the public sector banking space, State Bank of India leads with a commanding 23% market share in loans, followed by Bank of Baroda (BoB) and Punjab National Bank. Among private banks, HDFC Bank, ICICI Bank, and Axis Bank dominate, consistently outperforming PSBs in CASA growth and profitability metrics.

Bank of Baroda, as the second-largest public sector bank, holds total assets of ₹13 trillion and operates a robust branch network of over 8,200 branches as of FY24. Notably, BoB’s Gross NPA ratio improved to 3.5%, outperforming the average PSB and reflecting its focused efforts on asset quality improvement.

Regulatory Environment

The future outlook for PSBs remains cautiously optimistic, supported by continued improvements in asset quality, regulatory compliance, and digital transformation. The implementation of frameworks like IBC and SARFAESI has already led to the recovery of ₹10 trillion in stressed assets since 2017, bolstering the balance sheets of PSBs. This trend is likely to continue, improving asset quality further and reducing the burden of non-performing assets (NPAs). The CET-1 ratio of 10.9% for Bank of Baroda in FY24 demonstrates PSBs’ progress in strengthening capital adequacy and meeting Basel III norms. This trend of improving capital ratios should continue, supporting financial stability and regulatory compliance.

With the repo rate unchanged at 6.5% and the policy stance remaining neutral, PSBs can expect stable borrowing costs in the near term, which will help maintain credit growth. However, high interest rates may continue to pressure margins, particularly for PSBs that have a large proportion of costlier legacy loans.

Furthermore, the regulatory push towards UPI, open banking, and digital wallets is accelerating the digital transformation of the banking sector. These initiatives will enable PSBs to better serve tech-savvy customers and compete with private sector banks and fintechs. Over the next few years, PSBs are likely to witness improved operational efficiency through the adoption of digital banking solutions, driving growth in retail and MSME lending while enhancing customer engagement and retention.