NSE: MONTECARLO

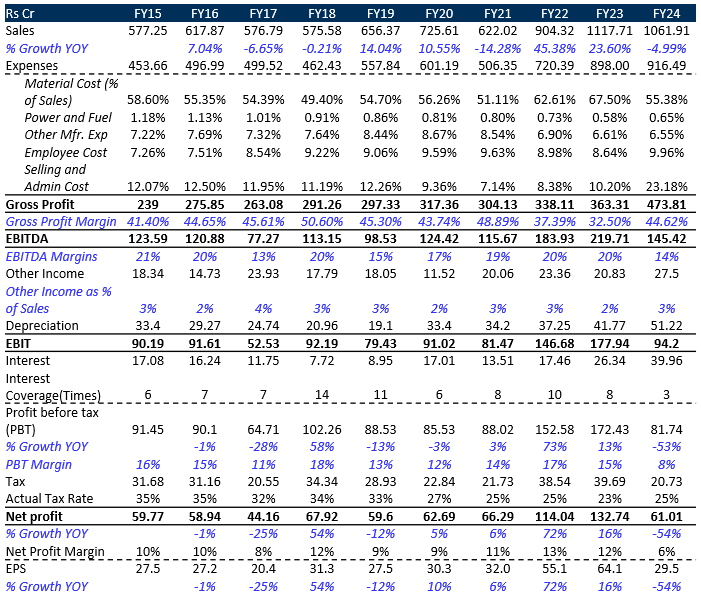

Income Statement

• FY23 saw strong sales growth of 23% due to aggressive expansion into large format stores and EBOs. However, in FY24, delayed winter, excess inventory, and higher discounts caused a decline in sales by 5% and impacted EBITDA. (May’24 concall, page 3)

• The company expects flat revenue growth in FY25 due to the closure of unprofitable stores and channels but anticipates improvement in profitability through 40-45 store additions and a 7-8% price increase to counter the effect of discounts which happens in the discount season.

• The management expects the cost of funds to come down to 100-200bps as the company is liquidating some old stocks.

• MCFL had good volume growth with woolen sales increasing from 19 lakh to 21.46 lakh units and cotton sales from 74 lakh to 76.06 lakh units. However, despite the volume increase, revenue declined due to higher discounts which negatively impacted net sales figures.

• In FY24, the company overestimated demand due to unexpectedly high sales in FY23, leading to excess inventory. To clear this inventory during the shortened selling season, they offered higher discounts. Despite the discounting, unsold merchandise remained, which had to be returned, further affecting margins.

• Moving forward, the company has allocated returned inventory to stores and adjusted production levels to match FY23’s demand. They expect flat revenues in FY25 but anticipate a significant improvement in profitability through optimized inventory management, controlled production, and shutting down underperforming stores.

• The company is closing down underperforming stores, including 4-5 EBOs, 30 SIS locations, and 35 sale points in large format stores (LFS), which contribute around ₹20-25 crore in revenue. The decision is driven by low margins, high rental costs, and low footfalls, especially in SIS and LFS locations. In these stores, low sales returns and excessive discounts made operations unsustainable. The closures are primarily in Northern, Eastern, and Central regions. Simultaneously, the company is opening 45-50 new EBOs to offset the revenue loss from these closures.

• In FY24, the company saw strong regional performance in the South and West, with sales increasing from ₹40 crore to ₹53 crore in the South and from ₹69 crore to ₹80 crore in the West. Despite higher returns in the North and East due to the late winter season, these regions continued to grow. The company opened 8 EBOs in the South and West last year and plans to open 10 more this year, projecting South to reach ₹70 crore and West to grow to ₹90 crore in FY25.

• To adapt to changing consumer preferences favouring discounts, the company has raised prices by 7-8%, higher than the usual 3-4% increase. This price adjustment aims to mitigate the impact of discounting on margins.

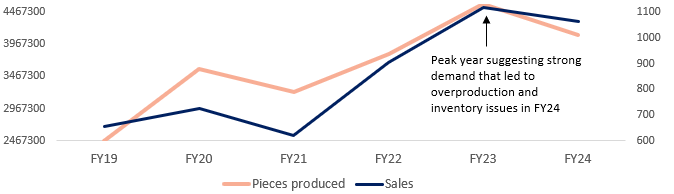

Exhibit 1: In FY24, there was a 10% drop in production as MCFL cashed out unsold inventory still sales revenue declined by 5% due to discounting.

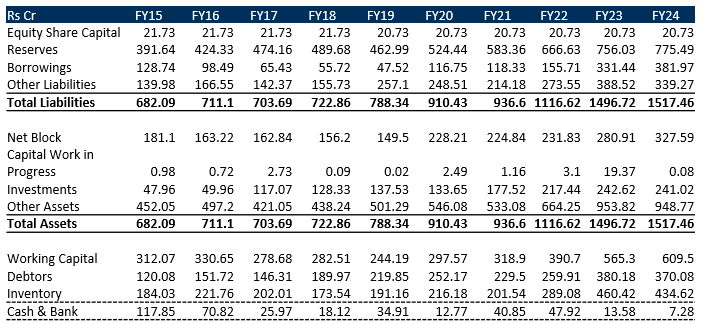

Balance Sheet

The company’s Debtors and Inventory levels surged sharply, particularly in FY23 and FY24. Debtors grew from ₹120 crore in FY15 to ₹370 crore in FY24, which can lead to issues with credit management and slower collections. Inventory saw a similar rise, increasing from ₹184 crore in FY15 to ₹435 crore in FY24, which led to overstocking, especially in recent years. Both trends indicate liquidity pressures if not addressed.

Additionally, Cash & Bank balances have consistently declined from ₹118 crore in FY15 to just ₹7 crore in FY24. This steep drop in cash reserves indicates that the company has been using its cash resources aggressively, possibly for expansion or debt servicing. This raises concerns about the company’s liquidity and its ability to meet short-term obligations.

The declining cash balance and growing reliance on borrowing may pose risks especially if operational performance does not keep pace with the company’s financial obligations.

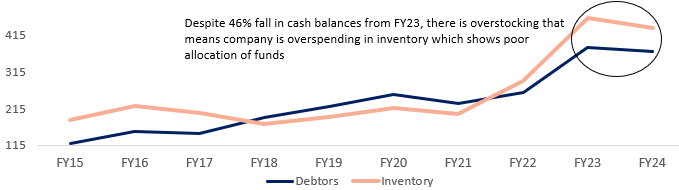

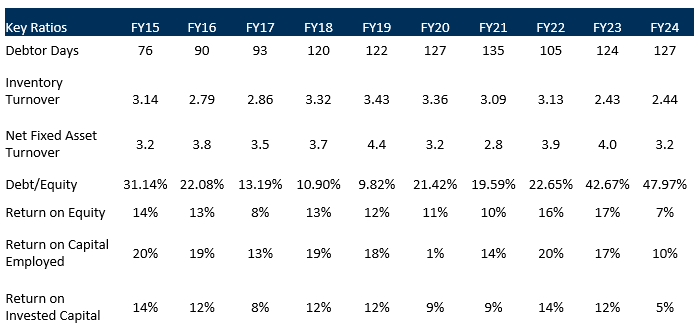

Exhibit 2: There is not only a debtor rise but the quality of debtor is also deteriorating as debtor days have increased from 76 in FY15 to 127 in FY24 which indicates slower payment collection from customers

Ratio Analysis

Over the last 8 years (FY2015-FY2022), the inventory turnover ratio (ITR) of the company has stayed in the range of 3 to 3.5.

An inventory turnover of 3 indicates that about 4-month’s worth of sales of MCFL is tied up in the inventory for the company. This is a large amount of inventory that MCFL carries on its books.

The credit rating agency, ICRA, explained the reasons for the large inventory requirement by apparel manufacturers, in its rating guidelines for the sector. The key reasons are multiple designs, colors, etc.; the need to keep stocks in warehouses, and sales returns.

Nevertheless, over the years, MCFL has kept its inventory turnover ratio within a tight range (excluding FY23 and FY24) indicating that it has maintained its inventory utilization efficiency.

Moving forward, the company has highlighted to its investors that it will keep inventory risks under control by ensuring that most of the garments are produced only after getting bookings from the retailers and selling them on an outright basis to the retailers without any large amount of returns of the unsold inventory.

MCFL has an SSGR (Self-sustainable growth rate) of 0% and if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company has to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth. This is boosting the debt levels of MCFL impacting the debt/equity ratio.