Written By: Bhumika Jain

If you’ve ever listened to a company’s conference call, you’ve likely heard management mention “You will see the benefits of operating leverage from next quarter onwards”. But what does it actually mean?

Operating leverage is about how a company’s fixed costs affect its profits without making any changes to the selling price, margin, or the number of units it sells.

Imagine you run a factory that makes shoes.

1) Fixed Costs: These are your constant expenses like rent, machinery, and salaries, let’s say are ₹1,00,000 every month – you pay them whether you produce 10 shoes or 10,000 shoes.

2) Variable Costs: These depend on how much you produce, like raw materials.

Now, if your sales go up, your fixed costs don’t change, so most of that extra revenue turns into profit. This is operating leverage – when higher sales lead to disproportionately higher profits because fixed costs remain constant.

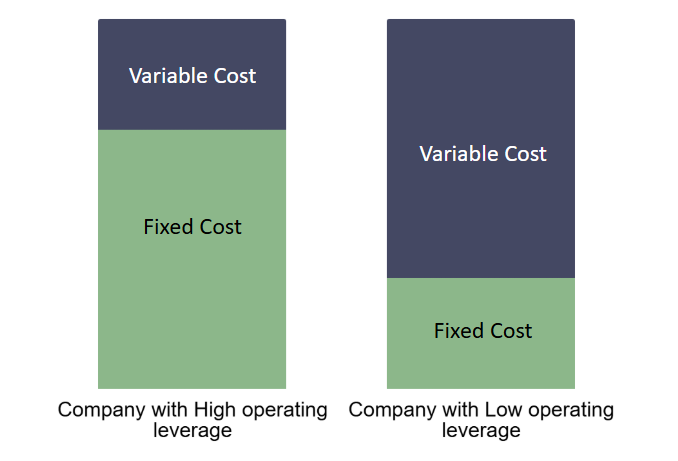

It is important to compare operating leverage between companies in the same industry, as some industries have higher fixed costs than others. The concept of a high or low ratio is then more clearly defined.

If you only sell 10 shoes in a month, the fixed costs still need to be covered. So, each shoe would have to contribute a larger portion of the profit to cover that ₹1,00,000. So, Low operating leverage companies may have high costs that vary directly with their sales but have lower fixed costs to cover each month.

But if you sell 10,000 shoes, those fixed costs are spread out over more shoes, meaning each shoe doesn’t have to cover as much, and you can make a bigger profit. So, Companies with high operating leverage must cover a larger amount of fixed costs each month regardless of whether they sell any units of product.

Why does management mention it?

When companies spend money to grow, like building bigger factories or buying new machines, these are fixed costs. These costs don’t change no matter how much or how little the company produces.

In the beginning, profits might seem low because sales aren’t high enough to cover all these fixed costs. But as sales increase, the company eventually reaches a point where these fixed costs are fully covered. After that, most of the extra money from sales turns into profit. This is the advantage of operating leverage – it allows profits to grow faster once sales reach a certain level.

Operating leverage also shows how sensitive profits are to sales. It works great when sales are growing because profits rise quickly. However, during downturns when sales drop, it can be risky. Fixed costs still have to be paid, even if the company isn’t selling much, which can hurt profits or even lead to losses.

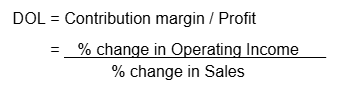

In these situations, the degree of operating leverage (DOL) is used, it is a way to measure how much a company’s profits will change when its sales go up or down.

For example, if your shoe factory has high fixed costs, a small increase in sales can lead to a much bigger increase in profits. This means your degree of operating leverage is high. On the other hand, if your fixed costs are low, changes in sales won’t affect your profits as much, which means a lower degree of operating leverage.

Companies with a high DOL benefit more from growing sales but also face bigger risks if sales drop because those fixed costs still need to be paid no matter what. It’s like riding a roller coaster – the highs are exciting, but the lows can be tough to manage!

This ratio is also often used when forecasting sales and determining appropriate prices. By understanding how fixed costs and profits are linked, companies can predict how much profit they’ll make if sales go up or down.

For example, if your shoe factory knows its DOL, it can calculate how much extra profit it will earn by selling more shoes or how much profit it might lose if sales slow down. This information helps set prices that cover fixed costs while staying competitive.

When the degree of operating leverage is high, even a small mistake in predicting sales can lead to big mistakes in estimating cash flow. This is because small changes in sales have a bigger impact on profits, making it riskier if the forecast isn’t accurate.

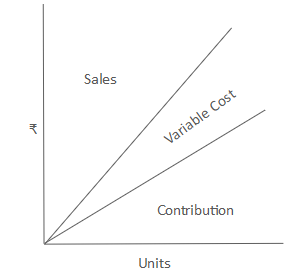

After filtering out the fixed costs, increases in volume will increase both the overall variable expense and the overall contribution.

Why don’t all companies operate at their optimum capacity to get the best of their leverage?

Sometimes companies deliberately choose not to run at full capacity because it might cost more to produce extra than they’d earn from selling those additional units. Additionally, running at full speed can wear out machinery or increase maintenance costs.

Companies also need to be careful during slow periods or when demand isn’t stable. Fixed costs, like rent or salaries, don’t change even if they produce less. If they push for full capacity without enough sales, it could hurt their profits instead of helping.

In short, companies aim to balance their production with demand to get the best results from their operating leverage while avoiding waste or unnecessary costs.

If volume or demand for the product is a concern, why do companies create a new product that competes with or takes away demand for an original product?

If a company is worried about not having enough demand or sales volume for one of its products, it might launch a new product that overlaps with or directly competes with the existing one. This is called cannibalizing demand.

For example, imagine your shoe factory makes high-end sneakers, but sales are low because not everyone can afford them. To attract more customers, you launch a more affordable version of the sneaker. Some customers who might have bought the high-end sneaker will now choose the cheaper one instead. This reduces the demand for the original product but increases overall sales and reaches a new group of customers.

Companies use this strategy carefully. The idea is to grow overall revenue and market share, even if it means sacrificing some sales of the original product.